WCLD LN

WisdomTree Cloud Computing UCITS ETF - USD Acc

Publié le 8 novembre 2024

Senior Associate, Quantitative Research and Multi Asset Solutions

Following the conclusion of the US presidential election, the Nasdaq-100 index rallied to reach an all-time high. This was driven by the prospect of a potentially favourable regulatory environment under the new president, along with strong Q3 earnings from major tech companies. Software companies within the index also showed signs of recovery in their recent earnings reports. However, from a macroeconomic perspective, the outlook remains mixed, and the Fed’s guidance will be closely monitored for signals on the future direction of monetary policy.

Is "Higher for Longer" still in play?1

Although the Fed implemented a 50 bps rate cut in September, rising concerns over fiscal deficits and resilient nonfarm payroll figures (with 254,000 jobs added in September). Entering November, the nonfarm payroll figure for October showed an increase of only 12,000 jobs. However, this figure was impacted by hurricane disruptions, making it less indicative of underlying trends. Further employment data in the coming months will be necessary to get a clearer view of labour market conditions.

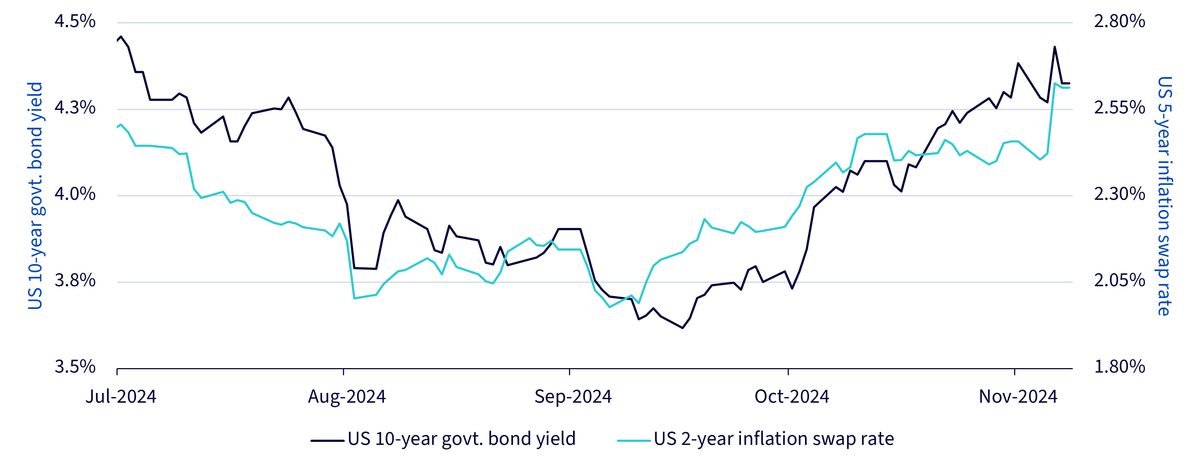

On the inflation front, September's inflation rate, although lower than the previous month, remained steady at 2.4%—slightly above the consensus estimate of 2.3%. Following the presidential election, potential high tariffs could add upward pressure on CPI. Notably, the US 2-year inflation swap rate recently approached highest level since April, suggesting that the market is anticipating more resilient inflation ahead (Figure 1).

These pushed the US 10-year government bond yield up by over 70 bps since its mid-September low as of 07 November 2024.

While the Fed implemented a 25 bps rate cut following the election, as widely expected, the timing of further rate cuts may now need to be reassessed and could be delayed in light of these new macroeconomic dynamics.

Source: WisdomTree, Bloomberg, from 01 July 2024 to 07 November 2024. Historical performance is not an indication of future results and any investments may go down in value.

