DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Publié le 16 février 2026

Senior Associate, Quantitative Research and Multi Asset Solutions

Japan’s February snap election delivered something markets rarely get in Tokyo - a decisive political authority and a clearer line of accountability. Prime Minister Sanae Takaichi dissolved parliament with little warning and voters responded by handing the Liberal Democratic Party a commanding result, clearing both an absolute stable majority threshold and a two thirds majority in the Lower House. That shift matters because it reduces legislative friction and speeds up policymaking, but it also concentrates market focus on one question – how ambitious fiscal policy becomes.

The election was preceded by a policy proposal that caught investors off guard. A pledge to suspend the consumption tax on food for two years. Even if the final design ends up more limited, the signal was enough to refocus attention on issuance, term premia and the yen. That explains why the post-election move was a familiar trio. Equities rallied on expectations of stronger nominal growth. Bond yields rose as investors priced the possibility of higher net supply and a higher fiscal premium.

For investors seeking to capitalise on Sanae Takaichi’s victory and sector specific opportunities, the WisdomTree Japan Equity UCITS ETF (Ticker: DXJ) offers a valuable solution. DXJ tracks the WisdomTree Japan Hedged Equity UCITS Index (Ticker: WTIDJHUT)—a fundamentally weighted index that selects Japanese companies deriving at least 20% of revenue from overseas markets, with a strong emphasis on dividend paying exporters and industrial cyclicals.

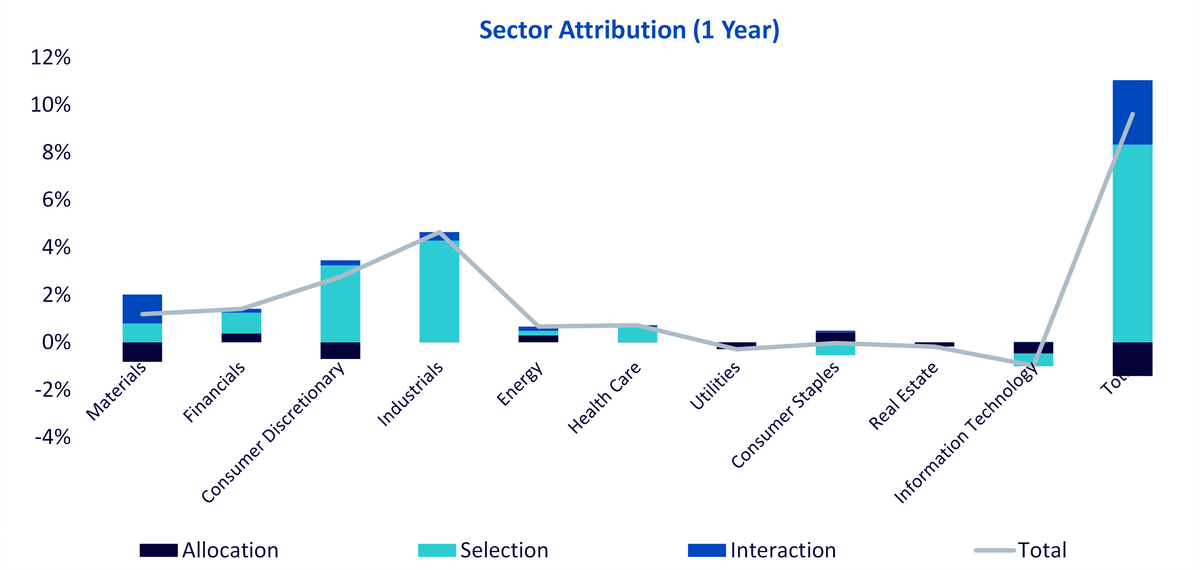

This aligns well with the expected beneficiaries of Sanae Takaichi’s victory and sector specific mix. In addition, DXJ has meaningful allocations to materials, financials and industrials, sectors that are expected to benefit from increased fiscal stimulus and a steeper Japanese yield curve. Over the past year, the WisdomTree Japan Hedged Equity UCITS Index outperformed the MSCI Japan Index by 9.62% benefitting from its selection of stocks within industrials, consumer discretionary and financials.

Source: FactSet, WisdomTree from 31 January 2025 to 30 January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

The more constructive interpretation of the election is that it increases the odds Japan can execute a coherent growth regime. Takaichi’s policy platform is framed around responsible and proactive fiscal measures aimed at lifting nominal growth. The government has highlighted a set of strategic investment fields that include semiconductors, energy security, defence and digital infrastructure, which are designed to raise supply capacity over time rather than simply boost near term demand.

This interacts with a structural force already in motion: corporate governance reform. The Tokyo Stock Exchange’s push for management that is conscious of cost of capital and valuation has accelerated corporate actions. Disclosure compliance is high, the share of stocks trading below book has fallen meaningfully, and buybacks have been trending higher over recent years. The market implication is straightforward. Better capital discipline can lift return on equity and improve the quality and durability of earnings, even when top line growth is not spectacular.

