Silver outlook: Searching for a silver lining

Published 2 July 2018

We have updated our silver model, incorporating our new gold price forecasts. Just like gold, silver has the potential to flat-line over the course of the next year. However, we propose a number of reasons why silver could defy the model-based trajectory, including increasing growth in its use in vehicles and a rise in photovoltaics. Supply disruptions could also create some upside price momentum.

In Gold and silver: similar, but different, we argued that silver’s price performance is 80% correlated with gold. In our modelling framework, gold price is therefore the main driver of silver price. However, we find the following variables as important drivers of silver price:

- Growth in manufacturing activity – more than 50% of silver’s use is in industrial applications (in contrast to gold where less than 10% comes from that sector). We use global manufacturing Purchasing Managers Index (PMI) as a proxy for industrial demand

- Growth in silver inventory – rising inventories signal greater availability of the metal and hence is price negative. We use futures market exchange inventory as a proxy

- Growth in mining capital investment (capex) – the more mines invest, the more potential supply we will see in the future. Thus, we take an 18-month lag on this variable. Given that most silver comes as a by-product of mining for other metals, we look at mining capex across the top 100 miners (not just monoline silver miners)

Inputs shaping our view

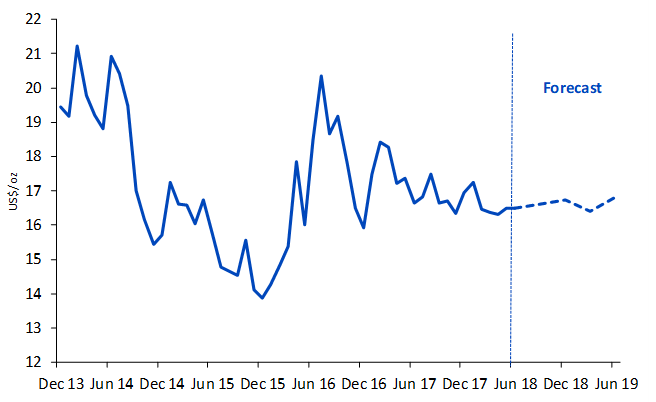

We expect Global Manufacturing PMIs to decline after seeming to have peaked at the beginning of this year. Silver exchange inventory has risen strongly in the past few years. We expect that growth to plateau over the coming year. Lastly mining capex has shown signs of revival in recent months. Although we use an 18-month lag in our model (when capex was still declining), the pace of decline was significantly smaller than a few years ago. Incorporating these views into the model along with gold’s trajectory we have already expressed views on, silver prices are likely to end June 2019 at US$16.8/oz.

Figure 1: Silver price forecast

Source: Bloomberg, WisdomTree, data available as of close 05 June 2018. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Past performance is not indicative of future results. You cannot invest directly in an Index.

If we were to incorporate either the bear or bull scenarios for gold in our simulated model, silver would rise or fall in accordance with those scenarios.

Structural breaks not incorporated in our model

We believe, there may be a number of structural changes, that cannot be picked up by the model but could see prices trade higher. Below are a few examples.

Automobile electrification

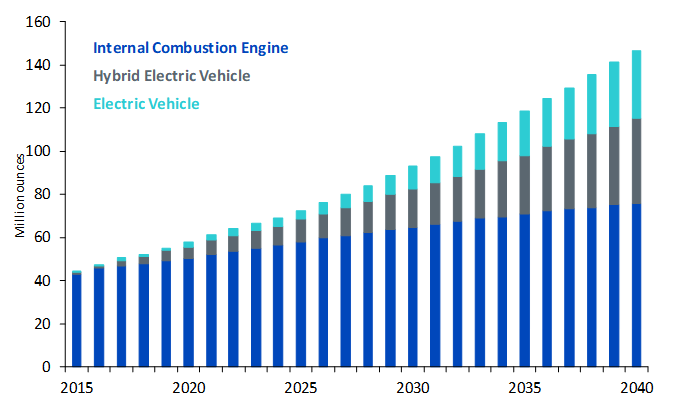

The expected growth in electric vehicles could see demand for silver rise in a similar fashion to nickel (see Nickel - electrification may boost demand). Silver is used in both internal combustion vehicles and electric vehicles. Automotive manufacturing used approximately 50 million ounces (Moz) of silver in 2017 (source: World Silver Survey 2018). That is more silver than that used by the photographic industry (44 Moz) and close to the amount of silver consumed in silverware (58 Moz) (source: World Silver Survey 2018). Silver used in automotive electronics account for more than a fifth of all silver use in electronics (243 Moz) (source: World Silver Survey 2018). As silver is primarily used in electrical connections, the electrification of vehicles is likely to see its use increase electric vehicles and autonomous vehicles have more circuitry that utilise silver compared to traditional cars.

