WENU LN

WisdomTree Strategic Metals UCITS ETF - USD Acc

Publié le 16 janvier 2026

After several years of oversupply and weak sentiment, strategic metals staged a powerful comeback in 2025. What began as tentative price stabilisation turned into a broad-based rebound, driven not by exuberant demand alone, but by deliberate supply restraint, policy intervention and structural shifts in energy demand.

From lithium to cobalt, copper and nickel, 2025 marked a turning point — one that may define the next phase of the energy transition.

Years of oversupply and scepticism around energy transition materials weighed heavily on strategic metals between 2022 and 2024. That narrative flipped in 2025.

The WisdomTree Energy Transition Metals Commodity UCITS Index TR delivered its strongest performance since 20091, rising 38% and outperforming the Bloomberg Commodity Industrial Metals Index by 17 percentage points. WisdomTree Energy Transition Metals Commodity UCITS Index TR provides exposure to the following 10 metals: Aluminium, Zinc, Nickel, Lead, Copper, Silver, Platinum, Tin, Cobalt, Lithium Hydroxide. Investor interest in WisdomTree Strategic Metals UCITS ETF which tracks this index surged, reflecting renewed conviction in the role of critical materials. WisdomTree Strategic Metals UCITS ETF is the only UCITS ETF that gives investors exposure to lithium and cobalt.

WisdomTree Energy Transition Metals Commodity Index TR | Bloomberg Commodity Industrial Metals TR | |

|---|---|---|

2003 | 53% | 44% |

2004 | 17% | 25% |

2005 | 27% | 33% |

2006 | 79% | 72% |

2007 | 2% | -10% |

2008 | -43% | -48% |

2009 | 70% | 80% |

2010 | 30% | 16% |

2011 | -22% | -24% |

2012 | 3% | 1% |

2013 | -17% | -14% |

2014 | -7% | -7% |

2015 | -27% | -27% |

2016 | 20% | 20% |

2017 | 21% | 29% |

2018 | -16% | -19% |

2019 | 10% | 7% |

2020 | 20% | 16% |

2021 | 28% | 30% |

2022 | 1% | -2% |

2023 | -14% | -9% |

2024 | 4% | 4% |

2025 | 38% | 21% |

Source: WisdomTree, Bloomberg. Data as of 31/12/2025. WisdomTree Energy Transition Metals Commodity Index TR and WisdomTree Battery Metals Commodity Index TR went live on 3rd February 2022. Backtested indices apply February 2022 weights historically. Historical performance is not an indication of future performance and any investments may go down in value.

This re-rating coincided with the year artificial intelligence entered the mainstream, driving a step-change in power demand. The energy transition has increasingly become an “energy addition” story — the world needs more of every energy source, not fewer. That is particularly true for power (electricity) and the metals that enable electrification are seeing a boost in demand. The metals in the index reflect this reality, with weightings influenced by both transition/addition relevance and market balance. Oversupplied metals are penalised; tightening markets are rewarded.

Crucially, 2025 was also the year supply discipline returned.

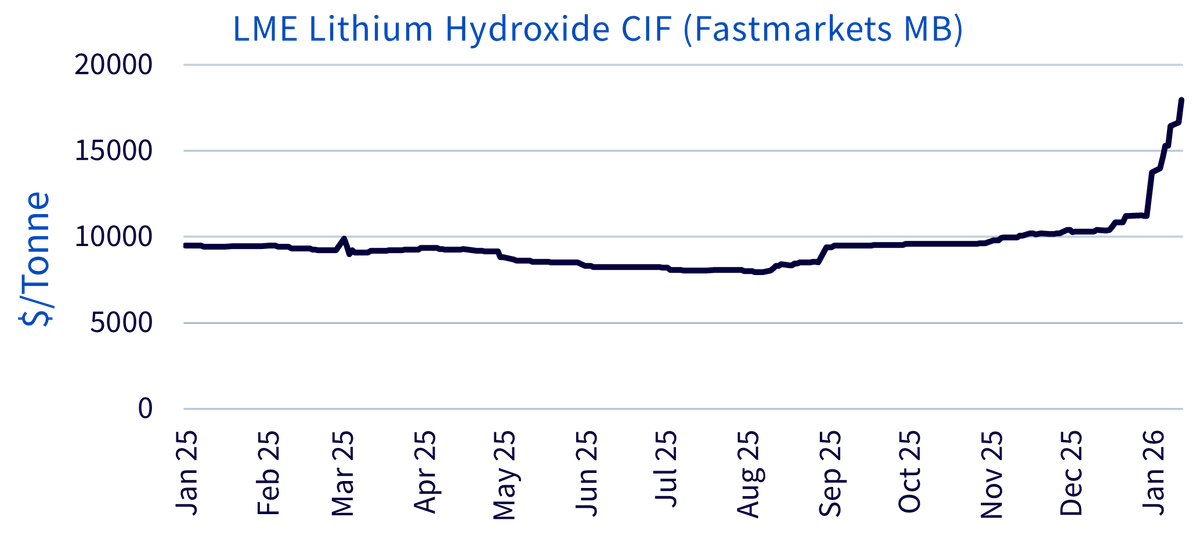

Lithium has been the standout performer. Prices have rallied more than 120% since July 2025, including a 60% surge in just the first two weeks of 2026. After falling almost continuously from the 2022 peak, lithium finally found its floor in mid-2025 and the recovery since then has been swift.