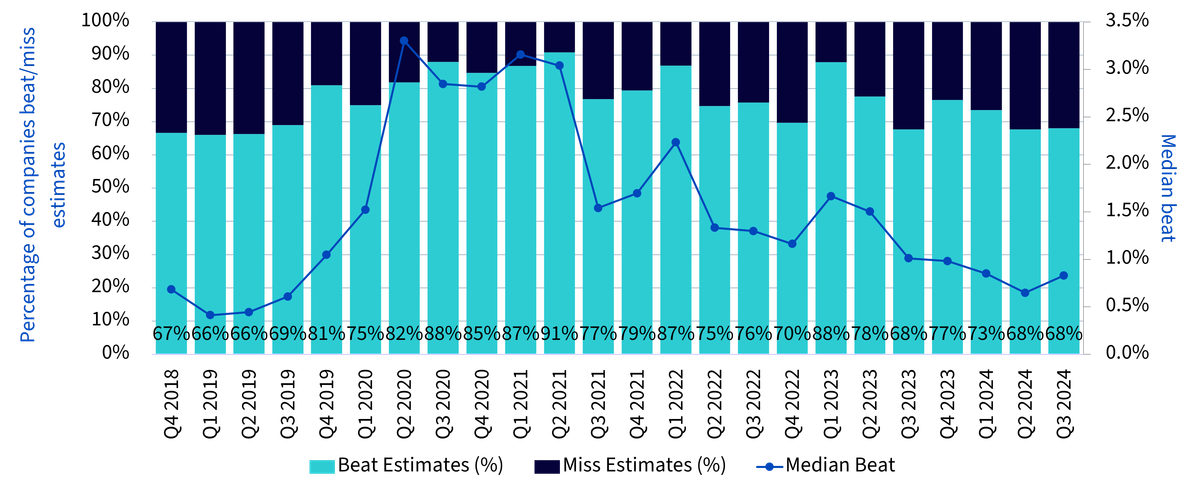

As of 7 November, 75 constituents of the Nasdaq-100 index had reported their Q3 earnings, with 68% of them delivering a positive revenue surprise against consensus estimates. The median positive surprise was 0.8%, slightly higher than Q2's level of 0.6%, although still below the levels seen in 2022 and 2023. Among all sectors, information technology was the one with the highest percentage of companies reporting earnings above estimates in Q3 2024. Additionally, of these 75 companies, 27 provided sales guidance, and 25 reported revenue figures above their own guidance. (Figure 2a)

GICS sector | Total companies | Companies reporting Q3 earnings | Companies with positive Q3 revenue surprise | % of companies with positive Q3 revenue surprise |

|---|---|---|---|---|

Information Technology | 39 | 22 | 20 | 90.9% |

Communication Services | 10 | 10 | 9 | 90.0% |

Health Care | 12 | 11 | 8 | 72.7% |

Industrials | 10 | 7 | 4 | 57.1% |

Consumer Discretionary | 12 | 9 | 5 | 55.6% |

Utilities | 4 | 4 | 2 | 50.0% |

Energy | 2 | 2 | 1 | 50.0% |

Consumer Staples | 8 | 7 | 2 | 28.6% |

Materials | 1 | 1 | 0 | 0.0% |

Financials | 1 | 1 | 0 | 0.0% |

Real Estate | 1 | 1 | 0 | 0.0% |

Total | 100 | 75 | 51 |

Source: WisdomTree, Bloomberg, as of 07 November 2024. The median beat denotes the median of volume by which reported sales exceed consensus estimates. Consensus estimates are the means of analysts’ estimated sales available on Bloomberg. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. Some earnings have not yet become public and typically begins to become public about one month into the future as companies report their results for the period ended 30 September or 31 October 2024. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

Source: WisdomTree, Bloomberg, as of 07 November 2024. GICS is the Global Industry Classification Standard. Consensus estimates are the means of analysts’ estimated sales available on Bloomberg. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. GICS Sectors represent first level classification in the Global Industry Classification Standard (GICS) hierarchy. You cannot invest directly in an index. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

