WSLV LN

WisdomTree Core Physical Silver

Published 26 January 2026

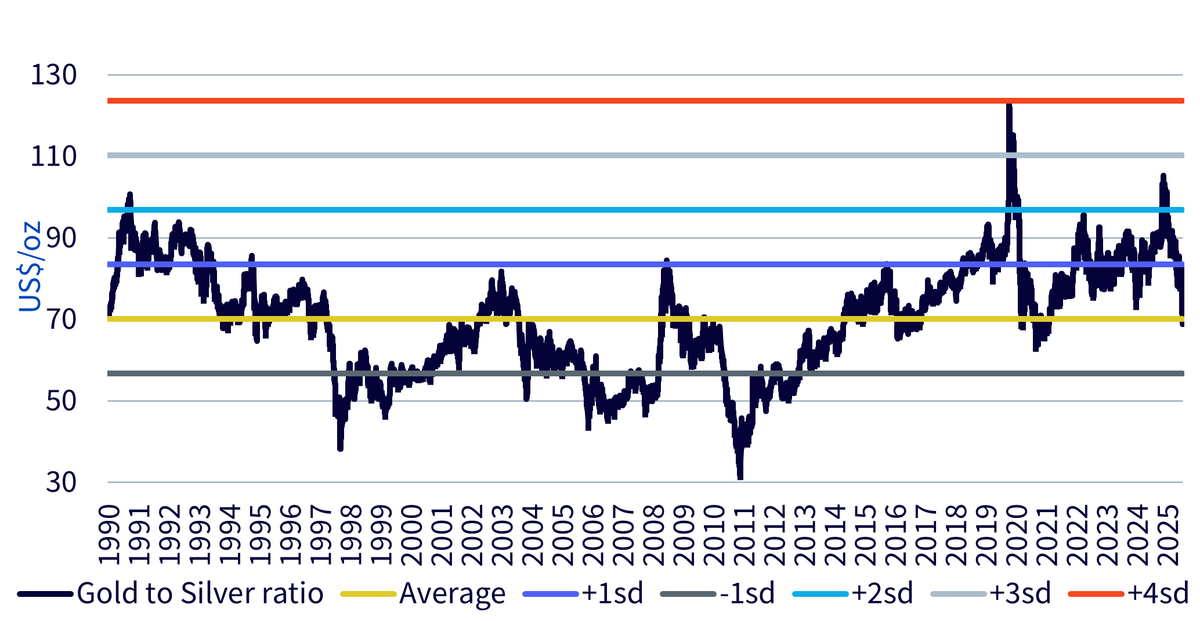

Silver has just had its best year since 1979, rising 147% in 2025. Initially led by the rapid gains in gold (which also had its best year since 1979, rising 65%), silver significantly outperformed its sister metal. The gold-to-silver ratio (Figure 1) fell from over 100 in June 2025 to under 60 by the end of the year as silver prices gained momentum. The gold-to-silver ratio has now returned to its long-term average since 1990.

It is worth noting that the monthly silver–gold beta did not rise in 2025. In fact, it fell to 0.9 from a long-run average of 1.4. However, a single year is a short period, particularly when analysing monthly data.

Source: WisdomTree, Bloomberg. June 1990 to December 2025. sd= standard deviation. Historical performance is not an indication of future performance and any investments may go down in value.

Silver has experienced multiple consecutive years of supply deficits (Figure 2), leaving supplies of the metal tight. We expect another year of supply deficits in 2026.

Source: Metals Focus, WisdomTree. 2025. (F) = Forecasts. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Despite the sharp rise in prices, miners are unlikely to produce more silver in a meaningful way. This is largely because most silver (more than 75%) is produced as a by-product of mining for other metals.

