Japan offers an avenue in a violent global value rotation

Published 17 May 2022

2022 has marked a turn of events for Japan. The once regarded safe haven yen, has declined the most (-11.3%) among G101 currencies this year2. A large part of the Yen’s decline is rooted in the widening of policy divergence between the US and Japan.

China, alongside Japan, is the only real major economy easing policy in 2022. The Bank of Japan (BOJ) also recently announced unlimited buying of 10-year Japanese government bonds (JGBs) to stem any movement higher in long-term borrowing costs above 25 basis points (bps). This divergence in policy stance is even more apparent with the Federal Reserve’s (Fed) plan to reduce its large balance sheet through a “fast runoff” that might pressure the long end of the US yield curve higher. Historically very low interest rates in Japan made borrowing in Yen attractive. But now with other currencies in a similar position of offering zero (or negative) rates on the currency many years out, the Yen lost its competitive edge on the famous carry trade.

Source: Bloomberg, WisdomTree as of 11 May 2022

Historical performance is not an indication of future performance and any investments may go down in value

Hedging costs are now rising along with global short-term rates, particularly in the US. This could cause even more Yen selling as investors’ demands for US dollars increase, and they seek the higher levels of interest rates available in the US markets without hedging the currency’s movements.

The weaker Yen bolsters the case for Japanese exporters

The weaker Yen has widespread implications for the Japanese equities since Japan is a market that generates a large portion of its revenue from global markets. So, a weaker Yen supports its profit outlook, thereby making Japanese exporters more competitive than global peers. This theory was validated on March 25, in an address to the Japanese parliament by the Bank of Japan Governor Haruhiko Kuroda who said, “There is no change in the basic structure that a weaker yen has positive effects on the Japanese economy by pushing up the overall economy and prices.” A January report from the BOJ estimated that a 10% depreciation in the yen would push up Japan’s gross domestic product (GDP) by 1%3.

Source: Factset, WisdomTree as of 31 March 2022. Europe = MSCI Europe Index. U.S. = S&P 500 Index. Emerging Markets (EM) = MSCI EM Index. Japan = MSCI Japan Index. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value

Japan’s energy sector to witness a shift to nuclear power

While much of the attention remains on the weaker Yen’s impact on exporters, it’s important to note that a weaker Yen also raises the costs of imports. Japan’s trade deficit widened to US$3.2Bn in March largely due to soaring energy costs. However, Russia’s war in Ukraine strengthens the case for Japan to shift its energy policy in favour of restarting nuclear power. During a speech in London on May 5, Prime Minister Fumio Kishida said that Japan would turn to its nuclear reactors to help reduce the country’s dependence on Russian fuel. He asserted Japan’s commitment to carbon neutrality by 2050 and the goal of reducing greenhouse gas emissions by 46% by 2030 while ensuring a stable energy supply.

Growth in Japanese dividends lure investors

Inflation has remained worryingly high in the US and Europe and surprisingly low in Japan. Owing to which, high dividend paying strategies have thrived in 2022. Interestingly, since the pandemic, Japanese dividends have grown more than major regions from the US to Europe and emerging markets. While European dividends have contracted more than 10%, Japanese dividends have grown almost 18%, measured in local currency terms. Given the conservative pay-out ratios of Japanese companies—which helped buffer dividend cuts in 2020—Japan tends to have a lower dividend yield than Europe, where dividend payments can be more cyclical.

Sources: WisdomTree, MSCI, as of 31 March 2022. Dividend growth measured by respective MSCI regional indexes. Dividend growth measured in local currency. You cannot invest directly in an index.

Past performance is not indicative of future returns.

Adopting a hedged Japanese exposure

Amidst rising geopolitical risks, Japanese equity markets performance have withstood the ensuing volatility better than most of its developed market peers in 2022 in local currency terms. However, when measured in foreign currency terms i.e., the US dollar or EUR terms the losses are magnified on the downside due to the weakness of the Yen (as shown below).

Source: Bloomberg, WisdomTree as of 11 May 2022

Historical performance is not an indication of future performance and any investments may go down in value

This goes to a point we often make - currency changes do not need to impact your foreign return, and you can target that local market return by hedging your currency risk. A hedged Japanese dividend paying equity exposure could enable an investor to hedge their exposure to the Yen. Valuations remain attractive both historically and compared to developed markets. US equity earnings multiples are trading at a 20% premium while Japan is priced at a 15% discount to its historical medium . The ensuing rotation from growth to value remains an attractive environment for value-oriented cyclical and industrial companies which are dominant in Japanese equity markets.

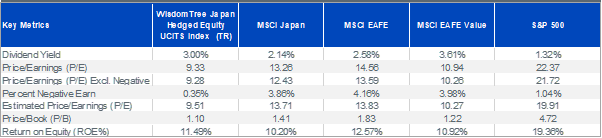

Examples of Fundamentals in Japanese Indices

Source: Bloomberg, WisdomTree as of 31 March 2022.

Historical performance is not an indication of future performance and any investments may go down in value

1 The Group of Ten or G10 is a group of 11 industrialized nations that have similar economic interests.

2 Bloomberg from 31 December 2021 to 11 May 2022.

3 “Outlook for Economic Activity and Price,” Bank of Japan, January 2022.

Related blogs

+ Commodity exporting currency AUD wins, while haven YEN loses its mojo

+ Green shoots emerging for Japan

+ Japan steps up as Suga steps down

Related products

+ WisdomTree Japan Equity UCITS ETF - USD Hedged (DXJ)

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.