WGLD LN

WisdomTree Core Physical Gold

Publié le 11 juillet 2025

Director, Research

The US Dollar experienced its sharpest first-half decline in over 50 years in 2025, undermined by erratic Trump’s Administration policy signals and clear signs of economic deceleration. The Dollar Index (DXY) fell 10.7%, while losses were even greater against key developed-market currencies: -12.6% versus the Swiss Franc, -12.2% against the Euro, and -8.7% versus the British Pound1. Meanwhile, several emerging market currencies saw some of their strongest performances in recent years.

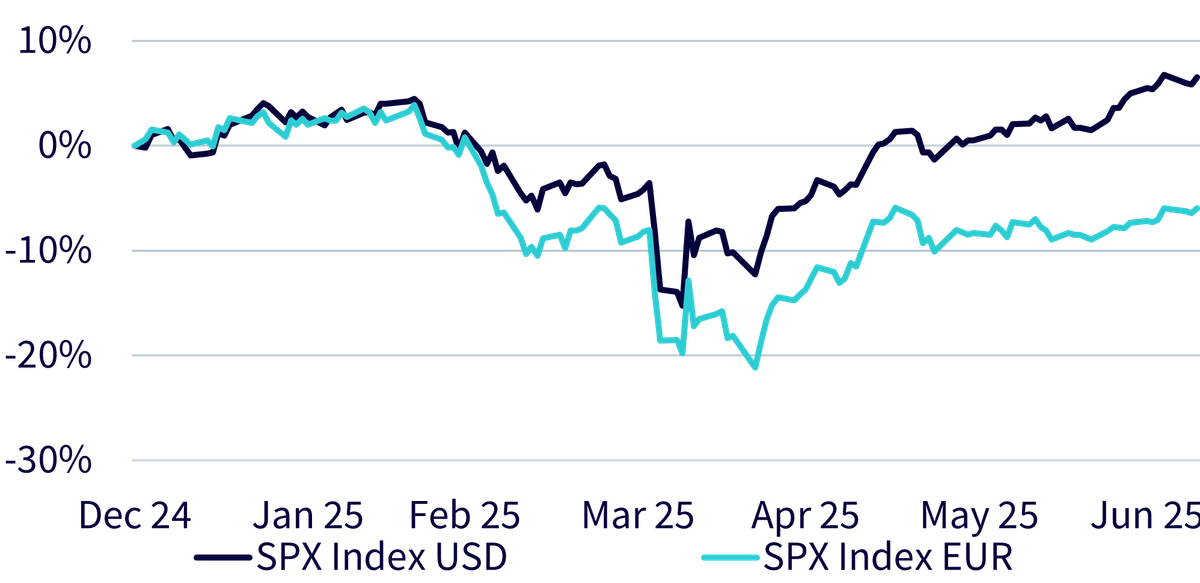

Currency fluctuations significantly affect total investment returns. For example, while the S&P 500 approaches new highs in USD terms, its value in euros is down 11% from the February peak2. A weaker Dollar, however, has also helped lower inflation in Europe, especially via cheaper energy-related commodities.

The Euro’s appreciation to its highest level since September 2021 has weighed on returns for Euro-based investors. In this environment, understanding the drivers of Dollar weakness and how to hedge currency exposure becomes essential. Additionally, and fortunately, there are solid tools to manage this risk.

Source: Bloomberg as of July 9, 2025.

