Diversified exposure

Provides diversified and targeted access to key metal commodities that are involved in energy transition technologies.

The world is becoming increasingly energy-hungry and the story is no longer just a ‘transition’ from one energy system to another. A more accurate framing is energy addition: total energy demand keeps rising, and a meaningful share of new renewable capacity is being built to meet incremental demand, not simply to replace legacy sources. Six forces are driving demand. First, we are in an era of energy addition: total energy demand is rising as economies grow and electrify, and a meaningful share of new renewables is being built to meet incremental demand rather than simply replace legacy supply. Second, decarbonisation and electrification are scaling, driving a metals-intensive buildout across renewables, batteries and grid infrastructure. Third, energy security has become a dominant policy priority since the Russia-Ukraine war, accelerating diversification of supply and ‘friend-shoring’ efforts that are infrastructure-heavy and metals-intensive. Fourth, data centres are contributing to sustained growth in electricity demand and in some regions, already creating localised constraints that require incremental generation and grid reinforcement. Fifth, artificial intelligence (AI) acts as an additional catalyst because AI workloads are materially more power intensive than traditional computing, amplifying the need for generation and grid investment as deployment scales. Sixth, two technology trends continue to raise metals intensity across the economy: 5G rollout (connectivity and wiring) and evolving vehicle technology (greater electrification, higher electronic content and lightweighting).

The result is a broader, more durable demand backdrop: decarbonisation, energy security, electrification and digital infrastructure are now reinforcing each other, supporting the case for strategic metals exposure.

Several years ago WisdomTree recognised that the growth engine for strategic metals extends beyond a single policy goal. As the global economy electrifies and the buildout of renewables, grids, data centres and advanced technologies accelerates, metals increasingly function like the enabling infrastructure of the modern energy system. This inspired us to build a differentiated suite of exposures that allow investors to access the theme through both commodities and equities, supported by our long-standing expertise in commodities and thematics investing, informed by our partnership with Wood Mackenzie, a leading energy and metals research consulting firm.

The WisdomTree Strategic Metals UCITS ETF (WENU) provides refined exposure to a diversified basket of metals that sit at the heart of electrification and ‘energy addition.’ The approach is not just a static demand story. It is constructed to be sensitive to supply-demand balance considerations, reflecting how these markets can tighten (or loosen) as supply responds slowly to new demand and bottlenecks emerge across mining and processing.

The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (RARE) provides diversified, yet targeted access to the miners that underpin strategic metals and rare earth supply chains. It is built to capture the theme’s breadth across multiple demand engines (from renewables and grids to AI linked electricity growth), while acknowledging the reality that supply chains are being re-priced through the lens of security and resilience as well as decarbonisation. The result is an equity allocation aimed at gaining exposure to the companies most aligned with the strategic metals supply chain opportunity, rather than relying on simple market-cap construction.

Together, the WisdomTree Strategic Metals UCITS ETF and the WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF are intended to reflect the updated reality of the theme: metals are not only inputs to the energy transition, they are foundational to energy security, electrification and powering modern technologies.

