WCBR LN

WisdomTree Cybersecurity UCITS ETF - USD Acc

Published 10 March 2025

How different was the world when President Trump first took office on 20 January 2017? Consider these contrasts between then and the close of 2024: the S&P 500 surged from 2,271.31 to 5,881.63—a gain of 259%. Bitcoin, once a fringe asset priced at $900, soared past $100,000 as institutional adoption became mainstream. Nvidia transformed from a relatively unknown company with a $59 billion market cap into a $3 trillion industry giant, while Elon Musk’s net worth skyrocketed from $12.9 billion to over $400 billion1.

For investors, such rapid change creates opportunities. Thematic investing is about identifying and capitalising on these frontiers of growth. As we step into Trump 2.0, the world will certainly evolve, and markets will inevitably move. This outlook highlights three themes that investors should consider to capture the next wave of growth.

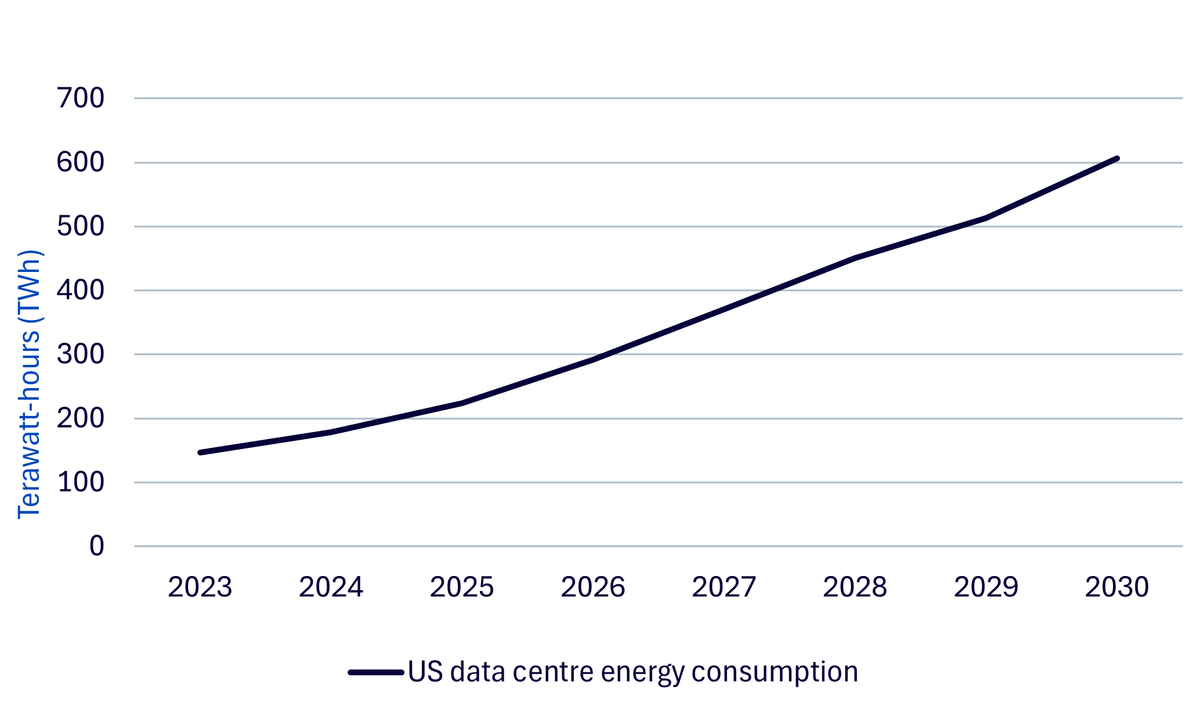

Artificial intelligence (AI) is at the heart of the next technological revolution, and it is an energy-intensive industry. The International Energy Agency highlights that a single ChatGPT query consumes ten times the energy of a typical Google search—illustrating just how power-hungry AI truly is. With an explosion in data centres, companies are actively seeking long-term energy solutions.

Source: Global Energy Perspective 2023, McKinsey, 18 October 2023, McKinsey analysis. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Big tech has already started securing energy sources to meet its growing demand. In October 2024, Google announced a partnership with Kairos Power to develop small modular reactors (SMRs) that will supply clean, reliable energy to its data centres by 2030. Unlike traditional nuclear reactors, SMRs are smaller, factory-built, and deployable closer to demand centres, making them an attractive solution for technology firms. Amazon and Microsoft are also turning to nuclear energy. Microsoft’s deal to power its data centres with energy from the Three Mile Island plant—America’s most infamous nuclear site—once it reopens in 2028 is a testament to the resurgence of nuclear energy.