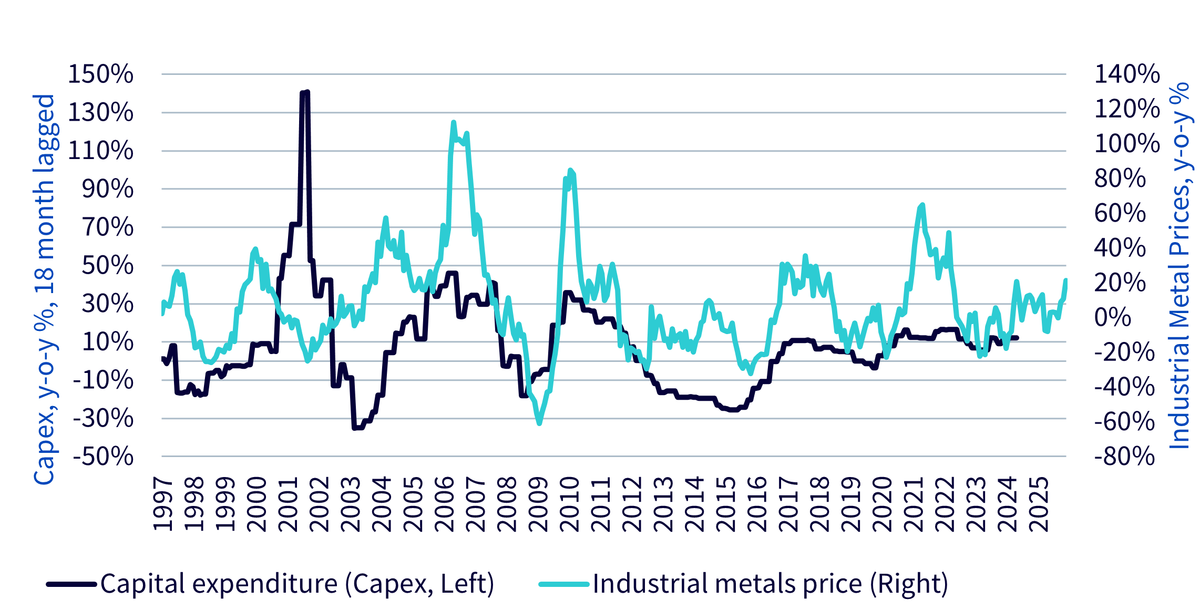

We observe a lagged relationship between mining capital expenditure and industrial metal prices (Figure 3). Capital expenditure has therefore not yet responded to the recent improvement in industrial metal prices. In copper markets, production disruptions at the El Teniente, Grasberg and Constancia operations are likely to constrain silver by-product output. Meanwhile, the Indonesian government is discussing supply constraints on nickel production and the Democratic Republic of Congo is restricting cobalt production and exports, both of which also have implications for silver by-product supply.

Source: WisdomTree, Bloomberg, February 1996 to December 2025. Historical performance is not an indication of future performance and any investments may go down in value.

