AIGG LN

WisdomTree Grains

Publié le 5 juillet 2024

Over the past year agricultural commodities performance has bifurcated with soft commodities (cocoa and coffee) driving performance higher while grains (wheat, corn, soybean) lagging in performance. However, the grains sector is showing signs of recovery following nearly two years of losses. The market remains focussed on the weather. As a result of adverse weather conditions from southern Brazil to Europe and Russia, concerns are growing on building stock levels. At the same time, high net short positioning levels across corn and soybeans, ahead of a challenging growing season are ripe for a short covering rally.

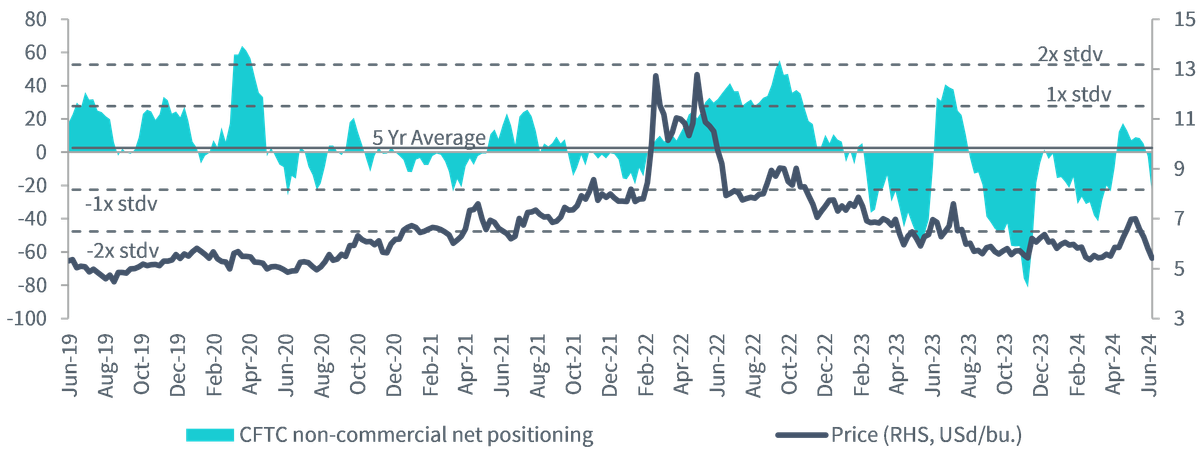

Wheat prices hit multi month highs in May owing to multiple factors at different global origins of wheat. In Canada, union workers at two of the leading rail companies voted to strike after unsuccessful labour negotiations that led to upward price pressure for wheat. Yet better crop prospects in Australia and the US have lent some pressure to wheat prices.

The Australian crop outlook has changed since the start of the year, especially in light of the official end of El Nino. The market is in consensus that wheat acreage in Australia will be increasing at the expense of canola crops. Since the beginning of June, Australia has witnessed good rainfall over most of western Australia keeping soil moisture levels high. So, Australia is well placed to produce more wheat than the last season. In the US, improved crop prospects and rising inventories are also weighing on wheat prices.

However, in Russia, the world’s largest exporter of wheat, production cuts are lending buoyancy to wheat prices. SovEcon the Russian consultancy has cut its crop forecast this week to 80.7mn tons. While the United States Department of Agriculture (USDA) expects a slightly higher global wheat crop compared to 2023/24 ending stocks are still expected to fall by almost 6mn tons, resulting in a significant tightening of the supply situation.

USDA raised its estimate for global consumption by 2mn tons to a record 802.4mn as food, seed and industrial use are expected to continue growing. The initial projections from USDA show global wheat demand exceeding production by over 4mn tons.

Net speculative futures in wheat have remained volatile moving from net long to net short since April 2024 reflecting the changing fundamental owing to adverse weather conditions.

Source: Bloomberg, Commodity Futures Trading Commission, WisdomTree as of 25 June 2024. Historical performance is not an indication of future performance and any investments may go down in value.

