DHS LN

WisdomTree US High Dividend UCITS ETF

Published 10 April 2025

There is no doubt that with his new tariff regime, U.S. President Donald Trump has upended the global economic order. The question now is: by how much?

The “Liberation Day” tariffs, announced on Wednesday, 2 April 2025, were set to take effect on Wednesday, 9 April 2025, but have been paused for most countries for 90 days. Markets have been whipsawing, declining sharply in the morning of 9 April, before rebounding strongly as tariffs were postponed.

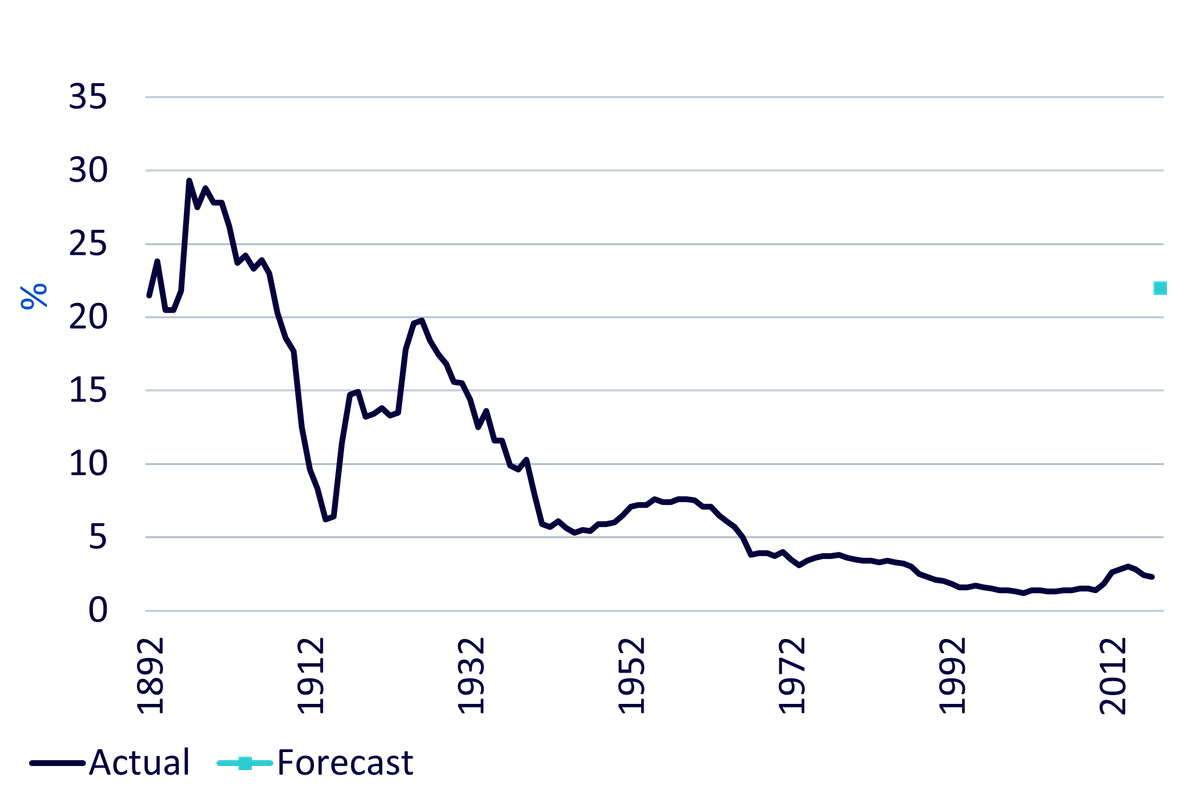

In 90 days U.S. average effective tariffs could rise to levels not seen in over a century. Pricing in such a large shock is no easy task – especially as countries scramble to negotiate their positions.

Japan appears to be leading the charge in diplomatic engagement. News reports indicate that Japanese Prime Minister Shigeru Ishiba has secured discussions with U.S. Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer. Meanwhile, the European Union’s initial proposal seems to have been rejected by Washington. The EU has also paused its steel and aluminium tariff retaliatory measures for 90 days in hope of progressing the negotiations.

U.S. tariffs on China have been scaled up to 125%, reflecting Trumps disappointment regarding China’s lack of flexibility. China has declared it will “fight to the end.” China will likely focus on stimulating domestic demand. However, on the People’s Bank of China allowed the yuan to weaken to lowest level since 2007. The move could signal the start of a competitive devaluation, which would almost certainly antagonize the U.S. and further reduce the chances of a trade truce.