Source: WisdomTree, Bloomberg, LME Lithium Hydroxide CIF (Fastmarkets MB). Janaury 2025 to January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

The second-half 2025 rebound was fundamentally driven, rather than speculative. By mid-year, prices had fallen deep into the global cost curve, forcing producers to react. Several Australian miners downgraded production guidance or placed assets into care and maintenance as spot prices slipped below sustainable levels. Refining ramp-ups slowed, new project investment was delayed, and the market began to rebalance.

A key catalyst arrived when Contemporary Amperex Technology Co, CATL suspended mining operations in Jiangxi province, raising concerns over regional supply availability. That shock helped restore confidence in the underlying market balance and became a critical driver of the late-2025 price recovery.

On the demand side, while electric vehicle (EV) sales attracted most of the headlines, energy storage system (ESS) demand surged faster than expected. By late 2025, inventories had tightened materially. A sharp futures rally followed, prompting exchanges to impose position limits, higher margins and increased transaction fees to prevent a disorderly short squeeze.

More recently, China introduced a major policy shift. The Ministry of Finance and State Taxation Administration announced that VAT export rebates for battery products — including lithium batteries — will be:

This follows earlier cuts from 13% to 9% in late 2024 and forms part of broader “anti-involution” policies aimed at curbing destructive price competition.

The impact has been immediate. Exporters are front-loading shipments ahead of rebate reductions, lifting near-term battery output and boosting demand for upstream materials such as lithium carbonate. Chinese lithium carbonate futures jumped sharply in early January 2026 as well.

Importantly, the spodumene market now looks tighter than lithium carbonate, with deficits expected in 2026. This increases volatility risks for lithium hydroxide, which relies heavily on spodumene feedstock and underpins the futures contract tracked by our index (see below).

Cobalt exemplifies this shift. The Democratic Republic of Congo (DRC) supplies more than 70% of global cobalt production, giving it unparalleled influence over the market.

By early 2025, cobalt prices had fallen to a nine-year low of around $10 per pound, as supply growth far outpaced demand. Inventories ballooned, eroding producer revenues.

The DRC responded decisively:

These measures helped lift prices, draw down inventories and bring supply closer in line with demand. Strategically, the DRC also aims to encourage domestic processing and improve its pricing power in global supply chains.

That said, tensions remain. While Glencore supports quota-based management, CMOC has pushed for looser restrictions. There are also concerns that prolonged controls could increase smuggling or supply chain distortions.

Copper markets tightened sharply in 2025 as production setbacks accumulated across multiple regions. Global concentrate supply undershot expectations, pushing the market into a material deficit.

The most consequential event occurred at Grasberg, one of the world’s largest copper mines. In September 2025, a severe mudslide struck the underground Block Cave operation, killing workers and forcing Freeport-McMoRan to declare force majeure. The mine is not expected to come back online fully until 2027.

Analysts estimate the disruption could remove 250,000–260,000 tonnes of copper output in both 2025 and 2026, with total lost supply potentially exceeding 500,000 tonnes. The incident triggered immediate price pressure and underscored the vulnerability of copper supply to single-asset risks.

Grasberg was not alone. Chile suffered power outages and a fatal tunnel collapse at El Teniente. Peru faced temporary closures due to social unrest. Accidents in Kazakhstan, China and Canada, alongside wildfire disruptions in North America, compounded the tightness.

Nickel may be next. Indonesia accounts for around 65% of global nickel production, but officials have confirmed plans to slow output growth in 2026 as a deliberate intervention.

Energy and Mineral Resources Minister Bahlil Lahadalia has framed the move as a way to support prices, curb oversupply and manage resource depletion amid rising inventories and weak pricing.

At the centre of the strategy is Indonesia’s RKAB system, which caps mining output. Reports suggest the 2026 nickel ore quota could be cut to around 250 million tonnes, roughly 30–35% below 2025 target levels. If implemented, this would mark a significant break from decades of aggressive expansion.

What unites lithium, cobalt, copper and nickel is not just stronger demand — it is the return of supply discipline. Governments and producers alike are showing a growing willingness to intervene, constrain output and protect long-term value.

For strategic metals, 2025 may be remembered as the year the cycle turned — from abundance at any cost to balance by design. 2026 is when we expect these trends to be amplified.

1 While the index technically only started in January 2024, its sister index, WisdomTree Energy Transition Metals Commodity Index TR, has live history since February 2022 and backtested performance prior to that using February 2022 weights.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.