How the Iran War Is Reshaping the Macro Outlook

Publié le 13 mars 2026

Baoqi Zhu

Senior Associate, Quantitative Research and Multi Asset Solutions

Blake Heimann

Senior Associate, Quantitative Research

Points clés

- The Iran war is now driving a real energy supply disruption, not just a short-term fear spike, with Hormuz flows severely reduced and oil/LNG markets under sustained pressure.

- Central banks are likely to respond first by cutting rates less than expected, but a longer-lasting energy shock could force a tougher stance if inflation broadens and expectations rise.

- Asian equities are taking the biggest early hit from higher energy costs, while defence, rare earths, and strategic metals could emerge as relative winners in a prolonged conflict.

- Rising Gulf defence demand could support spending across the wider air-defence chain, from radars to interceptors

- Related Products WisdomTree Europe Defence UCITS ETF - EUR Acc, WisdomTree US Value UCITS ETF - USD Acc, WisdomTree Europe Value UCITS ETF - EUR Acc, WisdomTree US Equity Income UCITS ETF, WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF - USD Acc Find out more

Iran, energy prices and why duration matters more than the first oil spike

The US war in Iran has intensified rather than stabilised. The Strait of Hormuz is effectively shut in market terms, shipping attacks have multiplied, and policy attempts to calm oil have not removed the risk premium.

Iran’s new supreme leader, Mojtaba Khamenei, used his first public statement to vow that attacks would continue, to use the effective closure of the Strait of Hormuz as leverage against the US and Israel, and to consider “opening other fronts” if the war persists. That hardens the market’s conclusion that this is no longer a temporary scare about what Iran might do, but a disruption tied to what is already happening.

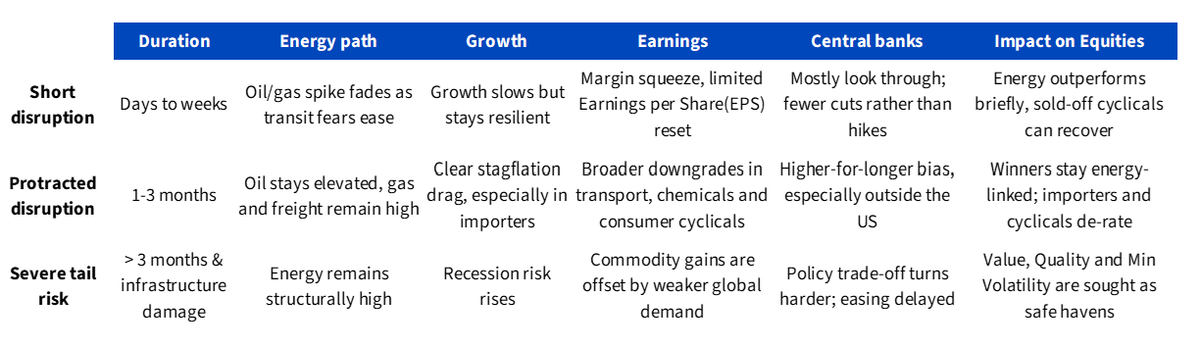

Figure 1: Scenario framework: the duration of the war determines the market outcome

Source: WisdomTree as of 12 March 2026.

The International Energy Agency (IEA) has now described the conflict as the largest supply disruption in the history of the global oil market. It says oil and product flows through Hormuz have fallen from around 20mn barrels per day (bpd) before the war to a trickle, while global LNG supply has been reduced by around 20%1 . That is the crucial macro update: the oil move is no longer just a fear premium layered on top of comfortable balances; it is being supported by a genuine interruption to physical flows.

Central banks: fewer cuts first, then a tougher reaction function if the shock persists

For central banks, the reaction function is still about persistence, not the first headline print. A short-lived energy shock can be looked through. A sustained one that lifts inflation expectations, broadens pass-through and affects wages cannot. The Federal Reserve’s (Fed) own research suggests oil shocks hit headline inflation quickly while the activity effect is initially smaller. The European Central Bank’s (ECB) updated strategy explicitly says that large, sustained inflation deviations may require a forceful or persistent policy response to stop expectations becoming de-anchored.