DXJ incorporates a dividend weighting methodology that tilts toward higher-quality companies with stable cash flows and strong shareholder return profiles. As investor preference rotates toward income-generating, capital-efficient businesses, DXJ is well placed to capture this shift. This dividend orientation also aligns with the ongoing transformation in Japanese corporate behaviour, where firms are increasingly deploying capital via share buybacks and higher dividends—trends that have accelerated since the implementation of governance reforms and Tokyo Stock Exchange (TSE) pressure for improved Return on Equity (ROE).

The recent election result strengthens the domestic political base for the defence shift signalled in the 2022 National Security Strategy. Prime Minister Sanae Takaichi’s decisive win has reduced resistance to her hawkish agenda and gives the LDP more room to press ahead with defence expansion. The main impact is less about direction, and more about pace and ambition. After decades of spending around 1% of GDP, Japan is targeting 2% by FY2027, and the stronger mandate raises the likelihood of faster execution and renewed debate about a higher ceiling over time, alongside constitutional revision discussions. This improves visibility for the Asia defence investment theme.

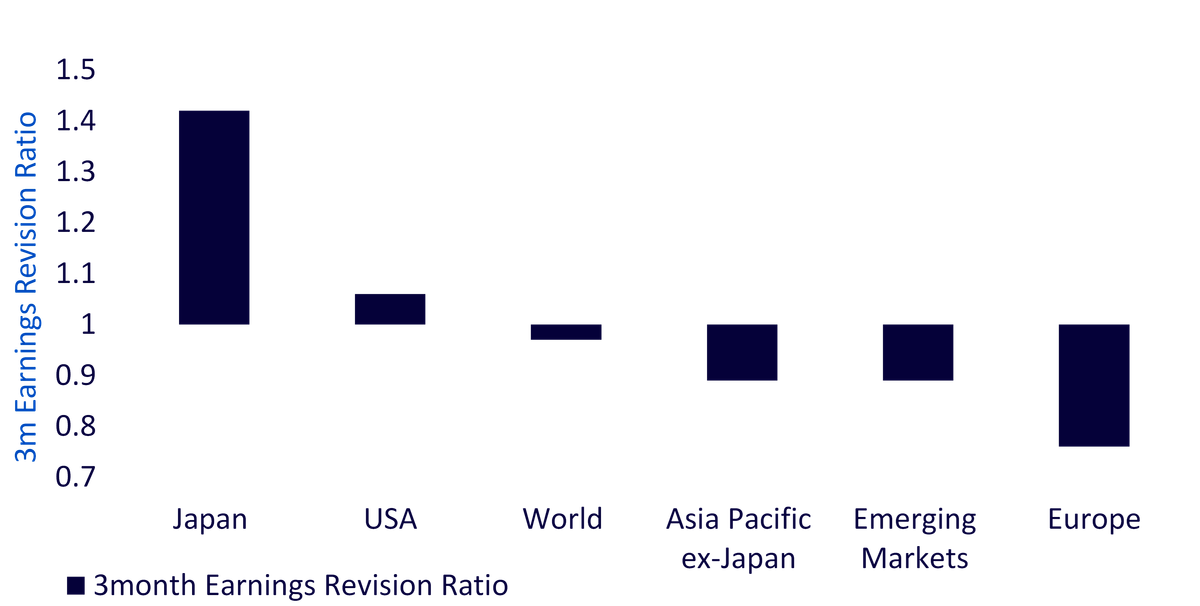

A second pillar of the equity case is earnings breadth. The US has been strong, but much of its earnings narrative has been concentrated in a narrow set of mega cap technology and AI linked firms. Japan’s earnings momentum, by contrast, has been broader across sectors, spanning traditional value areas and growth-oriented segments. That breadth helps explain why Japanese equity performance has remained resilient even as rates have normalised.

Source: MSCI, IBES, WisdomTree as of 31 January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

