Defensive Assets: It is easier not to lose money than to win it back

Publié le 25 mars 2020

Head of Research, WisdomTree Europe.

This blog is the seventh instalment of our blog series on Defensive Assets: ‘Offence wins games but defence wins championships’.

We have spent the last 6 weeks reviewing assets that offer defensiveness and asymmetry across asset classes. At the same time, markets have given us a real time demonstration of how such assets can help shield portfolios from some of the pain. We have seen for example that long duration US Treasury strongly rebounded initially, thanks to the Federal reserve swift interventions and despite the recent correction in yields, US Treasury 10+ is still up 20.69% year to date at the time of writing (24th march 2020). Gold also behaved very well initially and then suffered from the liquidity squeeze but it is also up 6.01% at the time of writing. Overall, they both helped to cushion well prepared multi asset portfolios from the brunt of the equity losses (MSCI World net TR Index in USD is down 25.84% over the same time frame). This instalment will focus on illustrating how such assets could be used in portfolios.

The following analysis is done from the point of view of a euro-based investor, but similar work could be done in any currency. As a first step, we will show a few example portfolios aiming to improve resilience through pure asset selection i.e. replacing traditional investments by more conservative assets without changing the overall asset allocation. This will allow us to analyse the overall impact of such changes. We will focus next week on a more dynamic approach introducing systematic asset allocation strategies that use rule-based mechanisms to create defensiveness like Vol Targeting (regular rebalancing between high volatility and low volatility assets to maintain risk around a certain level), Capital Protection mechanism (Constant Proportion Portfolio Insurance….). In this instalment we will illustrate:

- how some example defensive portfolios can potentially outperform more offensive portfolios over the long term

- how a well balanced risk return profile can improve the long term prospects for investors

We will also look at recent performance to see how those example portfolios would have behaved in the last weeks and months.

Defensiveness through asset selection

Avoiding loss and smoothing returns are some of the main objectives when it comes to asset allocation. This is why so many investors have adopted a 60/40 portfolio which mix 40% of safer assets such as Bonds and 60% or higher risk asset like equities or commodities as benchmark. This mix aims to provide exposure to the historically superior returns exhibited by equities, meanwhile also granting the diversification benefits available in Fixed Income assets. In this blog, we will use a euro focused, diversified 60/40 portfolio as the standard to which to compare some illustrative defensive portfolios. Building on our previous instalments’ findings, we will use the following two portfolios as example. The first one, the Illustrative Recession Portfolio, will focus on risk reduction only without focusing on the rest of our framework i.e. asymmetry & upside potential, or valuations. The second, The Illustrative Defensive Portfolio will aim to invest in the assets that our framework has uncovered i.e. assets that balance risk reduction and upside potential to deliver a more versatile investment profile, which can be more suited to uncertain times.

In the Illustrative Recession Portfolio, we start by replacing the European equities by a Min Volatility approach to developed equities in an unhedged version. This will benefit the portfolio in 3 ways:

1. the geographical diversification away from Europe will improve the risk-return profile

2. the Min Volatility approach will create strong defensiveness as described earlier

3. the currency exposure, heavily skewed towards USD and JPY, will also add some protection

In Fixed Income, we focus on the assets with the strongest risk reduction potential as highlighted in previous weeks, high rating local government bonds and government bonds in a safe-haven currency. Finally, we add extra diversification using Gold unhedged in US dollars. Such exposure coudl help the portfolio through the defensiveness of Gold but also the US dollar.

In the Illustrative Defensive Portfolio, we want to illustrate the potential advantages of more asymmetric assets (as listed in the previous instalments of this blog series) We have therefore focused on developed equities with a quality twist using WisdomTree proprietary approach. This approach will deliver similar geographical diversification and safe haven currency exposure as in the Illustrative Recession Portfolio but with an equity style that tend to be more all-weather than Min Volatility and therefore tend to deliver some risk reduction with some upside retention. In this example portfolio, we have also tried to increase diversification by introducing some Gold but also some Enhanced Commodities. Finally, in the Fixed Income pocket, we focus on two strategies: The Bloomberg Barclays US Aggregate index to benefit from the usual defensiveness of the USD dollars and US Treasuries but keeping US Corporates for the upside potential. And the EUR Treasury Enhanced Yield which could deliver to the portfolio the risk reduction of government bonds but with extra duration which could add diversification and extra yield which could improve the long term.