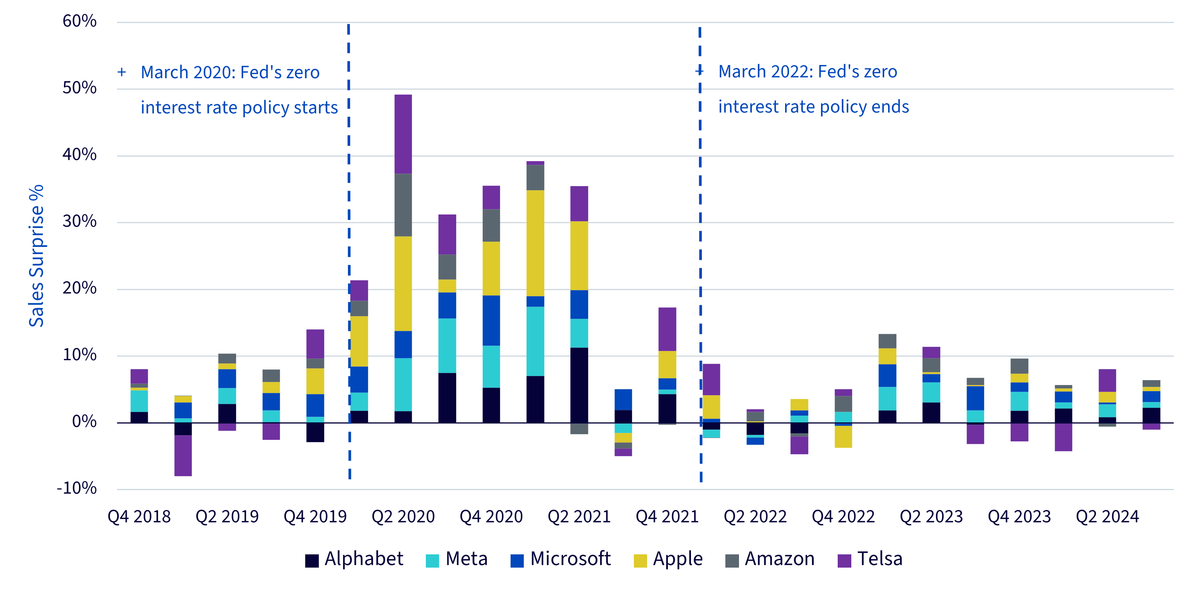

The Nasdaq-100’s performance has largely been driven by the tech giants known as the “Magnificent 72.” As of 7 November 2024, six of these companies had reported their Q3 earnings, with five exceeding consensus revenue estimates. Only Tesla’s Q3 revenue fell short of expectations. Looking back, these six companies significantly beat estimates in 2020 and 2021, when interest rates were near zero. However, as the Fed began raising rates, their revenue surprises narrowed, hovering close to zero. After Q4 2022 earnings, revenue surprises began to rebound (Figure 3a).

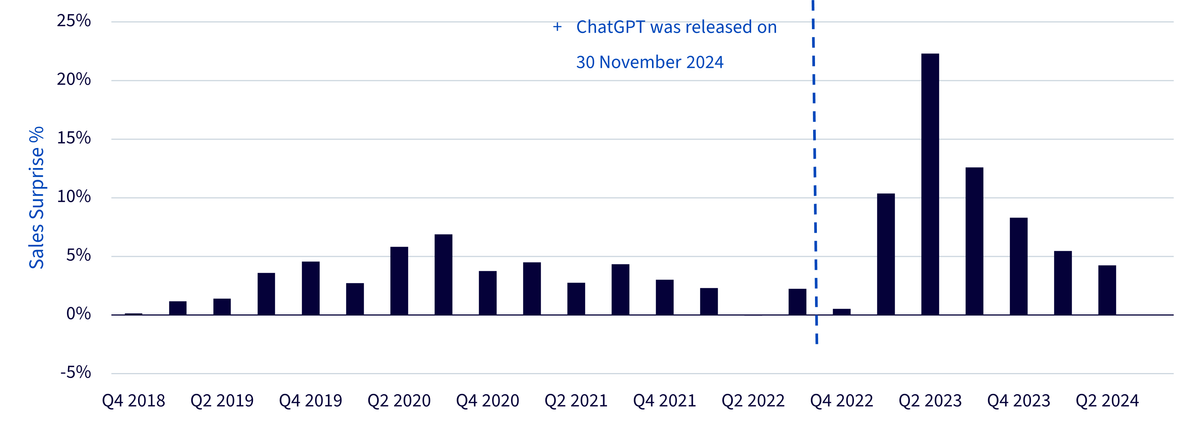

Nvidia’s revenue surprise tells a somewhat different story (Figure 3b). After the release of ChatGPT in November 2022, Nvidia’s revenue surprises surged, peaking with its Q2 2023 earnings before gradually decreasing to 4.2% in Q2 2024. This trend suggests that Nvidia's sales growth is gradually aligning with market expectations, although a gap still remains. Its Q3 earnings, due to be released in November, will provide further insight into the trajectory of its revenue surprises.

Source: WisdomTree, Bloomberg, as of 07 November 2024. Consensus estimates are the means of analysts’ estimated sales available on Bloomberg. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. Historical performance is not an indication of future results and any investments may go down in value.

Source: WisdomTree, Bloomberg, as of 07 November 2024. Consensus estimates are the means of analysts’ estimated sales available on Bloomberg. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. Historical performance is not an indication of future results and any investments may go down in value.

Software companies enjoyed substantial sales growth during the pandemic, benefiting from low interest rates and the shift to remote work. However, they have faced challenges this year. On one hand, high interest rates have impacted their performance by increasing funding costs and compressing valuations; on the other hand, slower sales growth has weighed on the valuation of these growth-driven stocks. Additionally, concerns that AI could replace some software services have shaken investor sentiment.

