QGRW LN

WisdomTree US Quality Growth UCITS ETF - USD Acc

Published 12 July 2024

Director, Quantitative Research

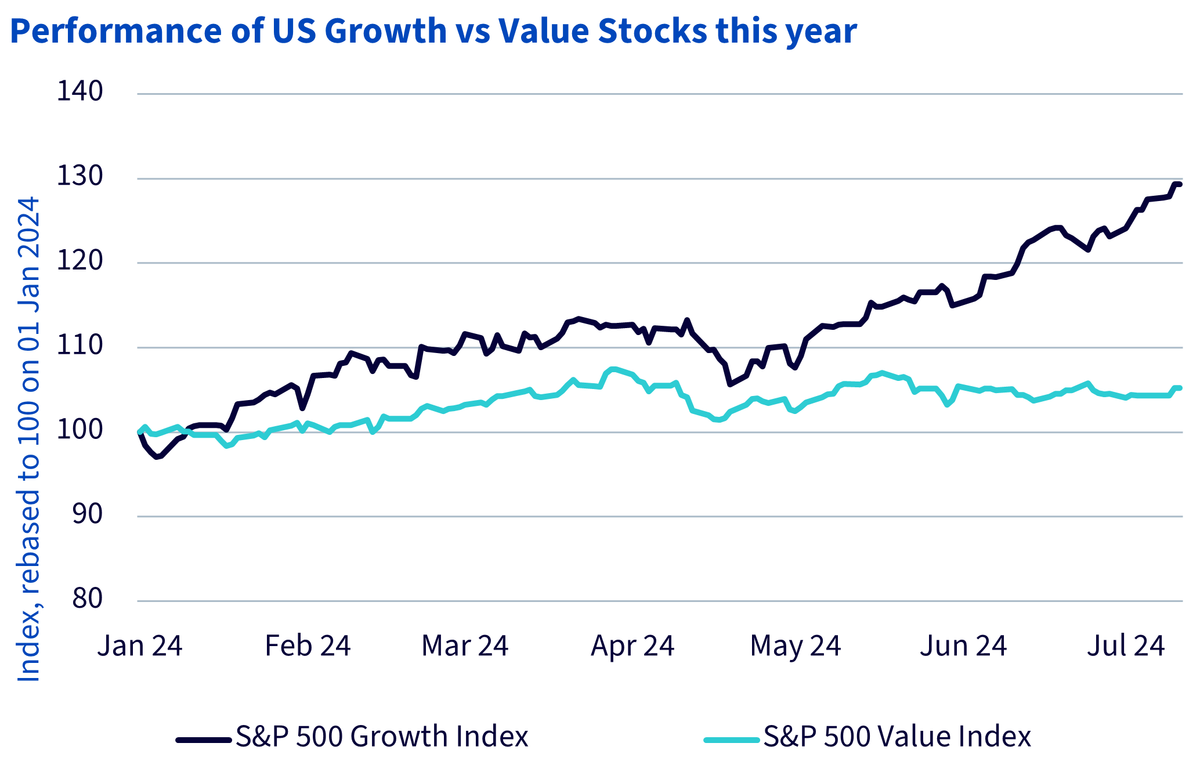

As US stocks continue to reach new highs this year, growth is clearly in the lead leaving value stocks trailing far behind. This is despite rate cuts getting pushed further out. This blog outlines the three key reasons for this outperformance and highlights a smart way for investors to access the opportunity in US growth stocks.

Source: Bloomberg, data as of 11 July 2024. Historical performance is not an indication of future results and any investments may go down in value.

With artificial intelligence (AI) all the rage this year, companies that are providing the building blocks upon which the technology is being developed are in the lead. Nvidia is the obvious example that has seen its share price rise by 172% this year1. Surprisingly, it isn’t the biggest gainer in the S&P 500 Index this year. Information Technology (IT) infrastructure provider Super Micro Computer Inc is at the number one spot with gains of 217% as markets realise the need for and importance of more data storage in this ongoing AI-powered digital revolution. So far, semiconductors are clearly in the lead. But once the Federal Reserve starts cutting, we may see software companies coming to life, still a good thing for growth investing.

Macroeconomic data from the US may not be stellar, but it isn’t worrisome either. Inflation prints have steadily cooled while labour market numbers haven’t raised any alarm bells yet. In June, the US unemployment rate stood at 4.1%, marginally higher than the 4% in the preceding month. The economy added 206,000 jobs in June, slightly less than May (218,000), but still meaningfully higher than the average monthly addition of 165,000 during the pre-pandemic year of 2019. Moreover, both services and manufacturing Purchasing Managers’ Indices (PMIs), useful gauges of month-over-month economic activity, continue to be in expansionary territory2. This means that, all in all, economic data is not creating any obstacles in the rally of growth stocks.

