USEU IM

WisdomTree Short USD Long EUR

Published 30 January 2026

Director, Digital Assets Research

Senior Associate, Quantitative Research and Multi Asset Solutions

The US dollar is weakening in a slow, structural way. The Japanese yen is strengthening in bursts, then snapping back. Together, they signal a regime shift: currency is no longer a passive backdrop. It is an active driver of portfolio risk and return.

This is not a foreign exchange (FX) trading story. It is a portfolio construction problem, with implications across equities, bonds, commodities and diversification itself.

The US dollar (USD) has been under pressure for months. Short-term rallies still occur, but they are increasingly tactical rather than trend-defining. The broader picture is one of gradual erosion.

Several forces are working against the US dollar:

One simple market check is US Dollar Index (DXY) . which has been trending lower into early 2026 and has reached its lowest level since 2022. This supports the idea that USD weakness is broad-based rather than solely driven by a single currency pair.

Source: Bloomberg, as of 27 January 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investments may go down in value.

The US dollar does not need to collapse to matter. A slow, grinding decline is enough to reshape global portfolio outcomes. It quietly boosts assets that tend to move inversely to USD, most notably gold, while eroding USD-based returns on overseas assets. Currency is no longer a background variable. It is becoming a first-order driver of returns.

The Japanese yen (JPY) has re-entered investor focus, but not as a stable safe haven. Instead, it has become hypersensitive to policy signals and shifts in global risk sentiment.

Key dynamics include:

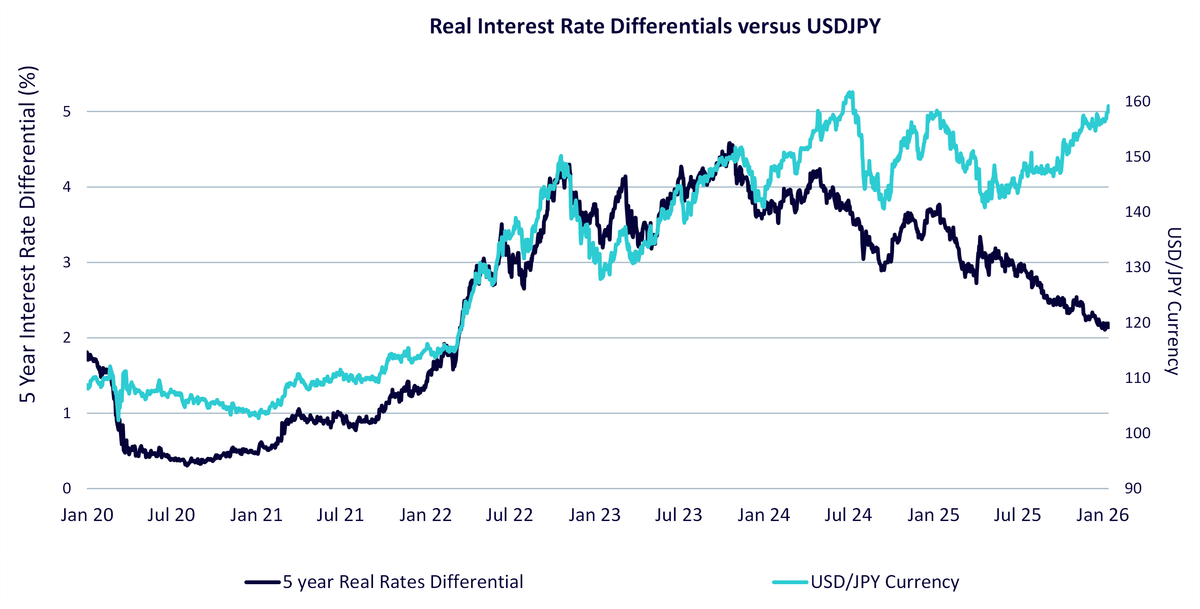

From market data perspective, the USD-JPY real yield differential remains positive, but it has been trending lower. The compression from around 3% in mid-2024 toward roughly 1.5% at the end of January 2026 reduces the rates tailwind behind USDJPY. At the same time, JPY 3-month forward carry remains negative, but it is far less negative than in 2022–2023. That shrinking carry cushion makes “short JPY” positioning more fragile and increases the probability of sharp, stop-driven JPY rallies.

