WBLD LN

WisdomTree Europe Infrastructure UCITS ETF - EUR Acc

Publié le 18 juin 2026

Senior Associate, Quantitative Research and Multi Asset Solutions

A new theme is gradually moving to the centre of Europe’s industrial debate. For much of the past decade, the focus was on how quickly the region could decarbonise. Today, policymakers are increasingly concerned that Europe is losing ground to other major economies in strategic industries.

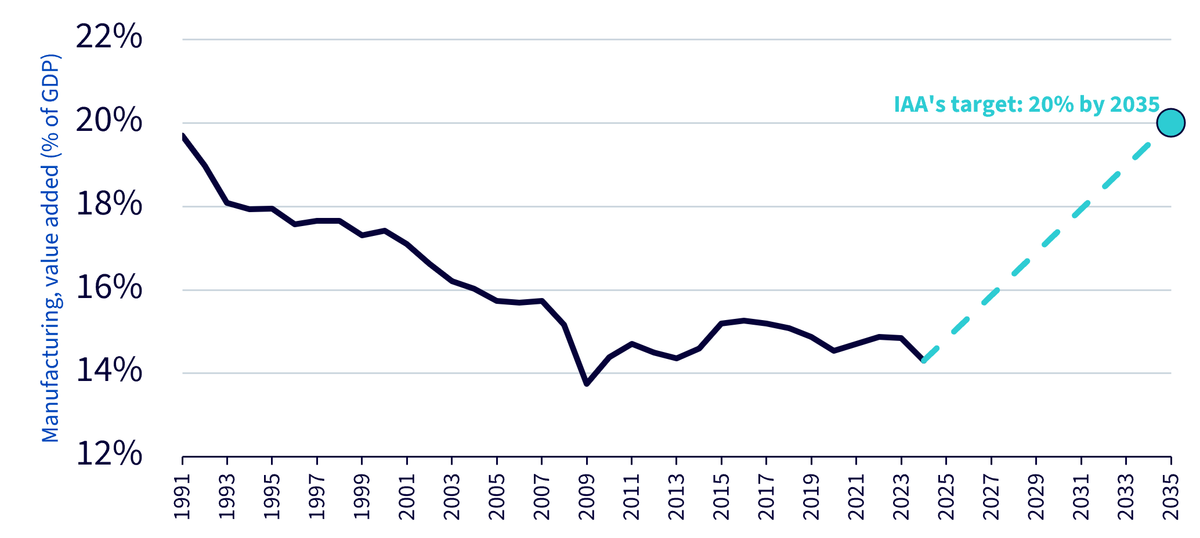

One challenge is the long-term decline of manufacturing. World Bank data shows that manufacturing value added accounted for around 19.7% of EU gross domestic product (GDP) in 1991, compared with 14.3% in 20241. While Europe remains home to many leading industrial companies, manufacturing has become a smaller part of the economy over time.

Source: World Bank. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

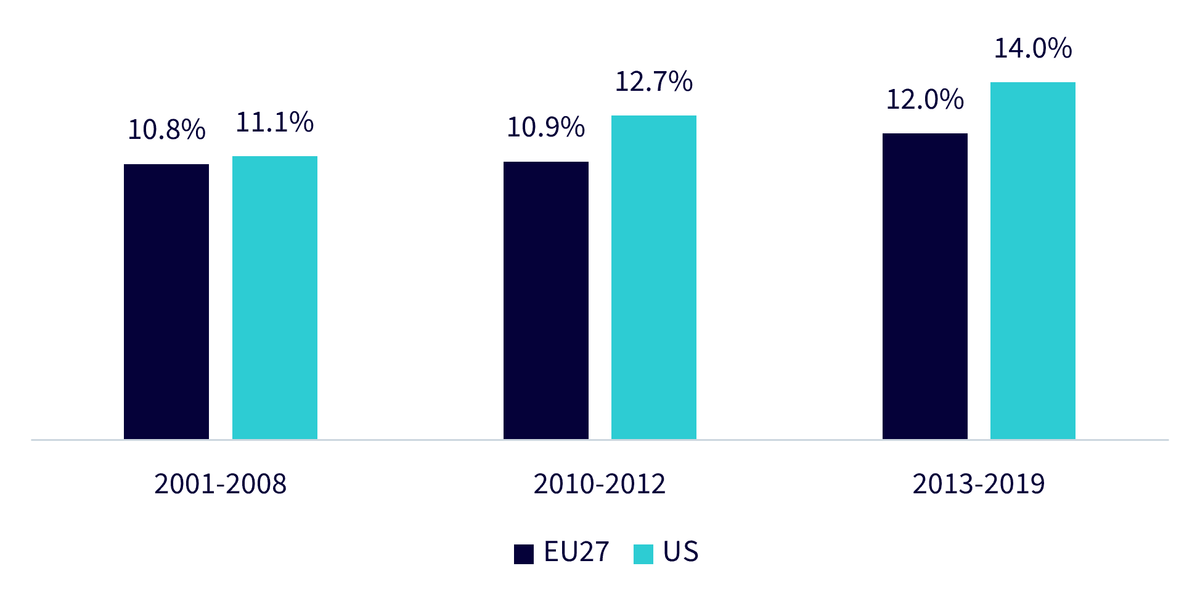

Investment is another pressure point. The Draghi report estimated that the EU may need an additional €750bn to €800bn of investment each year, equivalent to roughly 4.4% to 4.7% of GDP2, to support productivity, innovation and the green transition.

