Time to explore the Ethereum basis trade

Published 11 July 2024

Director, Digital Assets Research

Key Takeaways

- Related Products WisdomTree Physical Bitcoin, WisdomTree Physical Ethereum Find out more

Earlier this year, we published ‘How to smooth returns when investing in cryptocurrencies: The basis trade’, which focused on Bitcoin basis trade. In summary, we outlined that investors had a unique opportunity to enjoy a free lunch by capitalising on crypto market inefficiencies.

As such unique opportunities tend not to last too long (especially after the launch of US-domiciled Bitcoin ETFs that gathered more than USD 10 billion shortly after going live), we thought it was worth exploring whether there was scope for basis trade with Ethereum.

Basis trade

To implement basis trade, investors simultaneously take a long position in the spot market and a short position in futures contracts. By exploiting the price differential between spot and futures, investors aim to generate positive returns independent of the underlying asset’s price movement. The key idea behind this trade is that the future price converges towards the spot price as the futures contract approaches maturity.

It is interesting to note that during February 2021 – May 2024 period Bitcoin offered more opportunities for basis trade than Ether. This is because the curve was backwardated:

- 33% of the time for Ether

- 22% of the time for Bitcoin

Figure 1: Periods where ether futures traded above the spot price

Source: WisdomTree, Bloomberg. Historical performance is not an indication of future performance and any investments may go down in value.

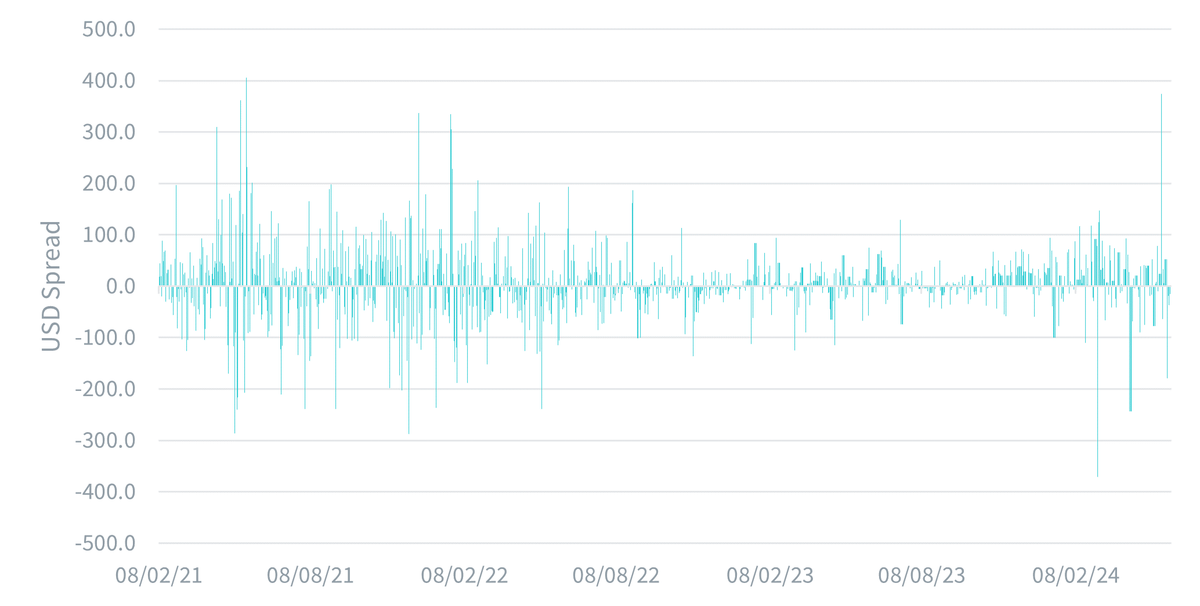

Figure 2: Spread between front contract and spot prices converges

Source: WisdomTree, Bloomberg. Historical performance is not an indication of future performance and any investments may go down in value.

Assumptions

To set up the scene, we are using the same assumptions1 as what we had for the Bitcoin basis trade:

- Use WisdomTree Physical Ethereum ETP for the spot with a notional of 100%

- Hold trade until futures expiration

Then, every month:

- Close short exposure in a futures contract that expires

- Short the next contract on the curve

- Ensure dollar exposure is the same on the long and short legs at rebalance

- In case the futures price is lower than the spot price, remain in cash (assumed at 0%)

For the Ethereum trade, it is important to note that staking increases spot returns. For this analysis, we assume that the ETP achieves a staking return of 0.56% per annum. This figure is based on the following assumptions:

- An Ethereum staking return of 3% per annum

- 25% of ETP staked with a 75% of staking return passed to investors via coin entitlement

For the avoidance of doubt, there are many ways a basis trade could be implemented. As such, the above assumptions and actions could be changed to fit an investor’s strategy and investment approach.

Risks

It is important to remember that basis trade exposes investors to the following risks:

- The future’s price does not converge to the spot price before the position is closed

- The future’s price diverges from the spot before the position is closed

In the case of the former, the return would be reduced. In the case of the latter, the return would be negative. That is, the investor would experience a loss.

Results

After running a backtest analysis for the February 2021 – May 2024 period, we observed interesting results. Specifically, the strategy was not invested 33% of the time (backwardated curve), had a positive return 51% of the time, and a negative return 15% of the time. Moreover, the average mean return was 1.4% on positive trades and -1.1% on negative trades, with a 3.9% maximum return and a -3.5% minimum return.

Monthly risk statistics highlight annualised volatility of 4.3% and a Sharpe ratio of 1.5.

Per trade stats | % of time | Mean return | Mean return ratio | Max return | Min return |

|---|---|---|---|---|---|

Non-invested | 33.3% | 0.0% | -- | -- | -- |

Positive trades | 51.3% | 1.4% | -- | -- | -- |

Negative trades | 15.4% | -1.1% | -- | -- | -- |

All trades | -- | -- | 1.3% | 3.9% | -3.5% |

Monthly* | |

|---|---|

Ann. return | 6.5% |

Ann. standard deviation | 4.3% |

Ann. downside standard deviation | 4.3% |

Max drawdown | -3.5% |

Calmar ratio | 1.9 |

Sharpe ratio | 1.5 |

Sortino ratio | 1.5 |

Source: WisdomTree, Bloomberg. Annualised implied carry between the second and front contracts. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

While Bitcoin basis trade had slightly more attractive backtest results, investors may find it beneficial to start exploring Ethereum basis trade as no free lunch lasts too long (i.e. Ethereum basis trade will disappear). The key components for Ethereum basis trade are already available in liquid, transparent and easily accessible form:

- WisdomTree Physical Ethereum ETP for long spot trade

- CME Ethereum futures for short futures trade

Of course, all investors need to make sure they fully understand basis trade mechanics and choose instruments and implementation strategies that are most appropriate for them.

1 Of course, we replaced Bitcoin with Ethereum, where required.

Categories

About the contributor

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).