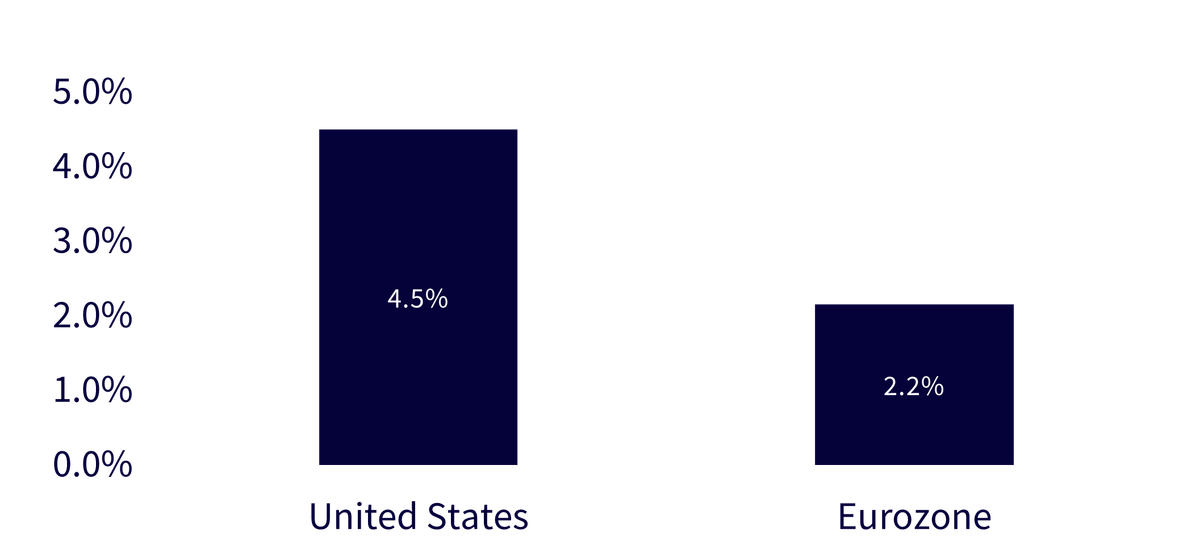

The primary reason for the Dollar’s weakness is political and economic unpredictability in the US. Investor confidence has been shaken by fears of aggressive economic and trade policies, including tariffs and tax cuts, alongside growing concern about debt ceiling negotiations and the independence of the Federal Reserve.

Macroeconomic data in the US points to slower growth, a mild uptick in unemployment, and falling consumption. As a result, investors have reduced their Dollar exposure in favor of other currencies and safe-haven assets.

In parallel, the Fed’s rate cuts have lagged those in Europe, as the Federal Reserve began easing only in September 2024. The very gradual pace of these cuts has reduced the relative attractiveness of USD-denominated assets for foreign investors.

Source: Bloomberg as of July 9, 2025.

These developments have a wide range of global implications, most of which are deflationary. Since many commodities (e.g., oil, industrial metals, and agricultural products) are priced in USD, a weaker Dollar makes them cheaper for countries with other base currencies. For commodity-importing regions like Europe and Asia, this reduces imported inflation.

Emerging market currencies have also benefited. A weaker Dollar reduces pressure on USD-denominated debt, a major burden for many EM (emerging market) economies. Currencies such as the Mexican Peso (MXN), Brazilian Real (BRL), Thai Baht (THB), and Indian Rupee (INR) have strengthened—especially where domestic growth remains solid. In such cases, currency gains can restore credibility and investor trust.

Further US dollar depreciation is possible, particularly if Trump’s second term brings renewed fiscal or protectionist measures. These could rapidly push the US closer to its debt ceiling (legal limit set by the US congress) or trigger political gridlock around public debt. Global trust in US financial governance could suffer, while the trend toward de-dollarization could accelerate, with countries like China and Russia expanding trade in currencies like the yuan or euro.

Although the Dollar still accounts for ~58% of global foreign reserves3, the process of de-dollarization is quietly advancing. For now, the Dollar’s dominance remains underpinned by strong US institutions and market liquidity. However, if erratic policies persist, the long-term risk of a diminished reserve role becomes more tangible.

Euro-based investors have felt the pain of Dollar weakness in the first half of 2025, particularly in USD-exposed parts of their portfolios. In retrospect, exposure to stronger currencies—like the Swiss Franc (CHF), Norwegian Krone (NOK), or resilient EM currencies—would have improved outcomes. Currency-hedged ETFs and active funds, though more expensive, could have helped mitigate forex losses.

Real assets are also useful hedges. Gold tends to move inversely to the Dollar, making it an effective store of value during USD downturns.

Selective exposure to emerging markets can be advantageous too—provided fundamentals justify it. This includes equity baskets or sovereign/corporate bonds denominated in local currencies, especially in well-managed economies. In such cases, EM currencies can both strengthen and support outperformance of the underlying assets.

Currency ETPs (Exchange-Traded Products) can serve as tactical tools. These instruments replicate the relative movement of currency pairs—such as EUR/USD—allowing investors to position for USD appreciation (long USD/short EUR) or depreciation (short USD/long EUR). They are widely used for hedging, speculation, or portfolio diversification.

ETPs typically track currency movements via derivatives (futures or swaps). A long USD/short EUR ETP gains when the Dollar rises against the Euro. Conversely, a short USD/long EUR ETP profits when the Dollar weakens. These instruments are not UCITS-compliant ETFs but structured ETNs, and should be usefully utilized tactically, more than as long-term core positions.

Could Trump’s “Big Beautiful Bill”—a proposed expansion of the 2017 tax cuts—further weaken the Dollar? It is a possibility. It includes:

Such measures could temporarily stimulate demand, boost disposable income, and support investment. They may also encourage reindustrialization and improve the US business climate. In the short term, this could attract foreign capital and strengthen the Dollar.

Source: Congressional Budget Office (CBO). The Long-Term Budget Outlook: 2025 to 2055, from March 27, 2025 Report.