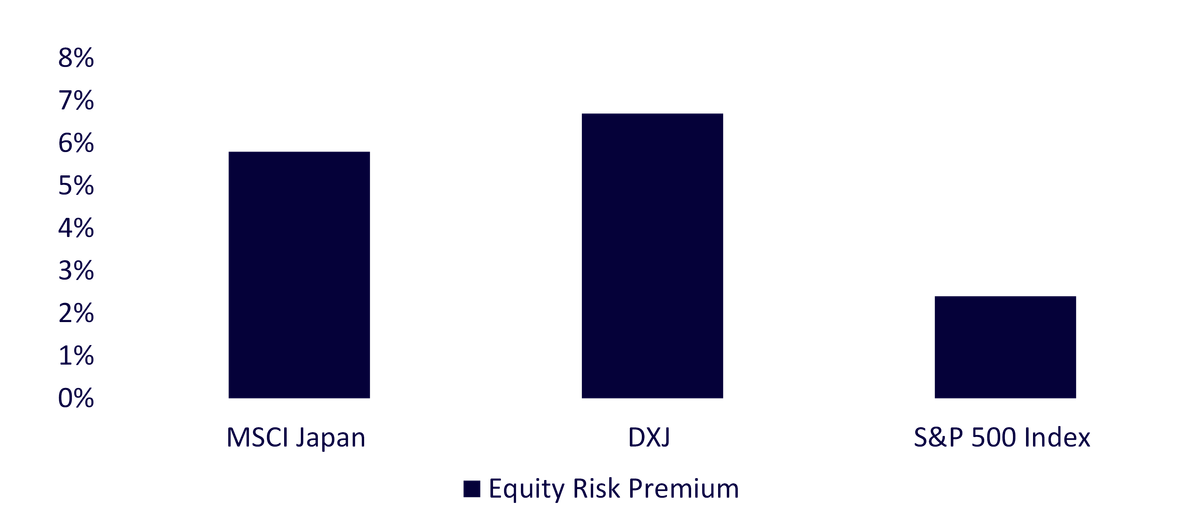

The key valuation bridge between rising yields and equities is the equity risk premium, which compares earnings yields to inflation adjusted bond yields. Even with higher JGB yields, Japan can still screen as offering a healthier buffer than the United States when you make that comparison. The reason is simple: Japanese equity valuations remain lower, and the earnings yield is higher, so the market can absorb some rate pressure without immediately losing its relative appeal, especially if nominal growth stays firm.

Source: FactSet, WisdomTree as of 31 January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

One nuance is important. The rise in yields has been large enough that the Bank of Japan (BOJ) has commented on the pace of the sell off and signalled it can step in if trading becomes disorderly, even as it continues to move away from ultra easy settings. That combination is consistent with a central bank that wants normalisation but aims to avoid an abrupt tightening of financial conditions.

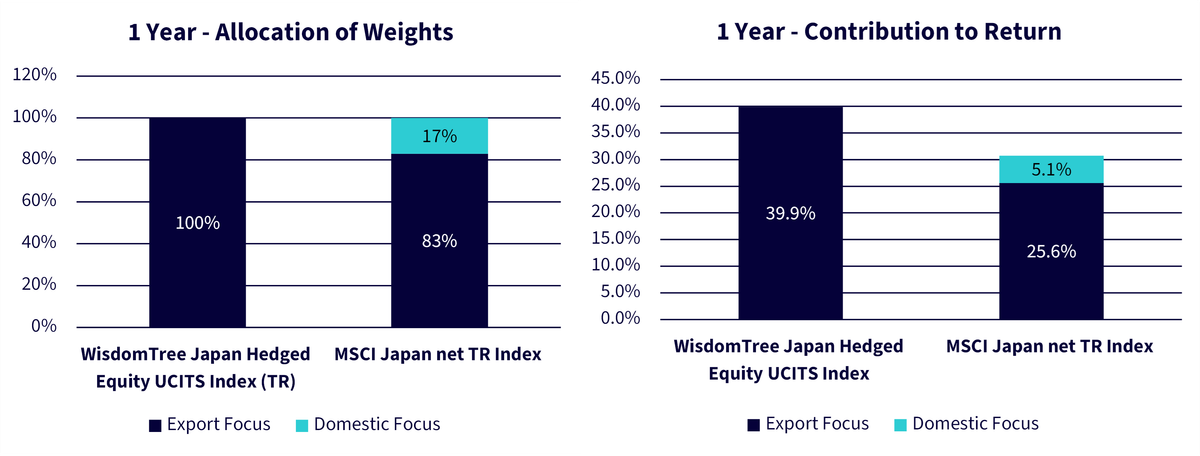

A core feature of DXJ is its built-in USD hedging, which significantly reduces the impact of yen depreciation on total returns. DXJ helps isolate equity alpha from FX noise, providing a cleaner and more stable source of return.

This is especially important at a time when global macro conditions, particularly diverging central bank policies are driving substantial currency volatility. Over the past year, the WisdomTree Japan Hedged Equity UCITS Index outperformed the MSCI Japan Index by 9.62% supported by its exporter tilt and currency hedge.

Source: FactSet, WisdomTree from 31 January 2025 to 30 January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

It is easy to look at Japan’s headline debt stock and assume the market has no room for error. The more useful lens is the direction of travel. As Japan moves further past deflation and nominal growth improves, tax revenues rise and the fiscal balance improves. The budget balance as a percentage of GDP comparison is especially telling. Japan’s deficit profile has improved markedly versus other major developed markets over the past cycle and the contrast with the post global financial crisis era is stark.

Japan’s election has not removed risk, but it has changed how risk is priced. A stronger mandate raises the odds of faster fiscal execution and reinforces strategic investment in defence, energy and technology. At the same time, governance reform continues to push corporate Japan toward higher returns on capital and higher shareholder payouts. With the BOJ normalising cautiously and the yen likely to remain a swing factor, investors may prefer targeted exposure to export-led earnings with less currency noise. In that mix, a currency hedged, dividend-weighted approach offers a disciplined way to participate in Japan’s next phase.

WisdomTree Japan Equity UCITS ETF - USD Hedged

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).