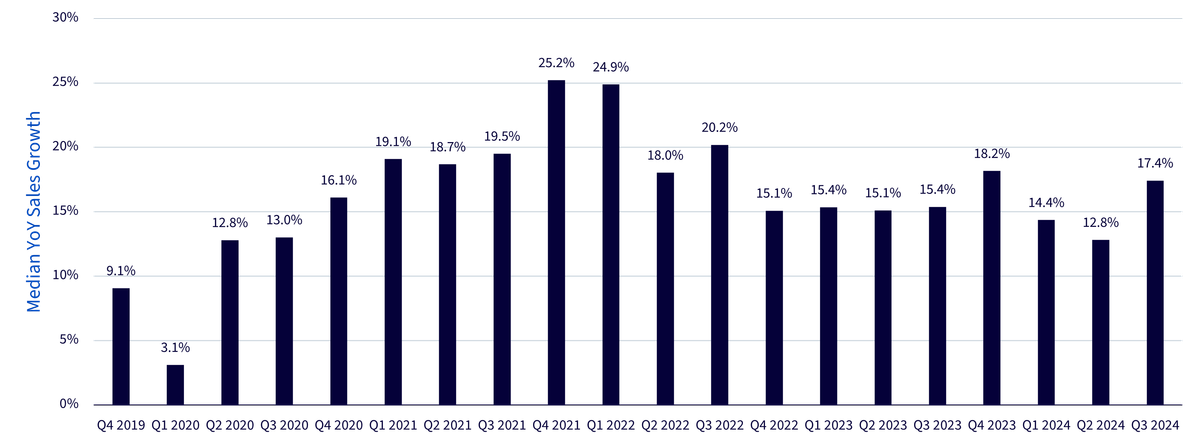

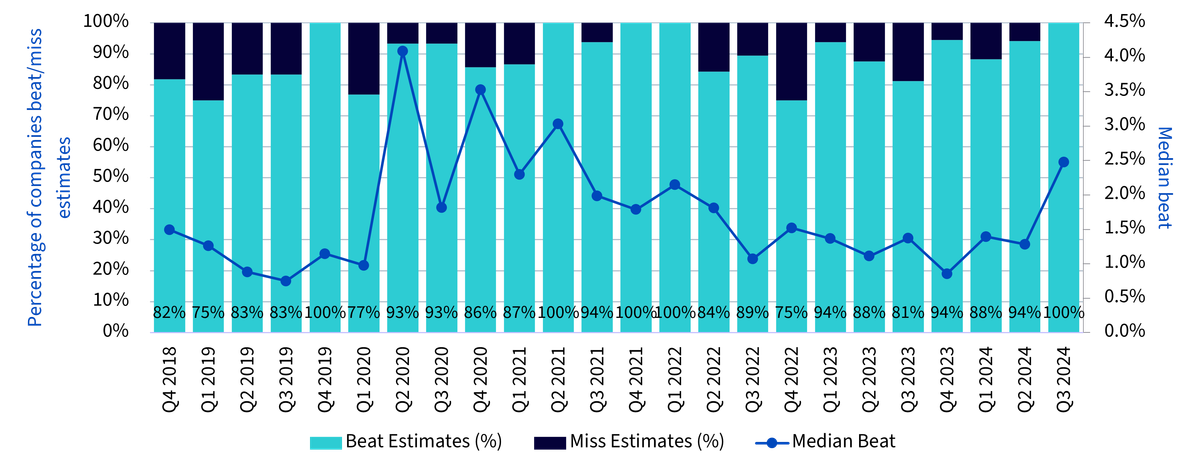

Recent earnings reports, however, have provided some positive signals for software companies in the Nasdaq-100 index. Firstly, the median year-over-year sales growth has rebounded from the weak levels of the first two quarters of this year (Figure 4a), which is likely to support these growth-oriented stocks. Secondly, all software companies that have reported Q3 earnings so far have delivered a revenue surprise relative to consensus estimates, with the median revenue surprise reaching 2.1% (Figure 4b)—the highest level since Q2 2021. If this figure holds once all companies have reported, it could be a strong indicator that Q3 may represent a turning point for the software sector.

Source: WisdomTree, Bloomberg, as of 07 November 2024. Sales growth rates are based on year-over-year changes in quarterly revenue. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. Some earnings have not yet become public and typically begins to become public about one month into the future as companies report their results for the period ended 30 September or 31 October 2024. Software companies are classified based on GICS. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

Source: WisdomTree, Bloomberg, as of 07 November 2024. The median beat denotes the median of volume by which reported sales exceed consensus estimates. Consensus estimates are the means of analysts’ estimated sales available on Bloomberg. The Q3 2024 data is based on the fiscal period of time that ended 30 September or 31 October 2024. Some earnings have not yet become public and typically begins to become public about one month into the future as companies report their results for the period ended 30 September or 31 October 2024. Software companies are classified based on GICS. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

The Nasdaq-100’s rise to an all-time high highlights the strong earnings performance of tech giants, with potential signals of recovery emerging in the software sector. While macroeconomic uncertainties, including inflation pressures and the Fed’s future rate path, remain areas of caution, the resilience in corporate earnings provides a supportive foundation. Balancing these positive corporate signals with broader economic risks will be key to determining whether the Nasdaq-100 can build on its recent momentum in the coming quarters.

1 Returns and macro data were sourced from Bloomberg, as of 07 November 2024.

2 Magnificent 7 stocks: Apple, Alphabet, Amazon, Microsoft, Meta, Telsa, Nvidia.

WisdomTree Cloud Computing UCITS ETF - USD Acc

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).