So, the likely sequence is first effect is fewer cuts, not automatic hikes. But the longer Brent stays, the less room the central banks have to ease. The ECB and BoE are likely to feel this constraint sooner than the Fed because Europe and the UK remain more exposed to imported energy costs, while Asia is most exposed at the regional level because around 80% of oil and oil products, and almost 90% of LNG, transiting Hormuz normally head to Asian buyers.

Equities: Asia takes the first hit, but security and scarcity are creating new winners

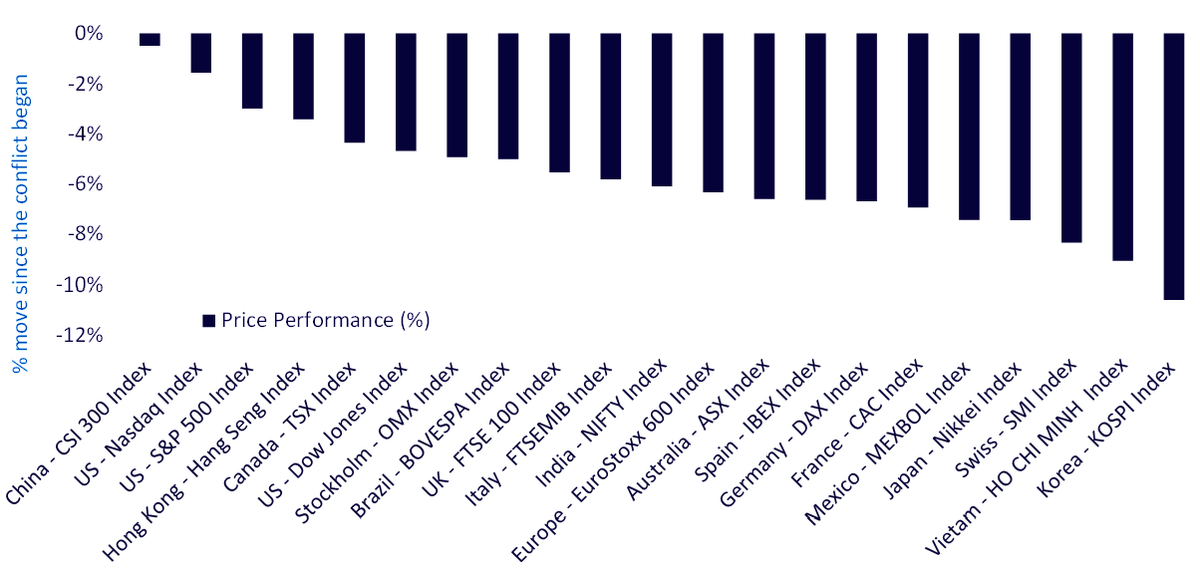

This explains why Asian equities have borne the deepest part of the initial sell-off. Higher crude, tighter LNG and a stronger dollar hit the region first through input costs, currencies and the rates backdrop. That is why Korea, Japan and Taiwan have led the drawdown, while China has been notably more resilient than its regional peers, with Chinese onshore equities falling far less than the broader Asian market in the earlier phase of the sell-off. China is a special case here: while it is not immune to higher oil prices, it has greater energy diversification compared to others, and retains significant leverage in rare-earth supply chains.

Figure 2: Relative market moves since the conflict began

Source: Bloomberg, WisdomTree from 2 March – 12 March 2026. Historical performance is not an indication of future performance, and any investments may go down in value.

At the sector level, the first losers remain the most energy- and freight-sensitive parts of the market. Airlines, transport, chemicals, packaging and the more cyclical parts of consumer discretionary, where higher fuel, feedstock and logistics costs squeeze margins before revenue estimates have even fully adjusted.

There is, however, a second-order halo effect that matters just as much for equities. Once investors begin to pay for energy security, supply resilience and strategic autonomy, the re-rating does not stop at oil and gas; it spreads into the bottleneck materials that sit behind advanced technologies, industrial supply chains and defence systems.

Positioning for Protracted Disruption

In the case where the conflict is prolonged, strategic metals miners may be set to benefit on a relative performance basis, particularly those exposed to rare earths and other hard-to-substitute inputs for advanced technologies. As governments and industrial buyers respond to the energy disruptions triggered by the conflict in Iran, the importance of securing critical supply chains is becoming clearer. The episode is a reminder that strategic materials, energy and defence technologies sit at the core of industrial and national sovereignty. Rare earth metals are key inputs for modern defence systems, including magnets used in precision targeting, radar systems, and drones. As military inventories are depleted during the conflict, demand for these materials may increase as governments seek to replenish defence equipment and munitions.

