AIGI LN

WisdomTree Industrial Metals

Published 12 April 2024

The Bloomberg Commodity Industrial Metals Index has risen 6.9% in April 2024 so far (28/03/2024 - 11/04/2024) following a decline in the first quarter of this year. Could this be a turn in the industrial metals cycle?

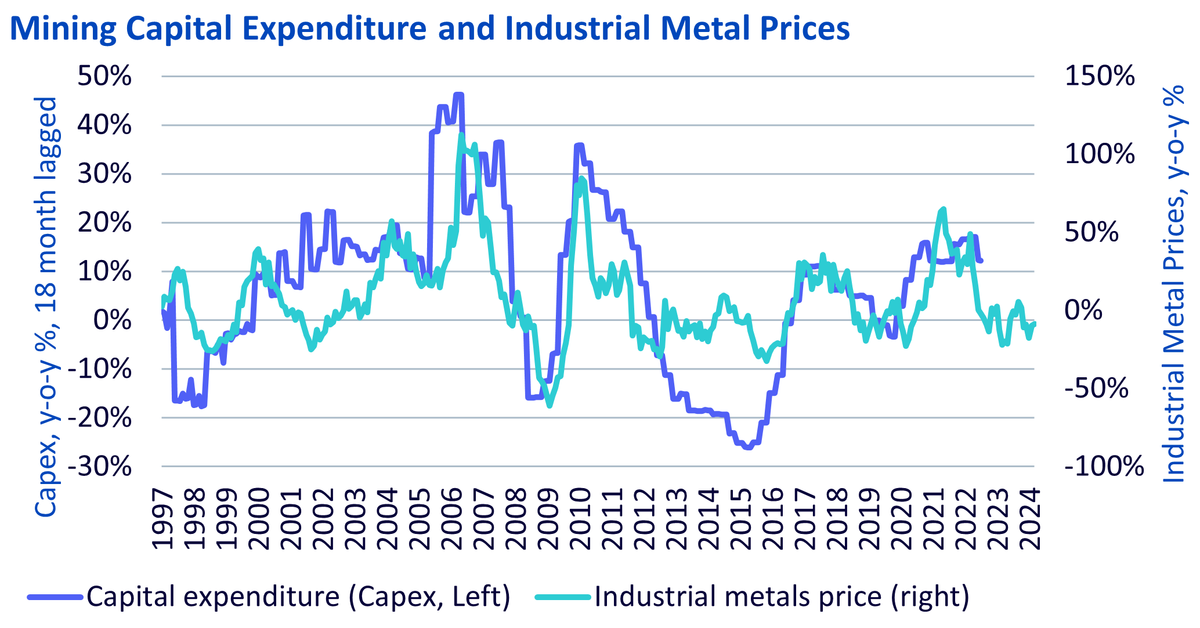

There is an adage that the cure for low prices is low prices. We are seeing that play out in industrial metals. With industrial metal prices having suffered through most of 2023, supply restraint from miners and smelters has become the response and as a result, industrial metal prices have started to regain some lost ground. As the chart below shows, capital expenditure tends to lag industrial metal prices. Up until recently, capital expenditure in mining activity was accelerating, but in the last quarter we saw a deceleration (albeit still positive year-on-year growth). That deceleration in capex, combined with other signs of supply restraint could mark the turning of the industrial metals price cycle.

Source: WisdomTree, Bloomberg, February 1997 to March 2024. Historical performance is not an indication of future performance and any investments may go down in value.

In January, First Quantum Minerals Ltd announced that it would suspend nickel mining at Ravensthorpe and only process stockpiles. Panoramic Resources Ltd also announced that it would suspend its nickel mining operations at its Savannah mine. Then mining giant BHP announced plans to shut down its Nickel West operations. All these projects are in Australia.

However, the main source of oversupply is from China and Indonesia in low quality nickel suitable for Nickel-Pig-Iron (NPI). We believe nickel output could be cut by 100,000 metric tons this year as producers seek to limit losses following a slump in the price of the metal.

Koniambo Nickel SAS (KNS) – a joint venture between Société Minière du Sud Pacifique SA (SMSP) and another mining giant Glencore plc –made the decision to transition KNS into care and maintenance in February 2024. Even with the French government’s proposed assistance, high operating costs and weak nickel market conditions would have meant that KNS would be an unprofitable operation.

In March, China’s top copper smelters agreed to jointly embark on production cuts at some loss-making plants as they seek to cope with a shortage of raw material. That exemplifies the juxtaposition between tight raw material availability and weak prices – a situation hard to maintain.

Chinese smelters had been rapidly expanding their capacity over the past year to get ahead of an expected surge in copper demand from sectors related to the green energy transition such as electric vehicles or wind and solar energy. But several mine disruptions globally, including the shutdown of the big Cobre mine in Panama owned by First Quantum, have meant copper concentrate is now in short supply.

Industrial metal prices opened the year weighed by ongoing concerns around the Chinese economy. The new GDP growth targets set in early March 2024 for China were initially met with scepticism as they were not supported by a new bout of stimulus. However, Chinese Manufacturing Purchasing Managers Indices appear to be rebounding (with the latest reading above the crucial 50 demarcation between contraction and expansion).

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.