Source: EIB Working Paper 2024/01, ‘Dynamics of productive investment and gaps between the United States and EU countries’. Productive investment = total Gross fixed capital formation (GFCF) less construction. Rates are productive GFCF as % of gross value added, chain-linked volumes 2015, national deflators, annual averages.

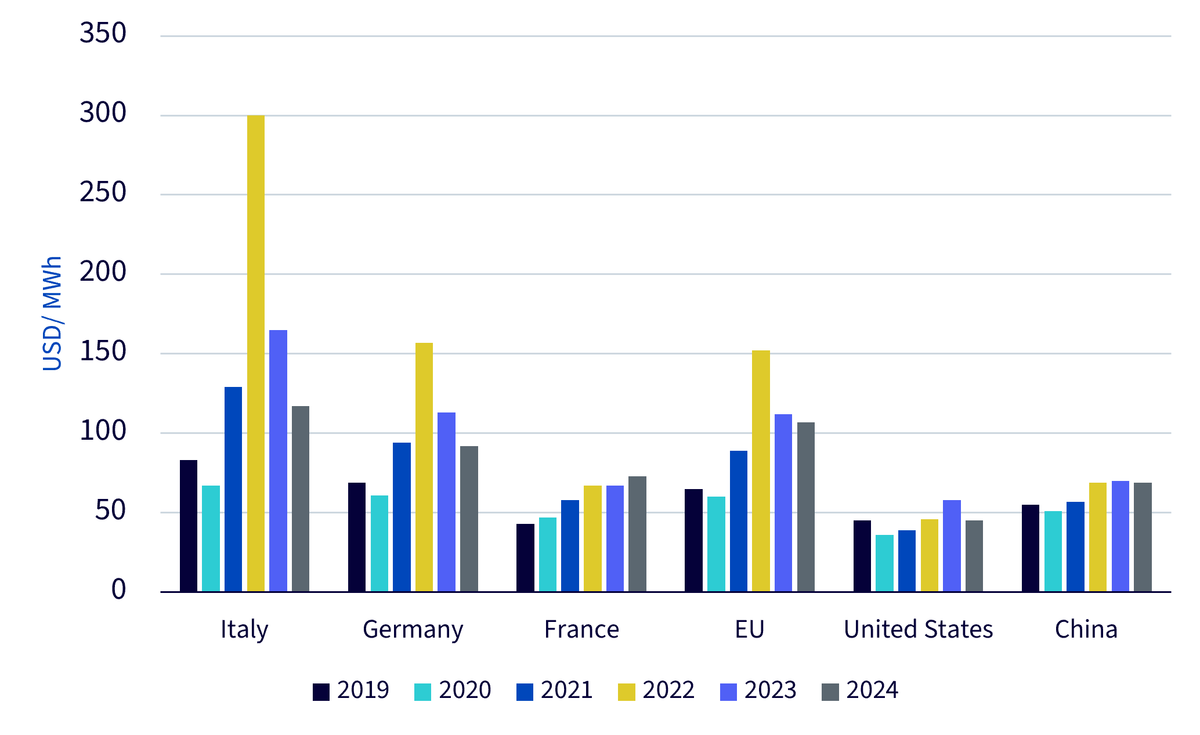

At the same time, the European industry faces structurally higher energy costs than some competing regions, particularly in energy-intensive sectors such as steel, cement and aluminium. The energy transition also raises new concerns about dependency risks linked to external supply chains, as technologies such as solar panels, batteries and power electronics remain heavily concentrated outside Europe.

Source: IEA. Historical data is provided for illustrative purposes only and is not indicative of future market conditions or investment outcomes.

Against this backdrop, policymakers are placing greater emphasis on industrial resilience and strategic autonomy. The Industrial Accelerator Act (IAA) is one of the latest initiatives aimed at strengthening domestic manufacturing, supporting low-carbon production and improving Europe’s industrial competitiveness.

The European Commission published the IAA proposal in March 2026. Although it is still a legislative proposal, it indicates a consensus is forming: Europe needs to strengthen its manufacturing base and reduce strategic dependencies.

The Commission’s proposal says the regulation would support the competitiveness and resilience of the EU manufacturing sector, with a focus on selected strategic sectors, while contributing to climate objectives, economic security and high-quality jobs. It also sets an ambition for manufacturing to account for 20% of EU GDP by 20353.

The Act focuses on three broad areas: energy-intensive industries, net-zero technologies and parts of the automotive supply chain. This makes it relevant not only to traditional materials such as steel and cement, but also to the manufacturing base underpinning Europe's energy transition, spanning renewable energy components, energy storage, grid electronics and electric mobility.