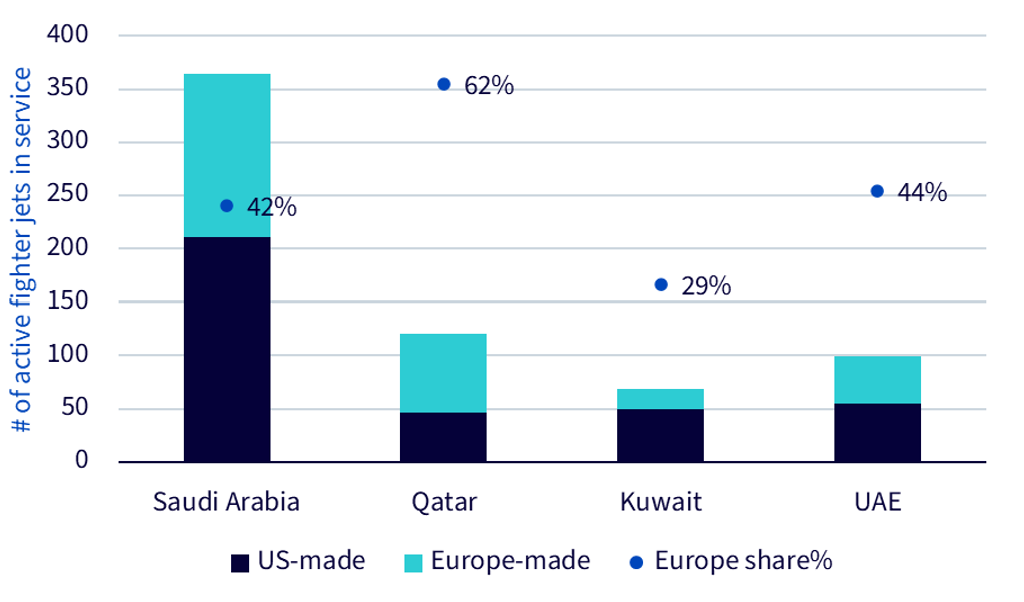

At the end of the supply chain, producers of defence equipment may also see stronger demand. Defence companies with Gulf exposure could benefit as the conflict highlights the need for more resilient, layered air-defence systems. Recent missile and drone attacks on Gulf states have underlined the importance of air surveillance, counter-drone capability and interceptor replenishment, while also exposing the cost of defending against high-volume, lower-cost threats. Beyond the traditional US suppliers, selected European and Asian suppliers are also positioned to benefit. European defence groups also have a meaningful installed base in GCC aircraft fleets. Thales has established exposure to Gulf air-surveillance radars, while Korean suppliers have already secured missile-defence contracts in Saudi Arabia and the UAE, supporting procurement diversification beyond sole reliance on US systems. The rise in demand is likely to be felt across the wider air-defence systems, from radars and command & control systems to interceptors.

Figure 3: Major GCC fighter jet fleets show meaningful European exposure

Source: Flight Global: World Air Forces 2026

Conclusion

What began as an energy shock is increasingly evolving into a broader security-of-supply shock. If the conflict endures, sustained pressure on oil and LNG markets could reshape the path for inflation, monetary policy and equity performance, raising the bar for central-bank easing and weighing on the most energy-sensitive sectors. At the same time, the disruption is accelerating the market’s focus on energy security, supply resilience and strategic autonomy. In that environment, defence systems and the rare-earth supply chains that underpin them could emerge as key areas of relative strength.

1. International Energy Agency as of 12 March 2026

À propos des contributeurs

Baoqi Zhu

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).

Blake Heimann

Senior Associate, Quantitative Research

Blake Heimann joined WisdomTree in 2020 and, in his current role as Senior Associate, supports the creation, maintenance, and reconstitution of our indices. Blake began his career in finance in 2017 as an Analyst at TD Ameritrade, and later a Quantitative Analyst with focuses on research and development of machine learning applications in finance. Blake has bachelor’s degrees in Mathematics and Economics from Iowa State University, as well as his Masters in Computer Science at Georgia Tech, with a specialization in Machine Learning. He is currently pursuing a Masters in Finance from the London School of Economics.

Aneeka Gupta

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.