DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Published 5 December 2025

Director, Digital Assets Research

At the start of December 2025, Bank of Japan (BoJ) Governor Kazuo Ueda delivered his clearest signal yet that a rate hike may be imminent. Markets reacted instantly and the Japanese yen (JPY) jumped roughly 0.6% against the US dollar (USD) as investors recalibrated expectations for Japan’s policy path.

For a currency long used as the world’s cheapest source of funding, even subtle shifts matter. With Japan now deep into its first tightening cycle in decades, those signals point toward one dominant theme: the unwinding of the yen carry trade.

The yen carry trade is built on a simple idea: borrow in Japan at very low rates and deploy the capital into higher-yielding assets abroad. But that simplicity masks growing vulnerabilities as Japan exits its era of ultra-easy money.

Bank for International Settlements (BIS) data shows yen-denominated credit to non-residents grew 6% year-on-year in Q1 2025, reaching JPY 65.6 trillion1. Growth remains positive, but it has slowed steadily since Q3 2024, right after Japan began tightening and carry exposures began to unwind. This marked a clear downshift from the double-digit annual expansions seen in the years prior.

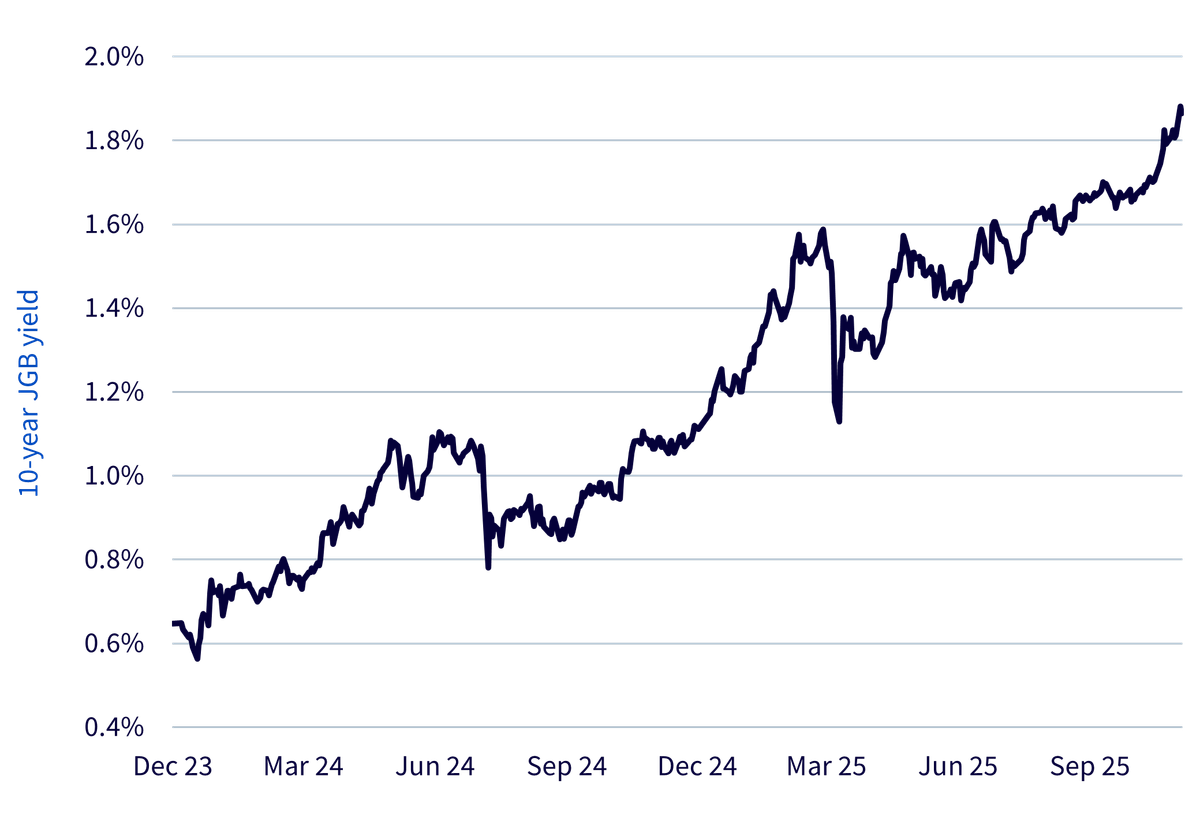

Source: Interest Rate : Ministry of Finance. 02 December 2025. Historical performance is not an indication of future performance, and any investment may go down in value.