On balance, the trade war appears to be escalating, not de-escalating.

Source: WisdomTree, Bloomberg, US International Trade Commission : Office of Analysis and Research Services Office of Operations. Historic: 1892-2024. Forecast: 2025

While these tariffs represent a demand shock, they simultaneously drive prices higher for goods and services consumed in the U.S. – a classic stagflation scenario that could complicate the Federal Reserve’s policy response. Though the Fed has previously suggested that tariff-driven inflation would be "transitory" – and indicated a willingness to resume rate cuts in response to growth risks – markets may already price in significant economic damage before any labour market weakness becomes visible.

Most cyclical assets are under pressure. Below is our assessment of key sectors:

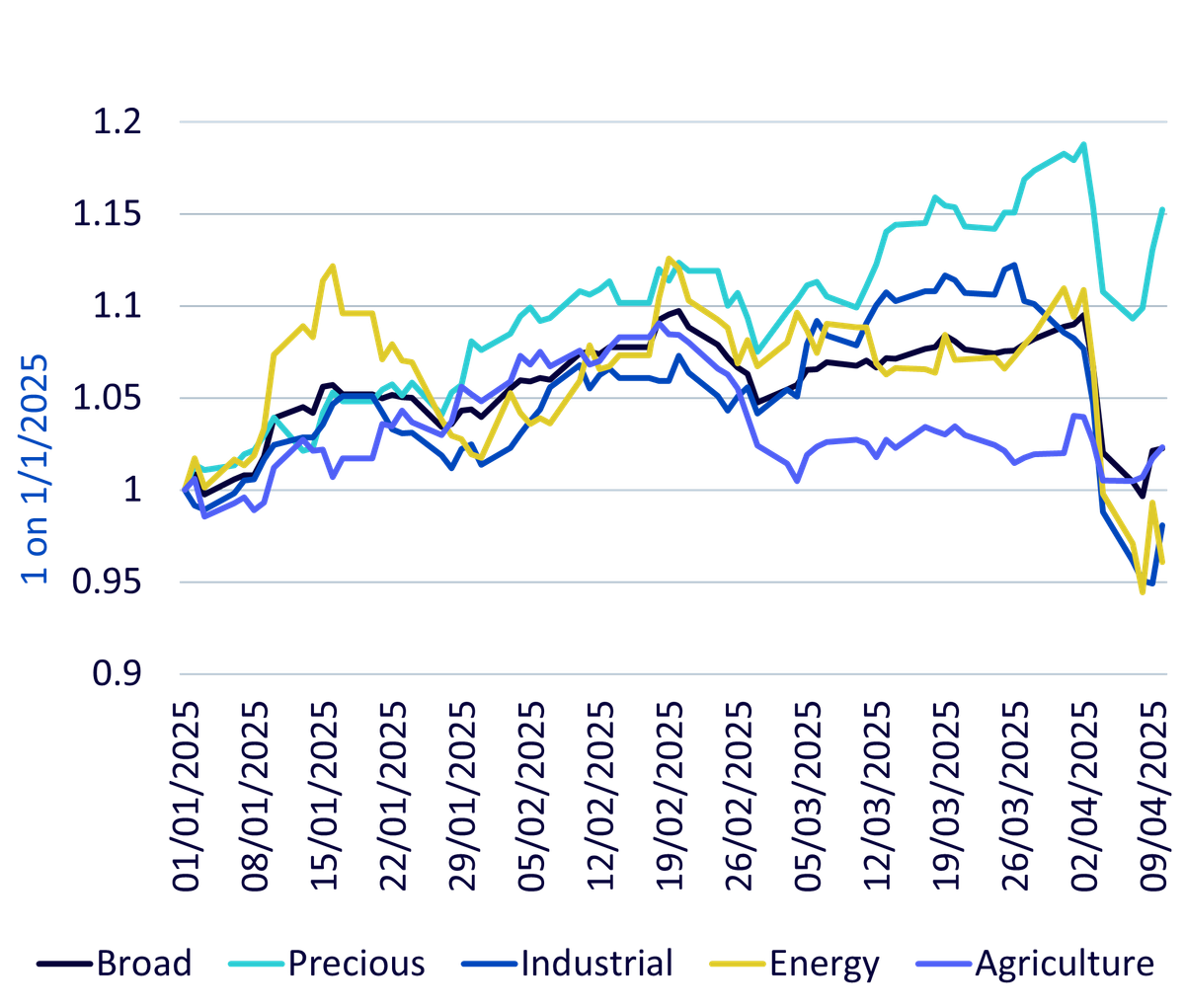

Commodity prices have declined across the board since the tariff announcement, with energy leading the losses. This is partly due to the Organisation of the Petroleum Exporting Countries and a group of allied non-OPEC oil-producing nations (OPEC+) unexpectedly announcing a significant production increase. Despite this, precious metals and agricultural commodities still show year-to-date gains, while energy and industrial metals have erased earlier progress.