The Act has four main tools. First, it introduces public procurement reforms that give greater weight to low-carbon and resilience criteria, including ‘Made in EU’ and low-carbon requirements in public procurement and public support schemes. Second, it sets restrictions for certain large foreign direct investments in strategic sectors. Third, it seeks to simplify permitting for industrial manufacturing projects. Fourth, it requires member states to designate industrial manufacturing acceleration areas intended to cluster strategic industrial projects.

The sectors in scope are highly relevant to the physical economy. The European Commission believes that while these sectors may account for a limited share of total EU manufacturing output, they play a disproportionate role as upstream suppliers to construction, mobility, energy and defence.

Although the IAA is primarily an industrial policy initiative, it has several important implications for Europe’s infrastructure sector.

The direct infrastructure link is through public procurement and materials. From 2029, public procurement for buildings and civil infrastructure would need to include minimum shares of low-carbon steel, concrete or aluminium. Under the proposal, at least 25% of steel used in relevant buildings, infrastructure and vehicles would have to be low-carbon; concrete and mortar would need a 5% low-carbon and Union-origin share; and aluminium would need a 25% low-carbon and Union-origin share4.

Infrastructure projects are large consumers of steel, cement, concrete and aluminium. If implemented largely as proposed, it could create a more visible market for European low-carbon materials. This would be supportive for producers that can document carbon intensity and origin, and for contractors that can source compliant materials efficiently. European producers and construction firms may be better positioned in some areas, particularly where EU-origin requirements apply or where local production helps meet procurement and carbon emission standards.

A second area of relevance is manufacturing capacity for energy infrastructure components.

For Europe's energy infrastructure, supply-chain constraints have increasingly become a limiting factor in project delivery. Renewable energy components, energy storage systems and grid electronics all rely on manufacturing capacity. A stronger domestic manufacturing base could improve resilience and reduce some of the risks associated with concentrated global supply chains.

The IAA sits alongside broader European efforts to strengthen domestic production in these strategic sectors. Many renewable energy technology components remain more expensive to produce in Europe, while global supply chains are often concentrated outside the region. By creating clearer demand signals and improving development conditions, policymakers hope to encourage companies to invest in European capacity.

The Act may also influence infrastructure indirectly through industrial development.

New manufacturing facilities require supporting infrastructure, including electricity connections, transport links and utility networks. Industrial acceleration areas are intended to make it easier for strategic projects to move forward, potentially encouraging new industrial investment across Europe.

Value-chain area | Why IAA may matter | Representative companies |

|---|---|---|

Low-carbon construction materials | Public procurement would start to favour low-carbon and, in some cases, Union-origin cement, concrete and aluminium. | Heidelberg Materials, Holcim |

Low-carbon steel and metals | Public projects and support schemes could create clearer demand for lower-emission steel and aluminium inputs. | ArcelorMittal, SSAB |

Grid and electrification equipment | Net-zero technology manufacturing and acceleration areas may reinforce demand for grid equipment, power systems and charging infrastructure. | Prysmian, Nexans, Schneider Electric, Siemens Energy, ABB |

Clean-energy components and storage | “Made in EU” and resilience criteria may support European or Europe-based suppliers of wind, solar, battery and storage components. | Vestas, Nordex, SMA Solar |

Engineering and construction | Industrial acceleration areas, grid connections and decarbonisation projects may create work for civil engineering and EPC contractors. | Vinci, Eiffage, Acciona |

Source: WisdomTree. Companies shown are provided for illustrative purposes only. References to specific securities should not be construed as a recommendation to buy or sell any investment.

The Industrial Accelerator Act adds a new layer of policy support to the region’s infrastructure investment cycle. By linking public procurement with industrial resilience and domestic manufacturing capacity, the Act may strengthen demand for low-carbon construction materials, energy components and the infrastructure supply chains needed to deliver Europe’s long-term priorities. Its impact will depend on final implementation and potential trade frictions, but the direction is clear: Europe is increasingly treating infrastructure, the manufacturing industry and strategic autonomy as connected investment themes.

While the IAA could support parts of Europe’s industrial and infrastructure value chain, the ultimate impact remains uncertain. The proposal is still subject to the EU legislative process and implementation timelines may change. Demand for infrastructure-related products and services may also be affected by economic conditions, public spending priorities, interest rates, energy prices and broader geopolitical developments.

The WisdomTree Europe Infrastructure UCITS ETF (WBLD) seeks to provide exposure to companies involved in building and supplying Europe’s infrastructure value chain. Its value-chain approach targets exposure to construction firms and key component suppliers, avoids pure operators, and aligns the portfolio more closely with the areas where public funding, procurement rules and industrial policy may drive growth. The portfolio allocates meaningful exposure to construction materials, electrical equipment, and construction and engineering industries, which are directly relevant to the infrastructure and manufacturing channels highlighted by the IAA.

Source: WisdomTree.

1 Source: World Bank

2 European Commission, The Draghi report on EU competitiveness

3,4 European Commission, Industrial Accelerator Act

WisdomTree Europe Infrastructure UCITS ETF - EUR Acc

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).