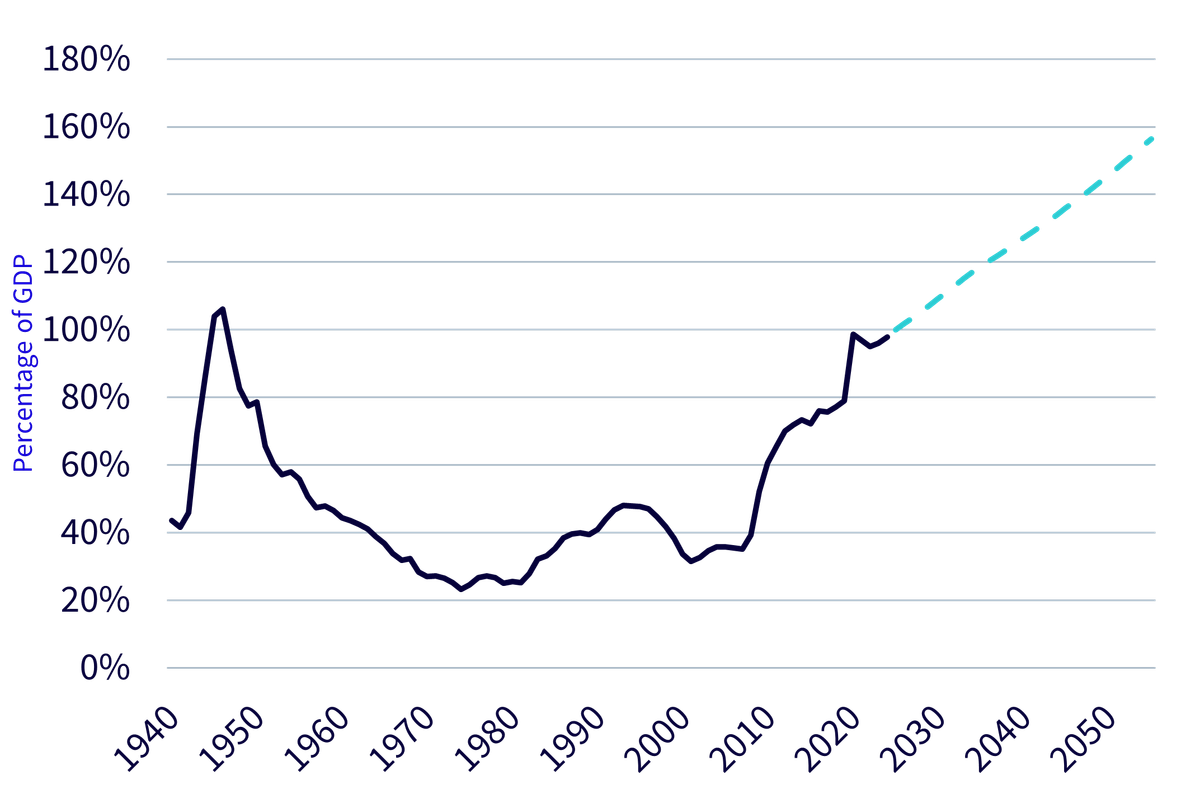

But the long-term risks are considerable. The US budget deficit already nears 6–7% of GDP, and public debt exceeds $34 trillion. Further fiscal expansion could increase sovereign risk and raise long-term interest rates as the Debt to GDP ratio (Figure 3) continues to climb. Moreover, the proposed tax cuts are criticized for favouring high-income earners, worsening inequality4.

From a currency standpoint, the effects may be twofold:

This dynamic played out after the 2017 Tax Cuts and Jobs Act. The Dollar weakened in 2018 despite strong economic growth and rising Fed rates—mainly due to fiscal concerns.

In essence, markets don’t respond to growth alone—they care about the sustainability and quality of that growth.

The Dollar’s weakness in 2025 stems from a mix of domestic political uncertainty, macroeconomic slowdown, and global financial realignment. For Euro-based investors, navigating this environment requires an active, diversified approach. Hedging tools, such as currency pair ETPs, exposure to uncorrelated assets, and careful currency positioning are key to weathering further volatility.

1 Bloomberg, period December 31, 2024 to June 30, 2025

2 Bloomberg, period February 20, 2025 to June 30, 2025

3 Council on Foreign Relations, June 8, 2025

4 One Big Beautiful Bill Gives Richest 20% an Average $6,055 Tax Break - Bloomberg, June 30, 2025

Director, Research

Piergiacomo is Director of Research at Wisdomtree. He has over 20 years of experience within the financial services industry, having served as the Head of Discretionary Portfolio Management at Banca Albertini Spa in Milan before joining WisdomTree. Prior to this, he held roles at Rasbank Spa (currently AllianzBank Financial Advisors) as Head of Equity Research and Head of Equity Desk. Piergiacomo has an M.Sc. in Financial Markets Economics from Bocconi University in Milan. He is also a chartered member of the Aiaf (Italian Association of Financial Analysts).