Source: WisdomTree, Bloomberg Commodity Total Returns Subindices. Historical performance is not an indication of future performance, and any investments may go down in value.

We remain confident that gold and silver will recover their recent losses. These metals have been caught up in the broader market sell-off, which is typical during periods of financial stress. In such times, gold is often sold as a source of liquidity to meet margin calls and manage risk. However, history shows that once the initial wave of stress passes, gold prices typically rebound. We believe gold could hit new all-time highs this year, potentially reaching over $3,600/oz within 12 months. Silver is likely to follow suit, benefiting from gold’s momentum.

Demand destruction may make it harder for industrial and energy commodities to recover. However, there is a strong likelihood that China will implement stimulus measures to cushion the blow. While we don’t expect China to launch a stimulus on the scale of the 2008 Global Financial Crisis, it will likely double down on its current approach – combining green ambitions with economic support. Infrastructure investment, especially in the power grid, will be metals-intensive. China is expected to buy metals aggressively during price dips. That said, we are less confident the same will apply to oil.

OPEC+, for its part, has a history of misjudging demand shocks – most notably during the COVID crisis. Its recent decision to boost production during a downturn does not inspire confidence.

U.S. agricultural exports are also likely to suffer in the tit-for-tat trade war, dimming the outlook for a meaningful rebound in CME and CBOT prices. However, if agricultural tariffs become part of broader trade negotiations, there is a chance for recovery.

The global equity market has been jolted into a sharp correction following a cascade of tariff announcements that began on Liberation Day, triggering a broad risk-off sentiment among investors. The magnitude and velocity of the selloff point to a deeper shift in risk sentiment and portfolio positioning. Cyclicals and high-beta tech names have borne the brunt, while small caps and emerging markets (EM) equities – often seen as trade-sensitive – have seen outsized drawdowns. Even large cap tech, previously seen as resilient, hasn’t been spared.

Amid the turbulence, WisdomTree’s dividend and core allocation strategies have offered a beacon of stability, with key ETFs showing strong relative performance and reinforcing the value of a diversified, quality-focused approach.

WisdomTree’s two dividend-focused UCITS exchange traded funds (ETFs) – which strategically steer away from the most concentrated exposures in mega-cap growth—have held up notably well during the recent downturn. The WisdomTree US Equity Income UCITS ETF (Ticker: DHS) known to target the top 30% dividend-yielding US stocks, after filtering out lower quality and momentum stocks. The strategy’s value-tilt and sector diversification – including a stronger allocation to healthcare, financials, and consumer staples – has been key to its outperformance versus the S&P 500 Index.

The WisdomTree Global Quality Dividend Growth UCITS ETF (Ticker: GGRA) – offer access to a portfolio of high quality, dividend paying global companies by selecting dividend paying companies with the best combined rank of earnings growth, return on equity and return on assets within an ESG-filtered universe of companies with sustainable dividend policies. By maintaining a higher tilt toward the highest Return on Equity (ROE) quintiles, the strategy offers high profitability and defensibility.

The WisdomTree US Efficient Core UCITS ETF (Ticker: NTSX) also deserves attention as a diversifier during drawdowns. By combining 90% US equities with a 60% overlay in US Treasuries, it seeks to provide a capital-efficient 60/40 exposure.

As equity markets stumbled and Treasury yields dropped, NTSX benefited from:

For investors looking to stay invested without taking on excess risk, NTSX offers a modern take on core allocation – particularly relevant when market stress prompts flight to safety.

With global markets digesting a cocktail of trade disruption, economic uncertainty, and monetary ambiguity, strategies that prioritize quality, dividend sustainability, and smart diversification are standing tall. As investors recalibrate, these ETFs represent core building blocks for portfolios looking to blend income, quality, and efficient risk control in an increasingly uncertain world.

