A Return to King Dollar Policy - Implications

Published 3 April 2018

Global Head of Research

One of the most important macro stories of the last 15-months has been the dramatic decline in the US dollar. This has helped spur international equity indexes that package foreign currency returns on top of the equity investments.

Source: WisdomTree, Bloomberg, from 16/3/2016-18/3/2018. You cannot invest directly in an Index.

Past performance is not indicative of future results.

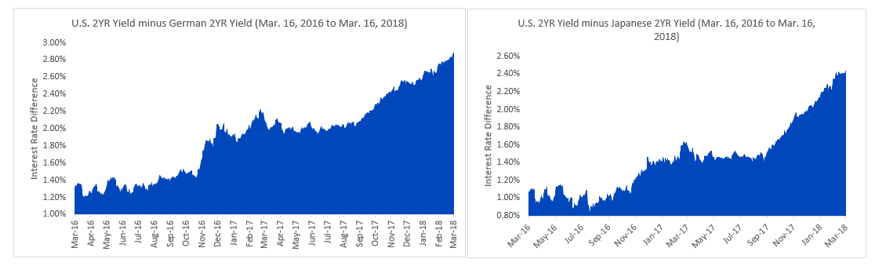

When you look at historical factors that drive currency movements, interest rate differentials are important, and the recent environment has been one where the US Federal Reserve (Fed) has been hiking interest rates while the major developed market central banks in Europe and Japan have kept short-term rates in negative territory. This makes the collapse of the dollar all the more interesting and perhaps surprising.

Differences between US and German or Japanese 2 Year Yields haven’t just Risen—They’ve more than DOUBLED in Favor of the US dollar (Mar. 16, 2016 to Mar. 16, 2018)

Source: WisdomTree, Bloomberg, from 16/3/2016-18/3/2018. You cannot invest directly in an Index.

Past performance is not indicative of future results.

The best explanation for what has been happening in our view is politically motivated uncertainty around whether US policy actions were going to favour a weaker dollar environment with less capital flows and investments into the US.

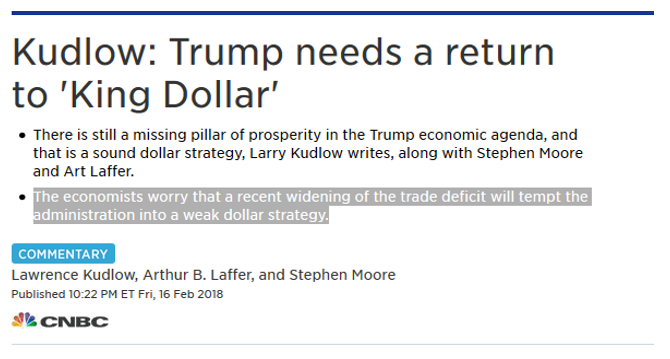

The changing guard in the White house, with Gary Cohn out as Trump’s primary economic adviser and the insertion of Larry Kudlow may be ushering in a very important strategic change in the currency markets and sentiment. In February, Larry Kudlow and fellow authors Stephen Moore and Art Laffer authored the following story:

Some excerpts from Kudlow’s article:

The Trump Administration and the Republicans in Congress have passed one of the best pro-growth tax bills ever. The Tax Cuts and Jobs Act ranks in the all-time hall of fame of legislation, along with Ronald Reagan's 1981 and 1986 Tax Acts and John F. Kennedy's posthumous tax cuts of 1964…..

When this is combined with President Donald Trump's deregulation agenda, we see no reason why the economy cannot grow for a sustained period at 3 to 4 percent growth — up from 1.6 percent in Obama's last year. But there is still a missing pillar of prosperity in the Trump economic agenda, and that is a sound dollar strategy.

The dollar weakened in 2017 and we want it stabilized.

… under Reagan the US dollar increased by 67 percent in value on foreign exchange markets through 1985. The price of gold, interest rates, and inflation all fell as well from double-digit inflationary highs, while the American economy reignited and the stock market launched its 18-year bull market.

Or, go back further in time. In May of 1962, President Kennedy's Revenue Act was passed and he reaffirmed that the US dollar was as good as gold — thus launching the incredible boom called the 'Go-Go Sixties'.1

A change in tone from the White House economic team that welcomes a strong dollar environment could challenge investors in the international investing world.