With Trump back in power, energy independence will likely become a focal point. Europe, having reduced its reliance on Russian gas since the Ukraine war, is also looking for long-term energy solutions. While Trump has pushed for increased US energy exports to Europe, logistical challenges remain. Consequently, Europe is accelerating its efforts in renewable and nuclear energy. France plans to build six new nuclear reactors at an estimated cost of €50 billion, while the UK is advancing projects like the Sizewell C plant to integrate nuclear into its net-zero strategy.

As energy-intensive industries grow, nuclear power is emerging as a cornerstone of sustainable energy strategies alongside wind and solar. This year, nuclear energy will undoubtedly claim a significant seat at the table.

Regulatory environments can either stifle or stimulate innovation. US Senator JD Vance, speaking at the Paris AI Summit earlier this month, highlighted how European regulation is restricting AI growth. He emphasised that regulation should facilitate, not hinder, innovation. This sentiment is gaining traction globally, suggesting that the tone from the top is shifting towards a more accommodative regulatory backdrop for AI.

Deregulation could further accelerate advancements in AI, blockchain, and cryptocurrencies. Elon Musk, a close presidential adviser, has emphasised the importance of reducing regulatory barriers to technological progress. This aligns with the significant capital expenditures undertaken by major tech firms in 2024, a trend that is expected to continue.

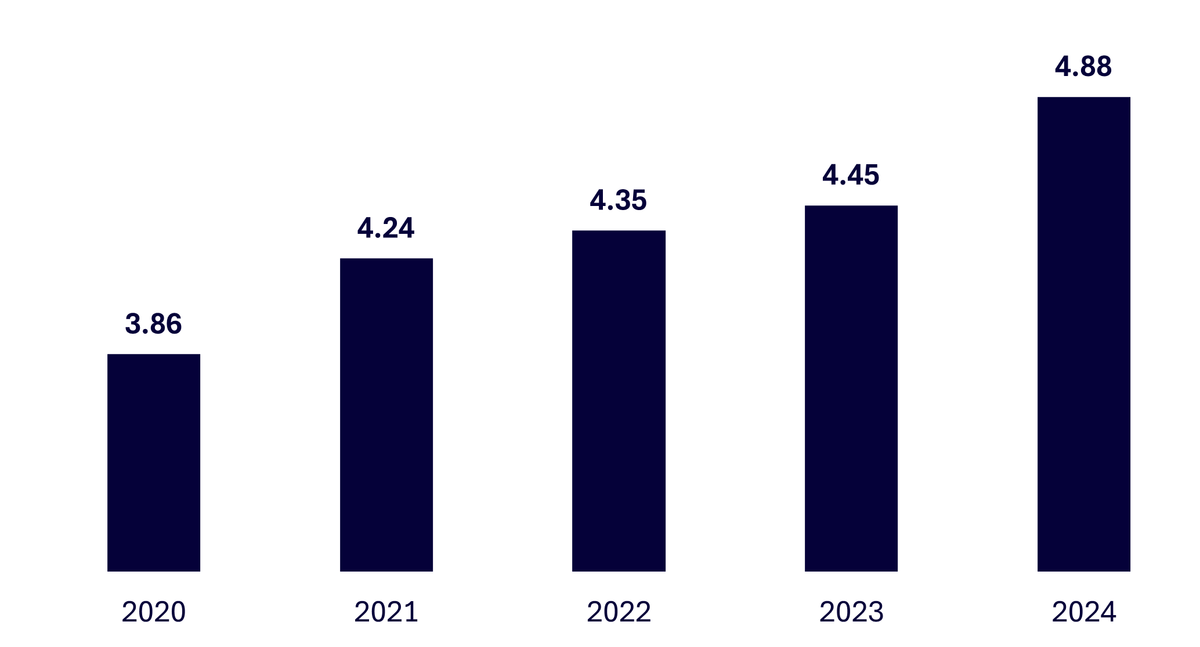

Source: IBM, 2025.

However, with increased innovation comes heightened cybersecurity risks. Figure 2 shows the steady rise in the average cost of data breaches, with a notable surge in 2024 as AI tools become more accessible and sophisticated. Cybersecurity is now a crucial aspect of corporate strategy, as companies grapple with:

As the digital economy expands, the demand for cybersecurity solutions will grow exponentially. Companies that develop robust security infrastructure will be well-positioned to thrive in this evolving landscape.