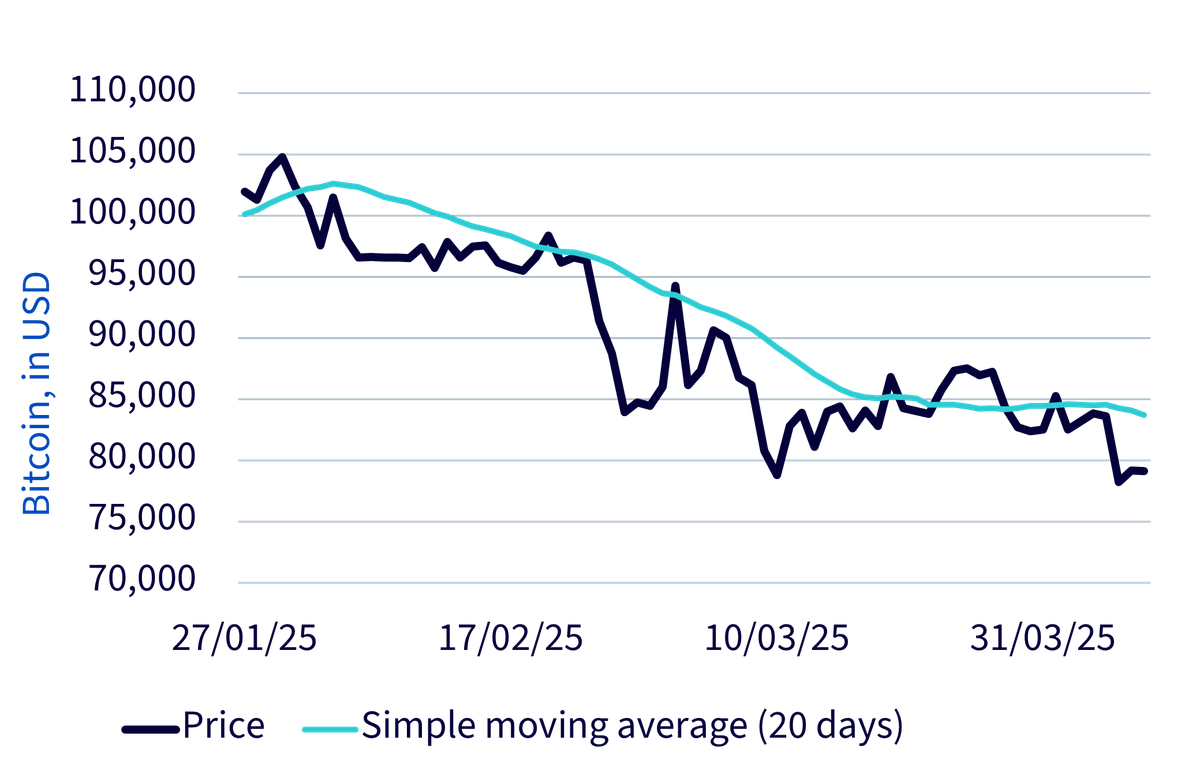

Since U.S. Liberation Day – when U.S. President Donald Trump announced unexpectedly high tariffs – bitcoin has demonstrated striking composure. While traditional markets absorbed the policy shock with volatility, bitcoin’s price action remained orderly and rangebound. Far from chaotic, its behaviour has been, in a word, disciplined.

Source: Artemis Terminal, WisdomTree. 08 April 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

This is not an isolated incident. Over the past several months, bitcoin has begun to exhibit characteristics more in line with a strategic asset than a speculative one. Volatility has moderated meaningfully, and correlations to traditional risk assets remain structurally low – making bitcoin increasingly relevant for multi-asset portfolios.

The broader context is even more compelling. The total market capitalisation of listed, investable assets globally exceeds $210 trillion1. With the cryptocurrencies’ total market capitalisation valued just under $3 trillion, they represent approximately 1.3% of the global market portfolio2. That places cryptocurrencies in line with asset classes such as high-yield bonds, inflation-linked bonds, or emerging market small-cap equities — all of which are regularly considered in strategic asset allocation models.

In this context, maintaining a zero allocation to bitcoin – a cryptocurrency that represents over 60% of total crypto market cap3 – is no longer a neutral stance. It is an active underweight decision. For allocators seeking genuine diversification and aiming to reflect the evolving structure of global capital markets, the case for at least a measured allocation to bitcoin is becoming harder to ignore.

Bitcoin is not just surviving a volatile macro environment – it is maturing through it. And that evolution is precisely what makes it more investable than ever.

1 Source: Bloomberg, WisdomTree. 31 March 2025.

2 Source: Bloomberg, WisdomTree. 31 March 2025.

3 Source: Artemis Terminal. 08 April 2025.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).