According to FactSet’s earnings insight on the S&P 5003, analysts typically revise their earnings estimates for US companies down over the course of any given quarter. Analysts have revised down bottom-up earnings per share (EPS) estimates (an aggregation of median EPS estimates) during a quarter by 3.4% over the last five years, 3.3% over the last ten years, and 4% over the last twenty years on average. Over the course of the second quarter this year, however, earnings estimates have only been revised down by 0.5%.

Moreover, at the sector level, the biggest decrease has come for industrials (-4.7%), while some sectors like consumer discretionary (+2.9%, a sector where some of the tech names reside), have had their bottom-up EPS estimates go up.

This means that analysts remain optimistic about second quarter earnings. If indeed we see a healthy second quarter earnings season for tech names, the momentum in growth stocks could continue.

A few common measures of selecting growth stocks include trailing sales and earnings growth, future sales and earnings growth estimates, and relative valuations like price-to-earnings, price-to-sales, and price-to-book ratios.

Because earnings-based measures of growth may be undefined for loss-making growth companies, growth strategies may ignore profitability considerations in favour of metrics like price-to-sales and price-to-book as proxies for growth.

At times, growth investors become enamoured with narrower non-earnings growth measures like “eyeballs” during the internet craze of the early 2000s, or “subscriber-growth” in recent years as it relates to streaming platforms and social media companies. This can lead to an approach to growth that over-weights highly speculative, or junky, growth names.

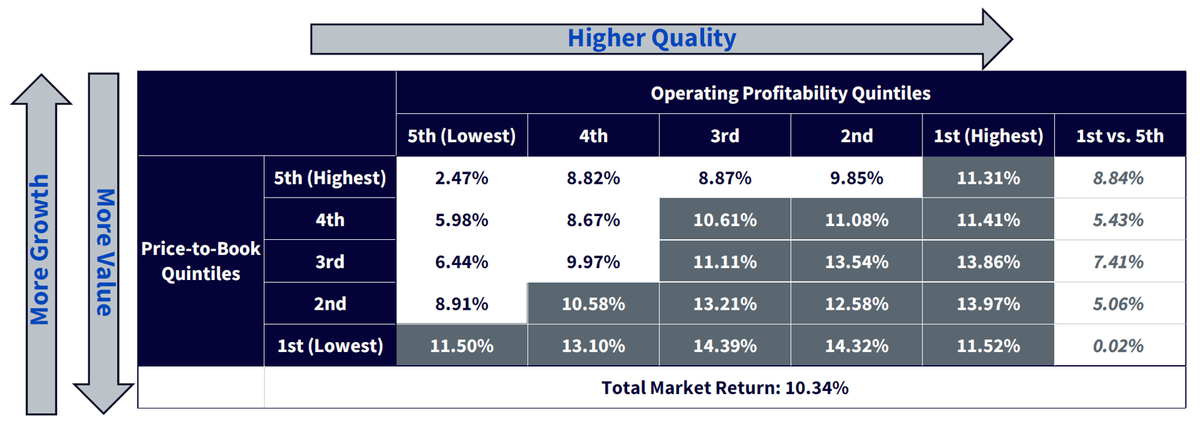

Instead, a focus on growth and profitability metrics can help avoid exposure to such speculative growth stocks. This is the approach adopted by the WisdomTree US Quality Growth UCITS Index. In the past, this focus on strong fundamentals has led to enhanced returns with Fama French factor data showing a huge difference in annualised performance over the last 6 decades between high-quality high-growth stocks and low-quality high-growth stocks (8.84%), underscoring the importance of combining the two factors for stock selection.

Source: Kenneth French Data Library, 30 Jun 1963 to 30 Dec 2023. Period based on availability of annual operating profitability returns sorted into quintiles, which begins 30 Jun 1963. Market is U.S.-listed equities grouped on the basis of operating profitability and price-to-book. Returns are annualised. Historical performance is not an indication of future performance and any investment may go down in value.

1 Bloomberg, as of 11 July 2024.

2 Trading Economics, 11 July 2024.

3 FactSet earnings insight 03 July 2024.

Director, Research

@MobeenTahirWTMobeen is a member of WisdomTree’s research team where he focuses on a wide range of asset classes to offer strategic and tactical insights to our clients on global markets and investment products. Before joining WisdomTree in December 2018, Mobeen worked at Willis Towers Watson as an investment consultant advising institutional clients as well as their in-house fund business on asset allocation and portfolio construction with his research focus being equity and multi-asset smart beta. Mobeen has a BSc (Hons) in Accounting and Financial Management from Loughborough University and an MSc in Accounting and Finance from the London School of Economics and Political Science. He is also a CFA Charterholder.

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.