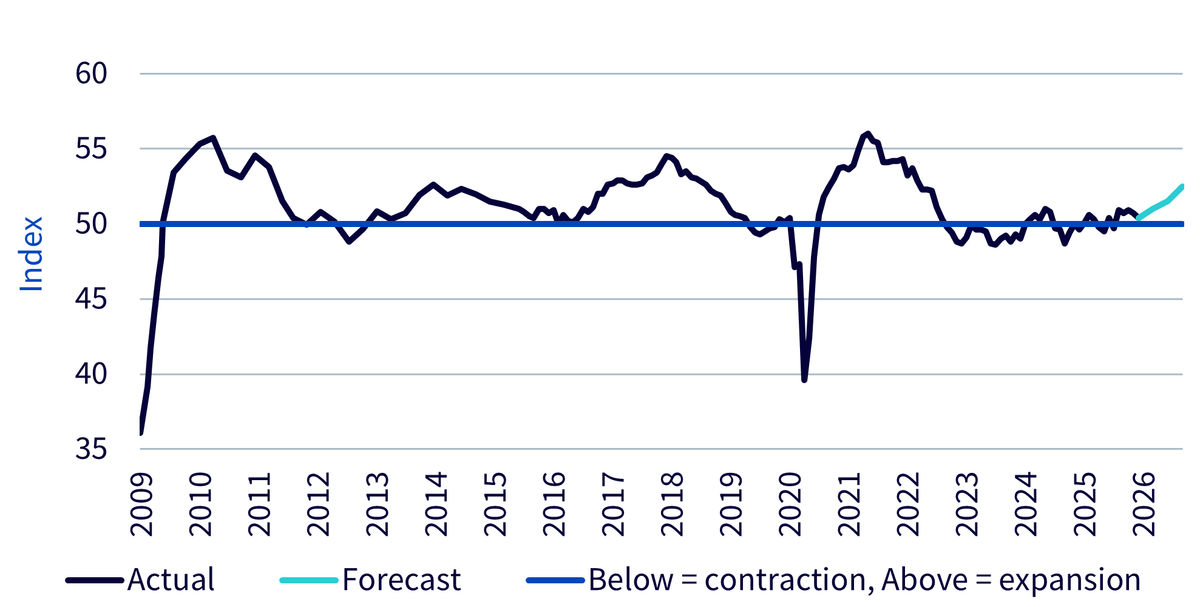

We expect a pickup in industrial activity in 2026, despite the moderating Purchasing Managers’ Index (PMI) readings seen in recent months (Figure 4). As interest rate cuts spur economic activity, we expect PMIs to rise, which should be supportive of silver demand.

Source: WisdomTree, Bloomberg, S&P Global, Historic: May 2009 to December 2025. Forecasts: January 2026 to December 2026. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

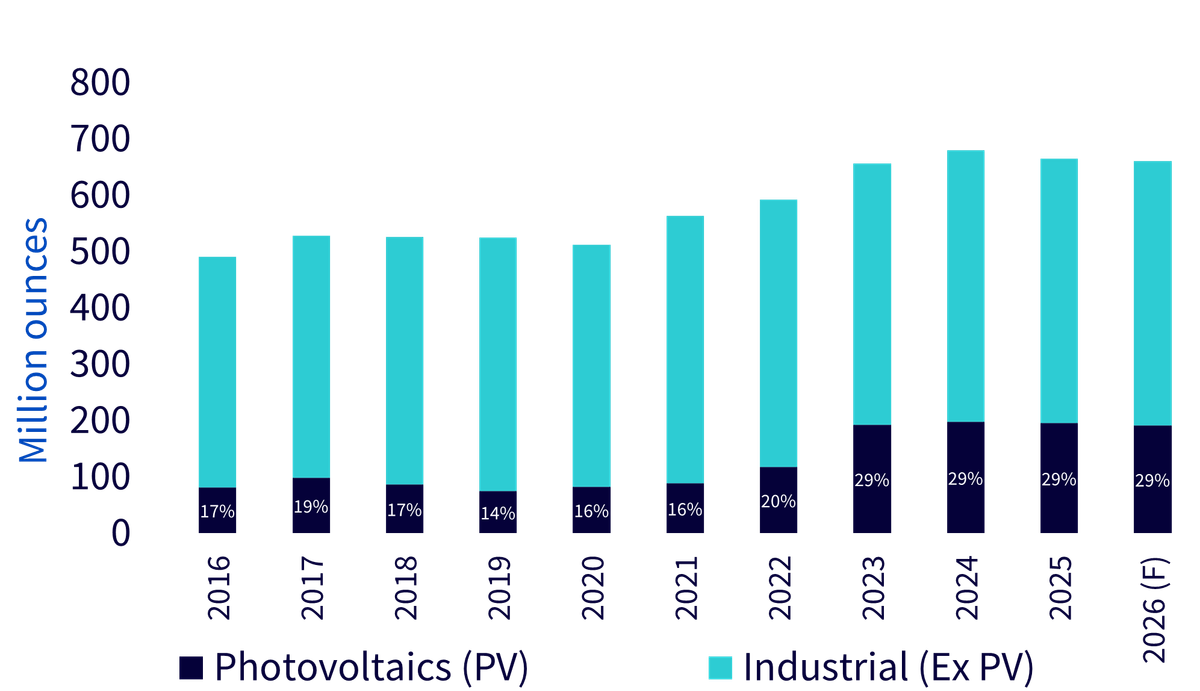

However, following the rapid rise in prices, some degree of silver thrifting is likely. We expect sustained growth in solar installations, but reductions in silver loading may have a net negative impact on silver demand in photovoltaic (PV) applications.

Silver demand in photovoltaics reached a record high in 2024, at just under 200 million ounces (Figure 5). It likely slipped from that peak in 2025 to around 196 million ounces and could decline further in 2026, to approximately 191 million ounces, as technological shifts support increased thrifting.

Source: Metals Focus, WisdomTree. 2025. (F) = Forecasts. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Since 2022, manufacturers have increasingly adopted copper-cored silver pastes for heterojunction (HJT) and Tunnel Oxide Passivated Contact (TOPCon) cells. This has reduced silver content from over 50% in 2023 to just 10–15% by mid-2025, without compromising efficiency.