Figure 2: Automotive silver demand forecasts

Source: GFMS Thomson Reuters, Silver Institute, WisdomTree, data available as of close 06 June. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Solar energy

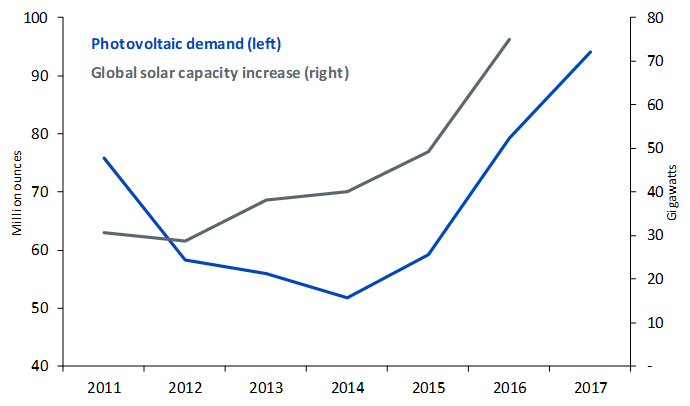

Silver use in photovoltaics (solar panels) has been the strongest source of silver demand growth of all industrial uses. Growing concerns about the environmental impact of fossil fuel consumption and aspirations to decarbonise after the Paris Agreement on Climate Change in late 2015 have acted as catalysts behind alternative sources of energy. Although many governments have reduced subsidies for solar power technology over the past decade, falling costs have improved their stand-alone economics and solar installations are rising. A few years ago, silver use in photovoltaics fell as manufacturers were “thrifting” (i.e. finding technological solutions to putting less of the metal in to save costs), but it appears that effort has now reached technological limits and silvers’ use will grow in line with installations. We acknowledge that relying on solar installation growth to fuel silver demand growth is risky – for example the US has imposed punitive tariffs on imports of Chinese solar panels which could dent their deployment – but with demand so strong, we believe that US companies will rebuild their solar panel manufacturing capabilities.

Figure 3: Photovoltaic silver demand

Source: BP, GFMS Thomson Reuters, Silver Institute, WisdomTree, data available as of close 06 June.

Historical performance is not an indication of future performance and any investments may go down in value.

Supply disruptions in trade wars

Mexico is the world’s largest producer of silver and accounts for close to half of US imports of silver. The country is at the brunt of protectionist pressures from the US. Beginning in June 2018 the US imposed tariffs on steel and aluminium imports from Mexico, Canada and EU. Silver is not included, but there is a risk that if a tit-for-tat trade war breaks out, silver could fall into the crosshairs. Mexico is placing tariffs on US steel and farm products and the EU is thinking about implementing “rebalancing measures”. These events indicate that trade-war appears to be escalating. A disruption to the global silver supply chains has the potential to raise its price in a similar manner to which we have seen steel and aluminium prices rise.

Conclusion

Based on our view that global PMIs have likely peaked, mining capex is no longer declining and exchange inventories may not fall after having risen in the past few years, silver has the potential to flat-line in line with gold. But there are a number of structural shocks that could allow silver to break out of our model-based trajectory. Growing silver demand from the auto industry as the number of electronic connections in vehicles increase could push prices higher. Falling costs of solar panels has seen its adoption increase and silver usage is unlikely to be thrifted further. Greater aspirations for reducing environmental damage could see photovoltaic use continue to increase. Lastly, even though we expect mining capex to rise, it does not rule out supply disruptions not least from an emerging trade war.

Related blogs

+ Gold outlook - gold to flatline out to June 2019 in the absence of shocks

Categories

About the contributor

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.