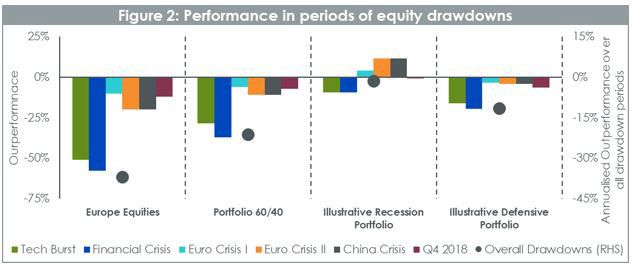

Reducing drawdowns with the Illustrative Recession and Illustrative Defensive Portfolios

In figure 2, we focus on the performance of the 3 example portfolios (rebalanced to their initial weights to make sure that weights do not drift) during the 6 drawdown periods. As expected, the 60/40 portfolio improves on pure equity but not by that much. The Illustrative Recession Portfolio exhibits performance in line with expectations with positive performance in 3 periods and only limited drawdowns in the other 3. The Illustrative Defensive portfolios sit a little bit in the middle with 6 significantly reduced drawdowns.

As discussed in the first blog of this series, most investors do not have a crystal ball to tell them when to switch in very defensive assets like cash i.e. just before the drawdown. Therefore, they would need to stay invested in that type of assets for long periods in preparation for possible shocks. This is why it is important to balance the risk reduction with the upside potential of the considered investments. While Figure 2 focuses exclusively on performance in equity drawdowns, in Figure 3, we use a more holistic approach to compare the 3 example portfolios, looking at performance across business cycles. Through that lens, the advantages of the example portfolios appear very clearly. In Figure 3, we have split the last 20 years into 4 types of periods using the Organisation for Economic Co-operation and Development (“OECD”) Composite Leading indicator (“CLI”). The CLI has been designed to decrease a few months before the economy starts to slow down or increase before the economy restarts. So, a strong decline in CLI tends to indicate a probable downturn in equity markets for example. Clearly, the Portfolio 60/40 is merely a diluted version of Equities. The other 2 example portfolios, on the other hand, exhibit unique behaviours. The Illustrative Recession Portfolio is very steady with small increase in all type of periods being strong decline in CLI or strong increase (similar to what cash could deliver). The Illustrative Defensive Portfolio, however, exhibits strong risk reduction in period of economic slowdown but also good performance in period of economic boom. By focusing on asymmetric assets, such a portfolio aims to deliver an all-weather type of behaviour.

It is easier not to lose money than to win it back

Figure 4 highlights the value of being defensive over the long term. Over almost 20 years both example portfolios beat the 60/40 mix despite the last 10-year bull run and despite the fact that they exhibit on average worse performance in good economic times (See Figure 3). This is driven by an often-overlooked fact: to regain the money lost in a 50% drawdown, an asset needs to gain 100%. So, if a volatile asset were to lose 50% and then gain 50% the overall performance is -25%. If a less volatile asset loses 15% and then gain back that 15 % then the overall performance is only -2%. This simple mathematical rule gives a fundamental advantage to more risk conscious portfolios. In Figure 4, the Illustrative Recession Portfolio is doing very well almost entirely because it did not lose money in 2008. Since March 2009, it has increased by 161% only compared to 222% for Equities. The Illustrative Defensive Portfolio is doing the best of all with the highest returns and lowest volatility despite showing a higher beta than the Illustrative Recession Portfolio because it is more balanced and benefits from both sides i.e. lower drawdown and positive beta to economic improvements.

The results above are at the end of last year (2019) but what happened since them? Year to date (at the time of writing, 24th March 2020), European equities are down -26.5% and the Portfolio 60/40 is down -16.67% for that period. Both the example portfolios are doing significantly better, the Illustrative Recession Portfolio is down -3.98% and is outperforming the Illustrative Defensive portfolio which is down -10.3%. That is to be expected with the sharp downturn in the markets that we have experienced in the last few weeks. However, being invested in a very defensive asset like the Illustrative Recession Portfolio starting in January this year would have been tricky. Markets were soaring up to this point and timing a switch from higher beta to lower beta exposure early this year would have been very hard. Assuming that investors have kept similar exposures for Q4 2019 and Q1 2020, we observe that the Illustrative Defensive Portfolio would have lost -6.44% versus -5.34% for the Illustrative Recession Portfolio illustrating further than investors would have been better off investing in more balanced investments. It is worth noting that the Portfolio 60/40, delivered -14.35% over those 2 quarters. This gives us a real life example of the advantages of all weather type investment of which the Illustrative Defensive Portfolio is an example, with its good defensiveness in Q1 and good upside profile in Q4 2019.

In the final instalment of the series, we will look at the problem of defensiveness through a different lens by focusing on dynamic asset allocation instead of asset selection.

Unless otherwise stated, data source is Bloomberg, as of 31 December 2019.

+ Defensive Assets: Is playing too safe too risky?

+ Defensive Assets: Are all equity strategies created equal?

+ Defensive Assets: The duration your portfolio needs

+ Risk-on or Risk-off, what is driving currency performance?

+ Defensive Assets: Currencies, a powerful tactical overlay

+ Defensive Assets: Gold, a precious ally in the fight against equity drawdown

Related products

À propos du contributeur

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.