Further silver savings are emerging from:

Collectively, these developments could reduce silver consumption per watt by 15–20% in 2026, marking a pivotal shift towards more cost-efficient, copper-based PV production.

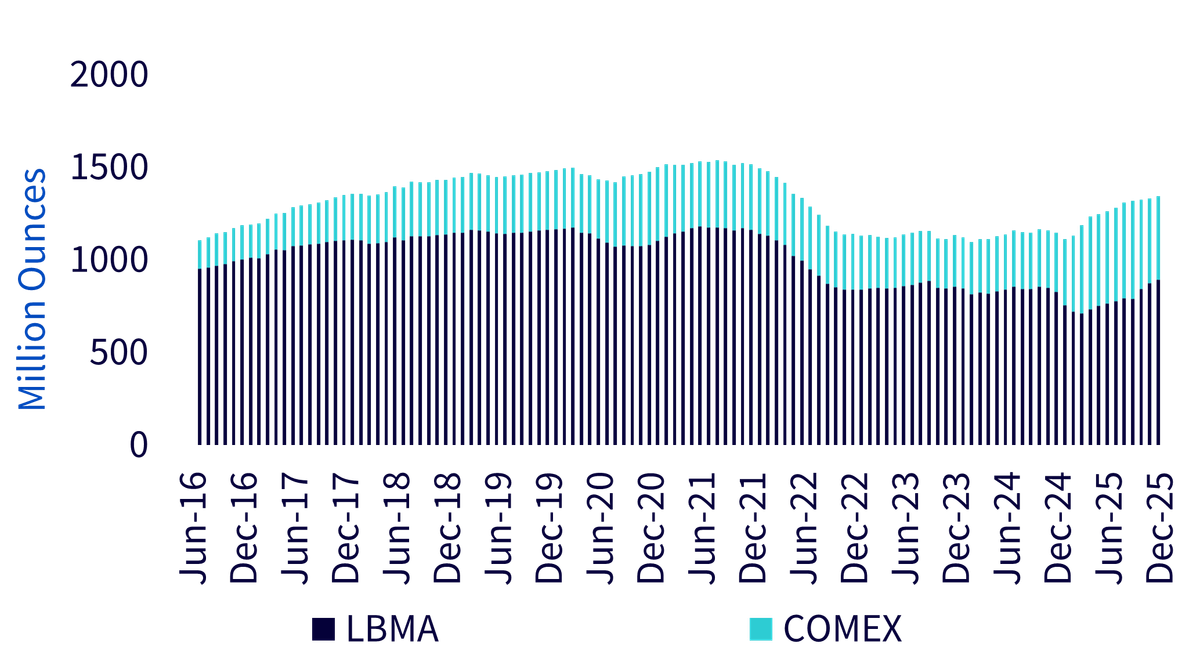

Concerns that the United States would implement tariffs on silver imports drove inventories into the US in 2025, as traders attempted to get ahead of this risk. Figure 6 shows that Commodity Exchange (COMEX) vault inventories rose during the year, while London Bullion Market Association (LBMA) inventories initially declined.

Although LBMA inventories recovered by the end of the year, following sharp price differentials, COMEX inventories remain elevated. This suggests that significant quantities of silver that were previously held outside both LBMA and COMEX vaults have entered COMEX facilities. Additional silver may also have moved into off-exchange vaults within the US.

While no tariffs were applied in 2025, silver’s inclusion in the United States Geological Survey’s (USGS) list of Critical Minerals for the first time has fuelled speculation that it could be subject to future sectoral tariffs. A Section 232 investigation into processed critical minerals, a broad category that now includes silver, was formally initiated by the US Department of Commerce in April 2025.

The Department of Commerce has up to 270 days from the initiation of the investigation to deliver its final report and recommendations to the President, although no public announcement of delivery has been made. Government shutdowns are likely to have delayed the process. Adding the 90 days the President has to respond to the recommendations, a decision could be imminent.

Our base case is that silver will not be subject to tariffs. As a result, there is some short-term downside risk to prices, but this should be quickly offset by silver’s correlation with gold, ultimately allowing silver prices to end the year higher.