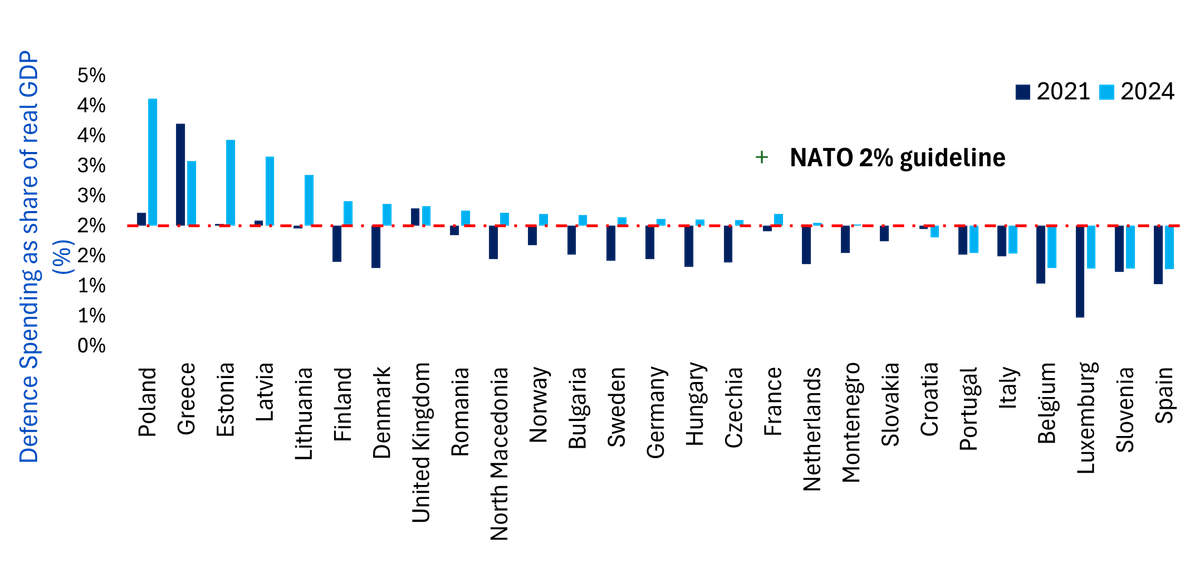

The geopolitical landscape is shifting, with Europe taking on greater responsibility for its own defence. The US has signalled that its military support for Europe will not be guaranteed, prompting European nations to strengthen their defence capabilities.

Source: Atlantic Council, WisdomTree. 2024 numbers are estimates. Iceland excluded as it does not have a standing army.

The UK has committed to increasing its defence budget to 2.5% of GDP by 2027, with a long-term goal of reaching 3%. Germany’s new leadership has also emphasised bolstering European defences, recognising the need for military self-sufficiency. European Commission President Ursula von der Leyen has proposed tapping into €93 billion of unspent COVID-19 recovery funds to finance defence spending. These measures indicate a significant pivot towards enhanced European military readiness.

Unsurprisingly, European defence stocks have reacted positively to these developments. The surge in defence spending will likely benefit companies specialising in military technology, cybersecurity, and advanced weaponry. As geopolitical tensions persist, investors should keep a close eye on the defence sector.

President Trump’s administration is set to champion technological innovation, with a more favourable regulatory environment accelerating AI adoption—reinforcing the urgent need for stronger cybersecurity. Meanwhile, the demand for secure and scalable energy solutions is driving a nuclear resurgence. At the same time, Europe’s move toward military self-sufficiency marks a significant geopolitical shift. As these themes evolve, markets will inevitably take notice, creating opportunities for investors.

For WisdomTree’s full Market Outlook, please click here.

1 Forbes, Bloomberg, February 2025.

Director, Research

@MobeenTahirWTMobeen is a member of WisdomTree’s research team where he focuses on a wide range of asset classes to offer strategic and tactical insights to our clients on global markets and investment products. Before joining WisdomTree in December 2018, Mobeen worked at Willis Towers Watson as an investment consultant advising institutional clients as well as their in-house fund business on asset allocation and portfolio construction with his research focus being equity and multi-asset smart beta. Mobeen has a BSc (Hons) in Accounting and Financial Management from Loughborough University and an MSc in Accounting and Finance from the London School of Economics and Political Science. He is also a CFA Charterholder.