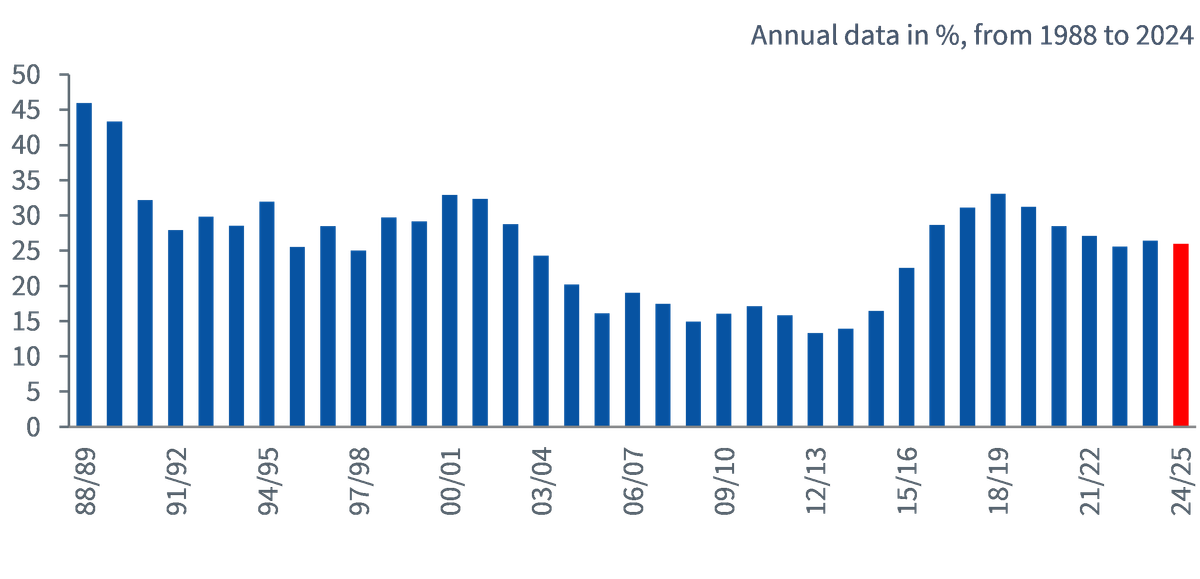

The US acreage is said to amount to 91.5mn acres, (3% lower than the prior year). This is likely to result in a higher US corn crop than previously forecast provided the yields per acre remain unchanged. Corn supply in the US remain plentiful. US corn stocks stood at just under 5Bn bushels, 22% higher than the prior year1. Corn stocks to use ratio (i.e. how much supply we have at the end of the year with respect to how much we use annually) remains low at 25.98 as highlighted below:

Source: Bloomberg, USDA, WisdomTree as of 25 June 2024. Historical performance is not an indication of future performance and any investments may go down in value.

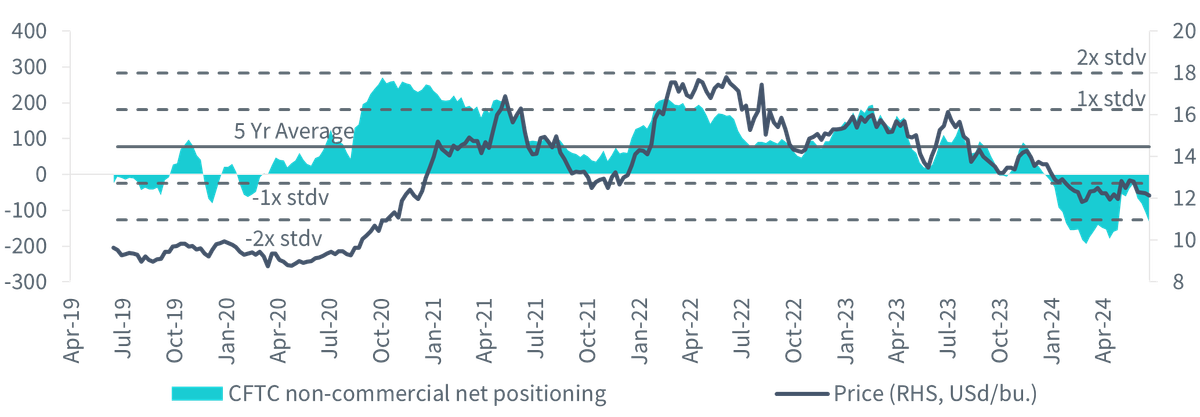

Soybean prices have been under pressure owing to plentiful stocks. Higher US supplies are also expected for soybeans. US soybean stocks amounted to 970mn bushels, 22% higher than the prior year2. The USDA reported a 3% annual increase in US acreage this year to 86.1mn acres3.This means that the area planted with soybeans is slightly lower than expected in a survey of US farmers in the spring. Soybean supplies in Argentina are also plentiful. The harvest in Argentina reached its highest level in five years in the completed 2023/24 season4.

Reflecting the weaker sentiment on the soybean market, net speculative positioning in soybean is more than 2-standard deviations below the 5-year average as highlighted below:

Source: Bloomberg, Commodity Futures Trading Commission, WisdomTree as of 25 June 2024. Historical performance is not an indication of future performance and any investments may go down in value.

1 USDA as of June 1, 2024

2 USDA as of 1 June 2024

3 USDA as of 30 June 2024

4 Buenos Aires Grain Exchange

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.