AIGI LN

WisdomTree Industrial Metals

Veröffentlicht am 15. Mai 2026

Agricultural commodity markets are experiencing a significant re-rating in 2026. The Bloomberg Commodity Agriculture Index has returned 13.4% Year to Date1, driven by a confluence of supply side shocks – a rising probability of an El Niño event disrupting growing conditions across three continents and the Iran war’s disruption to shipping through the Strait of Hormuz. These forces are not independent; they interact and reinforce each other and together they are reshaping the near term supply outlook across the agricultural commodity complex.

This year alone the WisdomTree Agriculture ETC (Ticker: AIGA) has attracted US$1.2bn in inflows, taking the assets under management to US$1.4bn underscoring the growing institutional interest in diversified agricultural commodity exposure. The WisdomTree Agriculture ETC (Ticker: AIGA) tracks the Bloomberg Agriculture Subindex Total Return (Ticker: BCOMAGTR Index) comprising futures on coffee, cocoa, corn, cotton, soybeans, soybean oil, soybean meal, sugar, and wheat. It reflects the return on fully collateralised futures positions, quoted in USD. The fund's diversified basket construction means investors gain access to the broad agricultural commodity complex, capturing the notable gains in soybean oil (+56.6%), cotton (+21.5%), and wheat (+31.2%)2, while spreading risk across eight commodities rather than concentrating in any single position.

Agricultural commodities can be highly volatile and may be affected by weather events, geopolitical developments, currency movements, regulatory changes and fluctuations in global demand. Commodity ETCs may experience significant price swings and investors may lose some or all of their investment.

Discussion of the Strait of Hormuz typically centres on oil. Less well understood is its parallel role in global fertilizer supply. The Persian Gulf nations — Iran, Qatar, Saudi Arabia, and the UAE — collectively represent one of the largest regional exporter of nitrogen fertilizers globally, a position reinforced after Russia's partial exit from normal trading channels following 2022. The Strait is the sole maritime exit for all of them. The scale of fertilizer exposure through the Strait is material:

The Food Agricultural Organisation (FAO) has confirmed a developing fertilizer shortage across Asia and the Global South, with India, Bangladesh, Egypt, Sudan, and parts of Sub-Saharan Africa among the most affected regions. The key analytical point is the lag between the disruption and its harvest impact. Shipping delays from the Gulf to the Indian subcontinent run approximately 30 days, meaning supply shortfalls in March affected April and May planting windows, with the full harvest consequences not expected to become visible in production data until Q3–Q4 2026. Four transmission channels are most relevant for AIGA's constituent commodities:

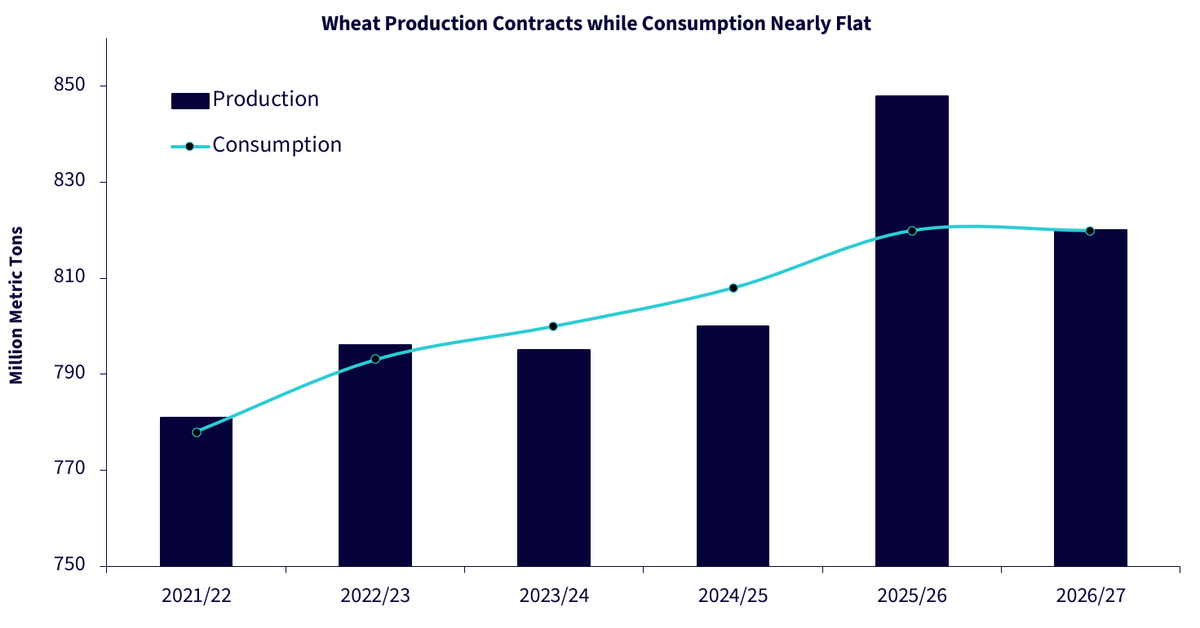

Source: USDA Grain: World Markets and Trade report as of May 2026.