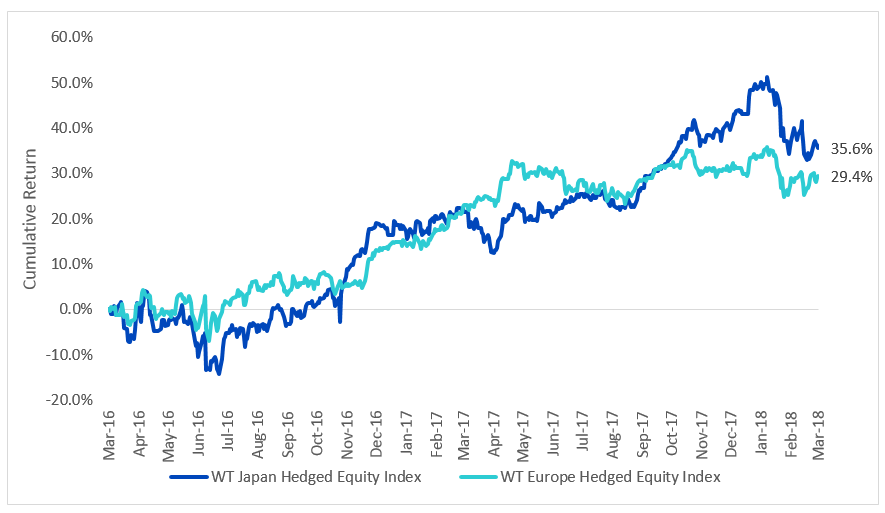

Don’t Forget about Global Export-Tilted Strategies

Now, the US economy does in fact remain the world’s largest consumer market, so a weakening dollar has created a short-term environment that has been more challenging for global multi-national companies that export into the US. Why? Well, a weaker dollar makes these imports into the US (exports from Europe, Japan and other regions) more expensive for US consumers.

Some of WisdomTree’s most widely followed strategies focus on global multinational exporters in Europe (WisdomTree Europe Hedged Equity Index) and Japan (WisdomTree Japan Hedged Equity Index). Over this two-year period, we know that the dollar generally weakened, creating, on the face of it a fairly challenging environment for these companies.

Source: WisdomTree, Bloomberg, from 16/3/2016-18/3/2018. You cannot invest directly in an Index.

Past performance is not indicative of future results.

- For context, the S&P 500 Index returned only 41% cumulatively over this same period. True, these Indexes of export-tilted stocks underperformed this widely followed benchmark, but it’s notable that the US dollar’s move was less than ideal during this period.

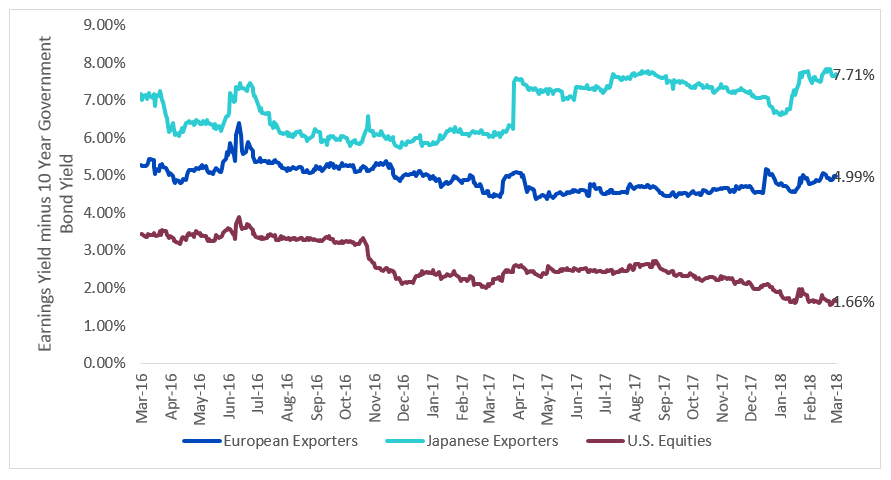

Why WisdomTree Keeps Focusing on Japan Despite the Yen’s Strength (Earnings Yield minus 10-Year Government Bond Yields)

Source: WisdomTree, Bloomberg, from 16/3/2016-18/3/2018. European exporters: WisdomTree Europe Hedged Equity Index. Japanese exporters: WisdomTree Japan Hedged Equity Index. US Equities: S&P 500 Index. Each equity index earnings yield has its respective 10-Year government bond yield subtracted from it.

Past performance is not indicative of future results. You cannot invest directly in an Index.

- As of this writing, the Yen was trading at a level of 105-106 to the US dollar and had exhibited the most strength of any of the G10 currencies when measured YTD 2018 through March 16th. So, why would WisdomTree ever focus on a basket of export-oriented Japanese equities? Well, the Japanese central bank remains the most aggressive of all global Central Banks and that contributes to a 6.93% differential between the earnings yield of the Japanese Exporters and the 10 Year government bond yield of Japan.

This is the illustration of a central bank encouraging the attractiveness of risky assets in Japan.

The US Dollar is one of the Most Important Strategic Questions in 2018

While we cannot say for sure what any currency will do, much less the dollar, before it happens, we do believe that the dollar’s movement—whether this downturn proves transitory or more long-lived—will have major implications for global asset allocation in investor portfolios. If Kudlow’s appointment triggers an inflection point, WisdomTree’s export-tilted strategies may become more interesting in short order.

1 https://www.cnbc.com/2018/02/16/kudlow-trump-needs-a-return-to-king-dollar.html

You may also be interested in reading…

+ All Eyes on the BOJ: From Down-Cycle Risks to Stimulus Action?

+ Drivers of Japan's equity performance may be changing

Related products

+ WisdomTree Japan Equity UCITS ETF - USD Hedged

+ WisdomTree Japan Equity UCITS ETF - CHF Hedged Acc

+ WisdomTree Japan Equity UCITS ETF - GBP Hedged

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.