Source: Bloomberg, WisdomTree as of 16 January 2026. USD-JPY real yield differential is calculated as (US 5y nominal Treasury yield - US 5y inflation swap rate) - (Japan 5y nominal JGB yield - Japan 5y inflation swap rate). You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investments may go down in value.

Near term, the directional message is less “yen steadily stronger” and more “yen strength arrives in jolts”. In practice, that means downside risks in USDJPY (sudden JPY strength) are more likely than a smooth trend, even if the pair remains range-bound overall.

A key development is that intervention risk is no longer solely a Japan story. Recent reporting suggested “rate checks” in USDJPY by Japanese authorities and unusually by the New York Fed’s FX desk acting as agent for the US Treasury. While this is not the same as actual intervention, it increases the probability of coordinated action if USDJPY re-tests the highs. The practical implication is a near-term “soft ceiling” on USDJPY: authorities appear more willing to lean against one-way yen weakness, which raises the odds of abrupt JPY-strength episodes even if the broader trend remains choppy.

What has changed is that USD weakness and JPY strength are no longer separate stories.

When US yields fall or global risk sentiment deteriorates:

But when markets question the Bank of Japan’s resolve or economic constraints:

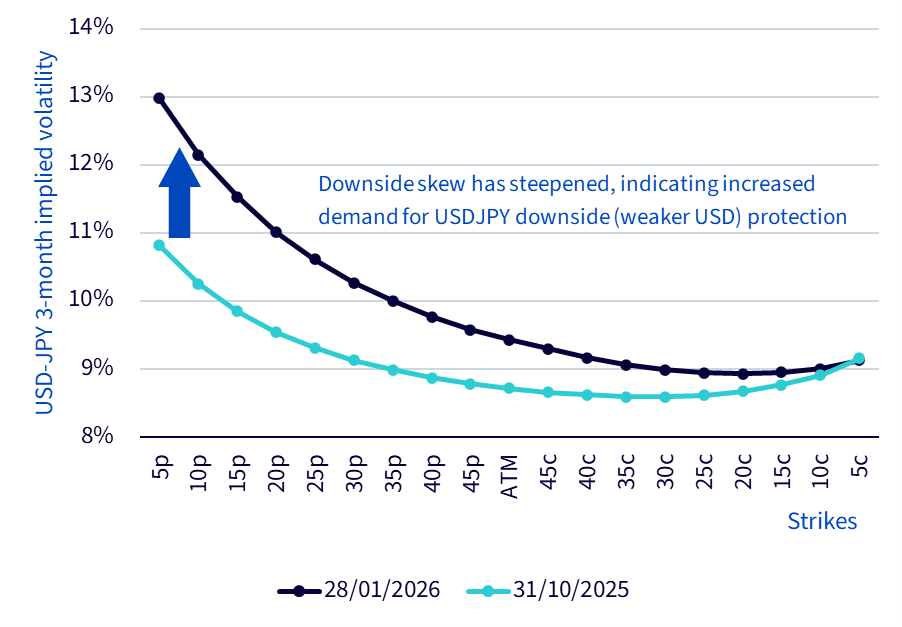

The outcome is a regime of short, sharp currency moves, not long, predictable trends. That makes currency risk harder to ignore and harder to sit through passively. From a market data perspective, USDJPY 3-month implied volatility is higher than late October 2025, and the downside wing is richer. That is consistent with investors paying up for protection against abrupt JPY-strength episodes, rather than just pricing symmetric two-way uncertainty.

Source: Bloomberg, as of 28 January 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investments may go down in value.

For diversified portfolios, this matters. Currency volatility can now amplify drawdowns, dilute returns and undermine assumptions about diversification, even when underlying assets perform as expected.

The mistake is to treat this as an FX trading issue. It is not. It is a portfolio design problem.

Investors need to be more deliberate about how currency exposure enters their portfolios:

In a world where US dollar weakness is becoming structural and Japanese yen moves are abrupt and policy-driven, and now increasingly intervention-shaped, ignoring currency exposure is no longer neutral. It is an active decision.

Investors who manage currency deliberately through currency-hedged share classes and currency ETPs are better positioned to control risk, sharpen returns and remain flexible as macro conditions continue to shift.

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.