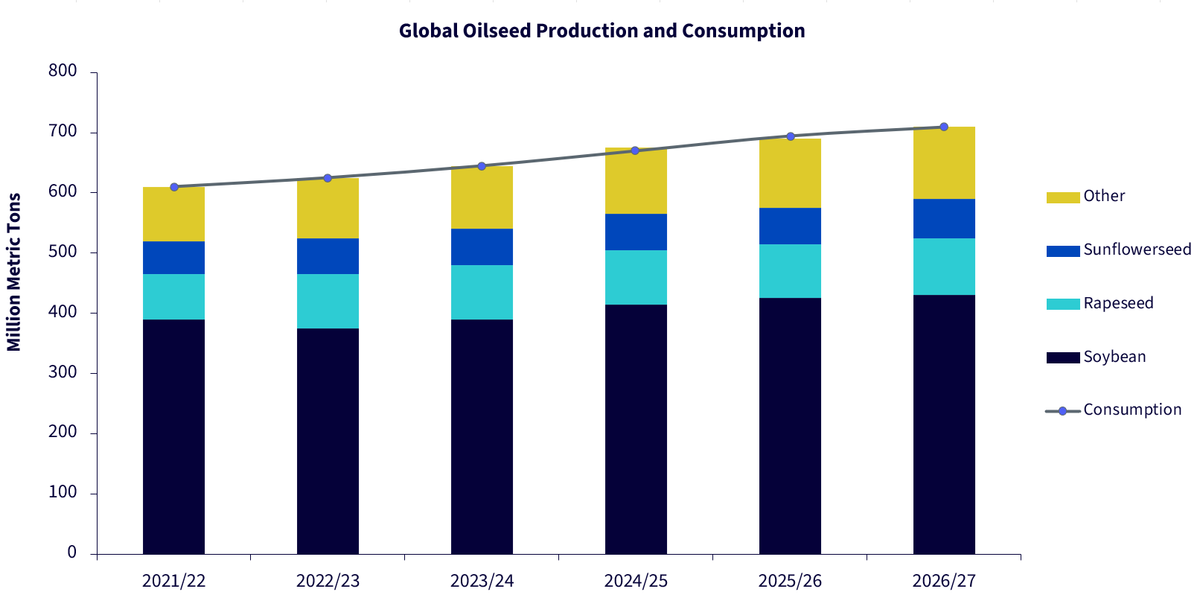

Source: USDA Oilseeds: World Markets and Trade report as of May 2026.

An El Niño event is widely expected to develop during mid-2026. An El Niño weather event is triggered by a warming of a region in the Pacific Ocean, which drives a change in trade wind patterns around the world. Some places become hotter than normal. Other places become cooler than normal. Some places become wetter than normal, while others become drier. The key issue is that a weather deviation from normal has the potential to adversely affect crop yields. The World Meteorological Organisation’s (WMO) April 2026 Global Seasonal Climate Update signals rapidly rising sea-surface temperatures in the Equatorial Pacific, with National Oceanic and Atmospheric Administration’s (NOAA) Climate Prediction Centre assigning a 82% probability to El Niño onset during May–July 2026 (vs 61% probability in their April report). Its significance in the current context is that it has the potential to reduce agricultural crop yields in the same producing regions that would otherwise have helped offset the input cost pressures arising from the Hormuz disruption. Both forces are pulling in the same direction at the same time.

What matters more is the timing and the baseline from which this event is developing. 2025 was cooler than 2024 due to a La Nina phase, despite being one of the warmest years on record overall. That La Niña induced cooling was always temporary. 2024 was the hottest year on record9 with global average surface temperatures 1.55 degrees above the 1850-1900 average, characterised by exceptional land and sea surface temperatures and ocean heat. Agricultural systems are already operating under stress from that elevated baseline and the return of El Niño layered on top of it compounds the risk materially.

Critically, the weather effects of El Niño tend to peak during December, but the impact typically takes time to spread across the globe. Much of the agricultural damage from an event that peaks in the northern hemisphere winter manifests in the following growing season, meaning stress that is already appearing in agricultural systems today is likely to intensify before it eases. Historical data shows there is typically a 6–12-month lag between the peak of an El Niño event and the peak of the production impact. Historically, agricultural commodity markets have often repriced ahead of confirmed production impacts, as markets tend to react in anticipation of tightening supply conditions.

Historically, soft commodities have often shown heightened sensitivity. Soft commodities have consistently been the strongest performers during El Niño episodes, three of the five soft commodities (cotton, coffee, and sugar) moved to multi-year highs in 2022–23, and in late 2024 orange juice and cocoa reached record highs while coffee reached a record high in 202510. Every strong El Niño in the past 55 years has reduced global cocoa production, with Ecuador and Indonesia the most exposed origins and significant risks in West Africa (where most of the world’s production is now concentrated).

For investors who wish to access the soft commodity dimension of the El Niño thesis more directly, WisdomTree offers a complementary product to AIGA via the WisdomTree Softs ETC (Ticker: AIGS). WisdomTree Softs is a fully collateralised, UCITS-eligible Exchange Traded Commodity (ETC) designed to provide investors with total return exposure to a basket of softs futures contracts. The ETC aims to replicate the Bloomberg Commodity Softs Subindex 4W Total Return Index (Ticker: BCOMSO4T). The index is composed of futures contracts on coffee, cotton, and sugar.

The agricultural commodity complex in 2026 is being shaped by two supply-side forces that are unusual both in their scale and in the way they interact. The Hormuz fertilizer disruption is affecting input costs and planting decisions in real time, with consequences that will continue to emerge in harvest data through Q3–Q4 2026 and into 2027. The developing El Niño is adding a climate layer on top of a temperature baseline that is structurally higher than any previous episode — and its production impact, when it arrives, will follow with a 6–12-month lag from peak.

1Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

2Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

3CRU as of 15 March 2026

4Argus Media as of 31 March 2026

5Energy Information Administration, June 2025

6United States Department of Agriculture (USDA) May World Agriculture Supply and Demand Estimates (WASDE) Report as of 12 May 2026

7United Stated Department of Agriculture as of May 2026

8Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

9World Meteorological Organization (WMO)

10Bloomberg Finance L.P. as of 31 March 2024

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.