Source: WisdomTree, Bloomberg LBMA. June 2016 – December 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

Silver typically acts as a leveraged proxy for gold. Our models indicate a beta of 1.4, meaning that if gold prices rise by 1%, silver prices tend to increase by around 1.4%, all else being equal.

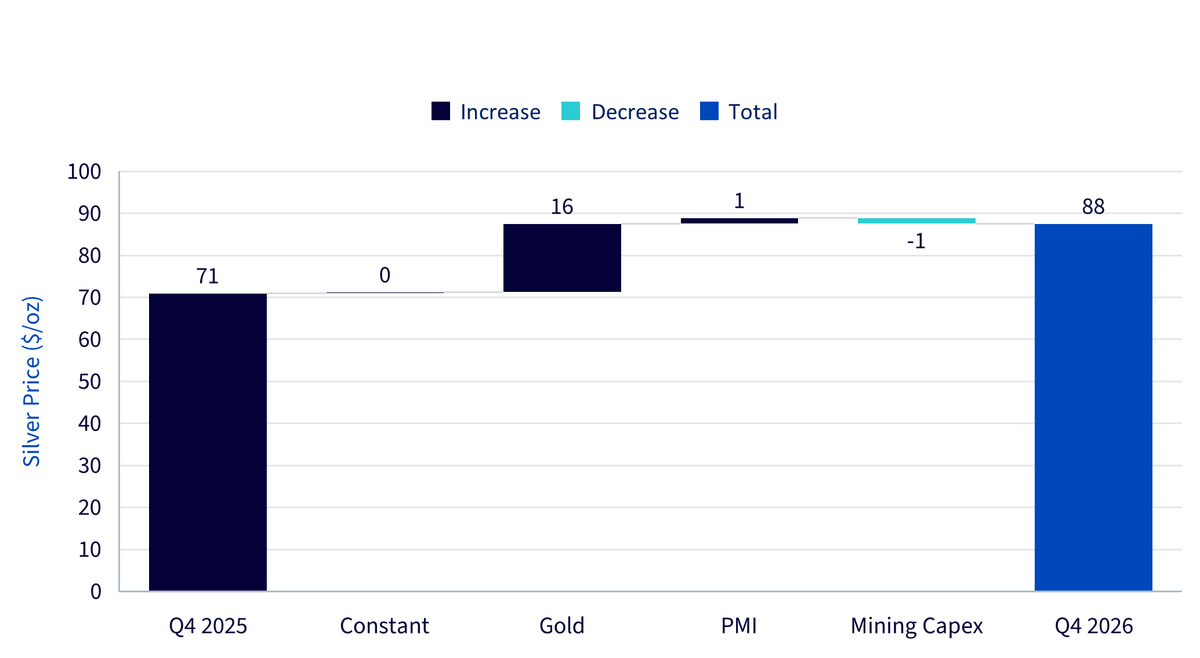

As outlined in our recent Gold Outlook, gold prices are expected to reach $5,020 per ounce by Q4 2026 under our consensus scenario. This reflects continued strong sentiment towards the metal amid concerns about fiscal dominance and inflation, which is moderating but remains above Federal Reserve targets.

Using our gold-linked model, we forecast silver prices to rise to $88 per ounce by Q4 2026. Most of the gains in silver prices are driven by their beta to gold. An improving industrial backdrop, which supports demand, may be partially offset by a modest increase in mine supply over this forecast period.

Source: WisdomTree, Bloomberg. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Looking ahead to Q4 2026, silver remains well supported by a combination of tight supply conditions, a constructive macro backdrop, and its strong linkage to gold. While higher prices are likely to encourage further thrifting in industrial applications, particularly in photovoltaics, these efficiency gains are unlikely to fully offset demand growth amid an improving economic environment. With supply constraints persisting and gold expected to continue its upward trajectory, silver prices are well-positioned to move higher over the forecast horizon.

WisdomTree Core Physical Silver (WSLV) provides low-cost (0.19% management fee) access to silver. The product is physically backed, meaning performance is linked to the spot price of silver rather than futures-based pricing, and therefore does not involve futures roll or swap costs.

WisdomTree Silver EUR daily Hedged (ESVR) provides a synthetic exposure to rolling silver futures prices with a currency hedge. Movements in the currency hedge can influence returns, particularly during periods when changes in silver prices coincide with fluctuations in the US dollar.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.