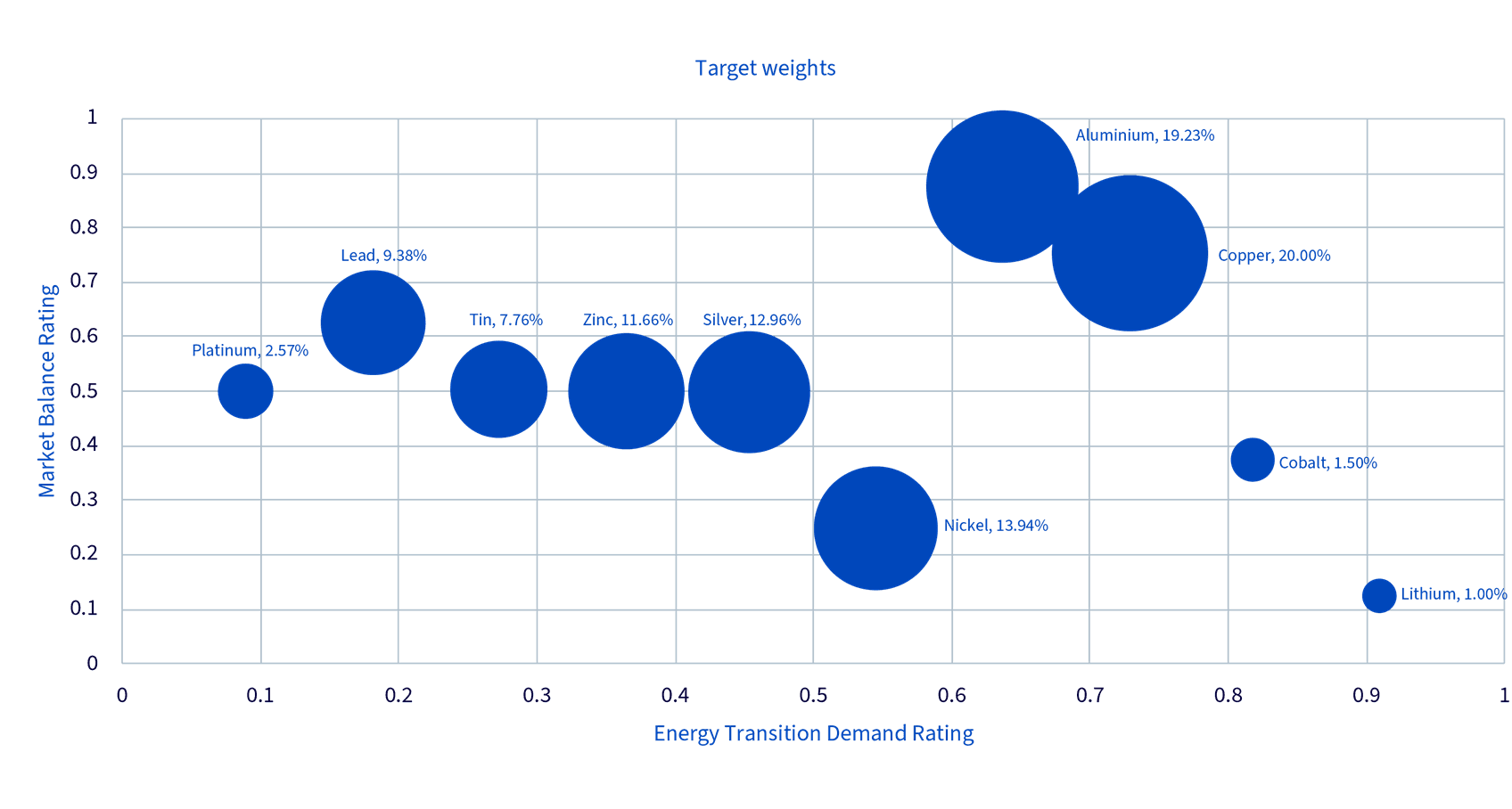

The WisdomTree Strategic Metals UCITS ETF provides exposure to a basket of liquid tradable metals that are central to electrification, energy addition and the buildout of modern infrastructure, including copper, aluminium, nickel, silver, zinc, lead, tin, platinum, cobalt and lithium, among others. The selection and weighting of the underlying metals is informed by expected demand growth across these end markets, while also taking account of near-term supply dynamics, recognising that strategic metals prices can be highly sensitive to periods of tightening or oversupply.

Source: WisdomTree, Wood Mackenzie, based on forecasts created July 2025. Bubble size represents the target weight. Market balance ratings is not considered for precious metals and is not available for tin. For the purpose of the chart construction, we set the Market balance rating at the midpoint (0.5) for these metals. Cobalt and Lithium weights are capped due to liquidity considerations at 1.5% and 1.0% respectively. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

For more information, read the methodology of the underlying index tracked by this ETF.

WENU

WENU is designed to provide investors with a total return exposure to a diversified basket of Energy Transition Metal futures contracts. The selection and weighting of metals is driven by the demand growth forecast in the energy transition while considering near-term supply overhangs or tightness.

WENH

WENH seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Energy Transition Metals Commodity UCITS Total Return Index. Currency volatility is minimised through the use of currency forward contracts (EUR hedged).

WENG

WENG seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Energy Transition Metals Commodity UCITS Total Return Index. Currency volatility is minimised through the use of currency forward contracts (GBP hedged).

WENP

WENP seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Energy Transition Metals Commodity UCITS Total Return Index. Currency volatility is minimised through the use of currency forward contracts (GBP hedged).

WisdomTree has extended its thematic equities and commodities partnership in the energy transition space with Wood Mackenzie to offer a solution in renewable energy. Wood Mackenzie is a leading energy transition research and consulting firm that has been providing quality data, analytics, and insights used to power the energy, renewables, and natural resources industry for nearly 50 years.

Their expertise in topics including energy, chemicals, metals and mining, and power and renewables make Wood Mackenzie an ideal partner to offer pure exposure to this rapidly evolving theme.

Learn more about Wood Mackenzie.

Mobeen Tahir

In the latest episode of The Next Big Thing podcast, we hosted Ryan Corbett, Chief Financial Officer of MP Materials, one of the most strategically important companies in the rare earths space. We discussed why rare earths sit at the centre of the supply chain reset, why NdPr is the real bottleneck, and how demand is broadening well beyond electric vehicles (EVs) into robotics, drones, AI infrastructure and defence. Ryan also explained why scale, policy support and vertical integration matter so much in a market still dominated by China. This blog summarises the key messages Ryan delivered on the show.

Aneeka Gupta

The latest rebalance of WisdomTree's Strategic Metals and Rare Earths Miners Index widens its lens from 10 to 14 metal categories, adding vanadium, silicon metal, manganese and niobium. It trims copper and lithium, lifts rare earths and nickel, tilts toward upstream mining and larger names, and now offers above-market growth at a discounted forward earnings multiple.

Mobeen Tahir

Lithium was once a laboratory curiosity. Today, it sits at the centre of the global shift towards electrification and digitalisation. As electric vehicles scale, battery storage expands, and industrial demand evolves, lithium demand is projected to rise meaningfully over the coming decades. Yet supply growth is expected to slow and remains concentrated in a handful of countries. In this blog, we break down the demand and supply outlook using International Energy Agency projections, with additional insight from our partners at Wood Mackenzie, and explore what this could mean for investors.

Mobeen Tahir

In the latest episode of our podcast, The Next Big Thing, Chris and I spoke with Ana Cabral, Chief Executive Officer of Sigma Lithium. We discussed how lithium sits at the heart of an increasingly electrified world, why low-cost and sustainable production is what separates winners from the rest, and how new sources of demand, from EVs to data centres and drones, are reshaping the market. Ana also shared how Sigma has built one of the world’s lowest-cost lithium operations while rethinking how mining can be done, using technology, process design and discipline to navigate a volatile commodity cycle.