What's Hot: Industrial Metals – Is this the entry point investors were waiting for?

Published 13 May 2022

Market downturns are often referred to as ‘corrections’. This can be problematic because it suggests that the new lower price is correct and the higher price previously was incorrect. An alternative framing would be that markets have revised their assessment of risks and rewards and come to a new price. Industrial metals have just experienced such a revision. But sharp revisions can also result in overshoots. Does that mean an attractive entry point has opened up for investors?

What has caused the pullback?

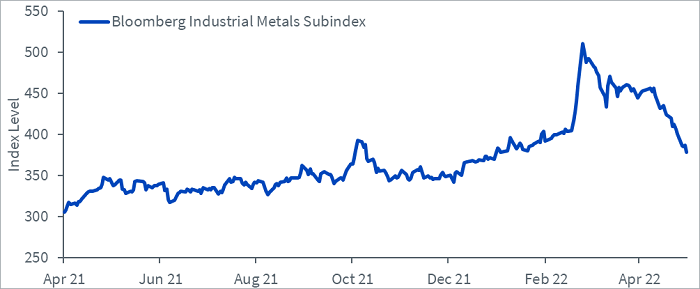

Industrial metals have pulled back sharply over the last month, and the price level for the Bloomberg Industrial Metals Subindex has reverted to pre-Ukraine conflict levels (see figure below). This is not particularly surprising. The geopolitical risk premium that was being priced into industrial metals at the start of the conflict has eroded as investors perceive the risk of outright bans on Russian industrial metal exports to be relatively low. This is not to suggest that the uncertainty facing the sector has evaporated. The conflict continues, and it is difficult to predict what sanctions may be imposed in the future.

Figure 1: The Industrial Metals basket has now returned to pre-conflict levels

Source: WisdomTree, Bloomberg. Data as of 12 May 2022. Based on the total return index.

Historical performance is not an indication of future performance and any investments may go down in value.

While the geopolitical risk premium was largely expected to fade away ultimately, the pace at which industrial metals have pulled back has taken many by surprise. Apprehensions of an impending recession in major economies have created a risk-off sentiment in markets – something industrial metals are certainly not immune to. Such worries have been augmented by the slowdown in China from renewed lockdowns. Markets often use Manufacturing Purchasing Managers’ Indices (PMIs) from the world’s biggest consumer of industrial metals as a proxy for the near-term outlook of the asset class. China’s Manufacturing PMI fell into contractionary territory in March and went deeper still in April.

So, is it an entry point then?

A mere drawdown in prices would not qualify as a potential entry point. If, however, there are grounds for optimism, in the long run, an over-extrapolation of a bearish run at any point can indeed create an attractive entry point for investors.

At WisdomTree, we have been arguing how two key shifts have created structural demand growth drivers for industrial metals in recent months. The first is the renewed focus from major economies on investing in infrastructure to induce economic growth. With rates now on the rise and thus support from monetary policy eroding quickly, this has become more important than ever before.

Second is the inevitable energy transition. According to Wood Mackenzie, the annual demand for copper is expected to rise from around 23 million tonnes (MT) in 2020 to around 43MT per annum in 2040, with green technologies including electric vehicles, renewable power, energy storage, and charging infrastructure largely responsible for the uptick. Similar growth trajectories are forecasted for aluminium and nickel, and there is optimism around the demand growth for other metals, including zinc, tin, platinum, silver, and even gold.

But what to do about contango?

Since investors typically access industrial metals through futures, roll returns make an important contribution to total returns. The normal state for an industrial metal is contango (higher futures prices than spot prices). Contango is the price holders of futures pay for the convenience of not having to store the physical commodity. In recent weeks, particularly since the start of the conflict, many industrial metals went into backwardation (higher spot prices than futures prices) due to expectations of acute supply tightness. This backwardation was offering investors the bonus of a positive roll yield. With a few industrial metals now back in contango, should investors be worried about the impact of negative roll yields?

The bottom line is that many industrial metals being deep in backwardation is unusual and would generally occur when prices are inflated – as was the case when the conflict started. It is just not possible for metals to be attractively priced and still be in deep backwardation. But caveats must be offered here. When there is market volatility, future contract curves can change their shape quickly. Some metals, like tin, are still in backwardation, whereas others, like aluminium, may have gone into contango at the front end of the curve but are in backwardation when you look further along the curve.

Ultimately, industrial metal could bounce back quickly if the bearish risk sentiment prevailing in markets turns and China opens up again. And then focus will return to the long term drivers of industrial metal demand.

Related blogs

+ Energy Transition Commodities: Price Resilience to Economic Slowdown

Related products

Categories

About the contributor

Director, Research

@MobeenTahirWTMobeen is a member of WisdomTree’s research team where he focuses on a wide range of asset classes to offer strategic and tactical insights to our clients on global markets and investment products. Before joining WisdomTree in December 2018, Mobeen worked at Willis Towers Watson as an investment consultant advising institutional clients as well as their in-house fund business on asset allocation and portfolio construction with his research focus being equity and multi-asset smart beta. Mobeen has a BSc (Hons) in Accounting and Financial Management from Loughborough University and an MSc in Accounting and Finance from the London School of Economics and Political Science. He is also a CFA Charterholder.