As Figure 1 illustrates, the 10-year Japanese Government Bond (JGB) yield climbed from 0.65% at the end of 2023 to 1.86% by early December 20252. The ascent reflects a decisive departure from ultra-accommodative policy. First through adjustments to Yield Curve Control, then its removal, and finally the BoJ’s early rate hikes and reduced bond purchases.

The 10-year JGB has become a clean visual proxy for a regime shift as markets are now pricing in sustainably positive inflation and wage growth, after decades where deflation was the norm.

With monetary tightening underway and funding costs rising, the debate is no longer if the carry trade unwinds, but how. Markets will price the difference aggressively.

If the unwind remains gradual:

Under this path, capital still rotates back toward Japan, but repositioning can occur over months, not hours.

If the unwind accelerates:

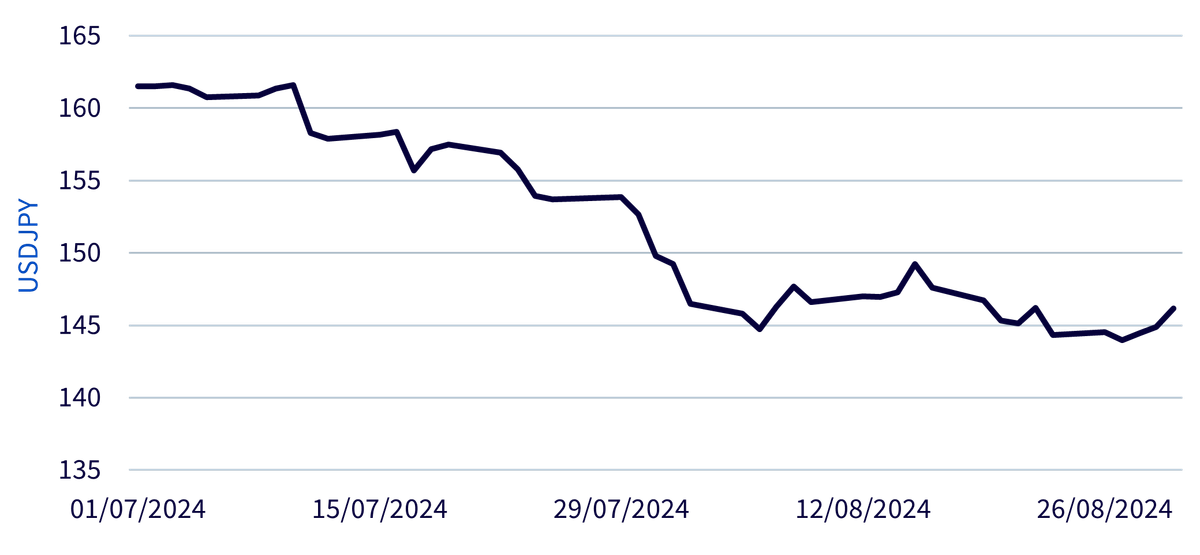

Markets already saw a preview. In August 2024, the yen strengthened roughly 6% within days3, slicing through carry exposures across asset classes. That is a reminder of how quickly positioning can unravel when funding conditions turn.

Source: Optuma, WisdomTree. 02 December 2025. Historical performance is not an indication of future performance, and any investment may go down in value.

What comes next reflects structural policy realignment, not a transient data point.

As currency volatility rises and carry trades unwind, the case for currency-hedged exposure to Japan becomes stronger.

WisdomTree Japan Equity UCITS ETF (DXJ) provides targeted access to dividend-paying, export-driven Japanese corporates that tend to benefit from a weaker yen but can see margins compressed when the currency strengthens.

Its currency-hedged share classes help investors stay exposed to corporate fundamentals while reducing the impact of yen volatility on portfolio returns.

For investors seeking directional exposure to the yen, whether defensive or opportunistic, WisdomTree’s JPY exchange traded product suite provides tools for:

These instruments allow investors to navigate currency volatility proactively rather than simply absorb it.

For years, the yen carry trade has quietly underpinned global liquidity. As the BoJ prepares to tighten further, that support is fading, and the pace of the fade will set the tone for global markets.

Either way, investors who recognise the timing dynamics and position early will be better placed to separate signal from noise as global markets transition into a more volatile, opportunity-rich phase.

1 Statistical release: BIS international banking statistics and global liquidity indicators at end-March 2025

2 Interest Rate : Ministry of Finance. 02 December 2025.

3 BIS Bulleting No 90. The market turbulence and carry trade unwind of August 2024.

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).