WTAI LN

WisdomTree Artificial Intelligence UCITS ETF - USD Acc

Published 1 March 2024

Global Head of Research

Leading into the most recent Nvidia earnings report, we were seeing more and more calls for Nvidia’s share price to start trending down. Consider this example from the Financial Times:

Nvidia is nuts, when’s the crash?1

The results over the past year have been amazing – yes – but there is not really a precedent where a company goes from well below a $1 trillion market capitalisation to being close enough to discuss a $2 trillion market capitalisation in less than a year2.

There are two logical interpretations:

The trick to remember—the current share price is not necessarily telling us something about the past, but rather it is offering a view on the future. We saw an article indicating that Nvidia’s current valuation may be supported if the company can 10x their current revenues and do so with an operating margin of around 55% – stable – over the coming 10 years. We cannot know today if that will or will not happen, but we can note that the entire semiconductor market (meaning all sales of all semiconductors, not just AI accelerators) has been $500-600 billion in recent years, and we are saying that Nvidia, on its own, in 10-years may achieve annual revenues of $600 billion5.

The point: Continued execution on an exponential growth thesis, while not impossible, is a very high hurdle to clear.

Nvidia has been a public company for a long time – it went public in 1999 at $12 per share6. Before the extreme feelings of FOMO (fear of missing out) kick in, we must remind ourselves that the idea of using graphics processing units (GPUs) for artificial intelligence applications did not hit the mainstream until the so-called ‘AlexNet’ moment in 20127.

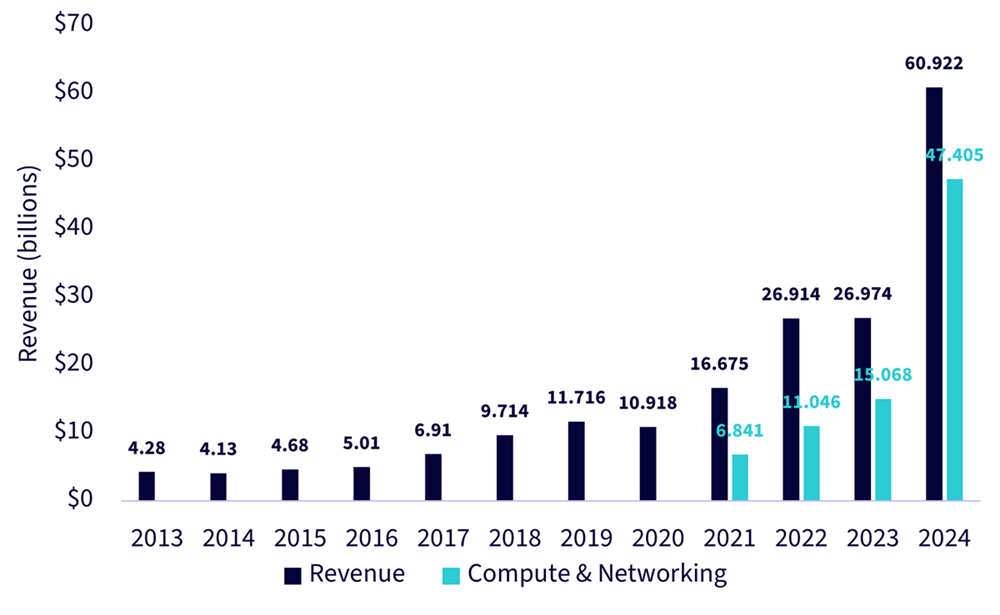

This means that we can look at Nvidia’s revenues, year-by-year, for quite a long time. We went back through the 10-K Annual Filings and built Figure 1:

Source: Nvidia’s Securities and Exchanges Commission (SEC) filings, specifically the annual 10-K reports for each of the specified years. Past performance is not indicative of future results.

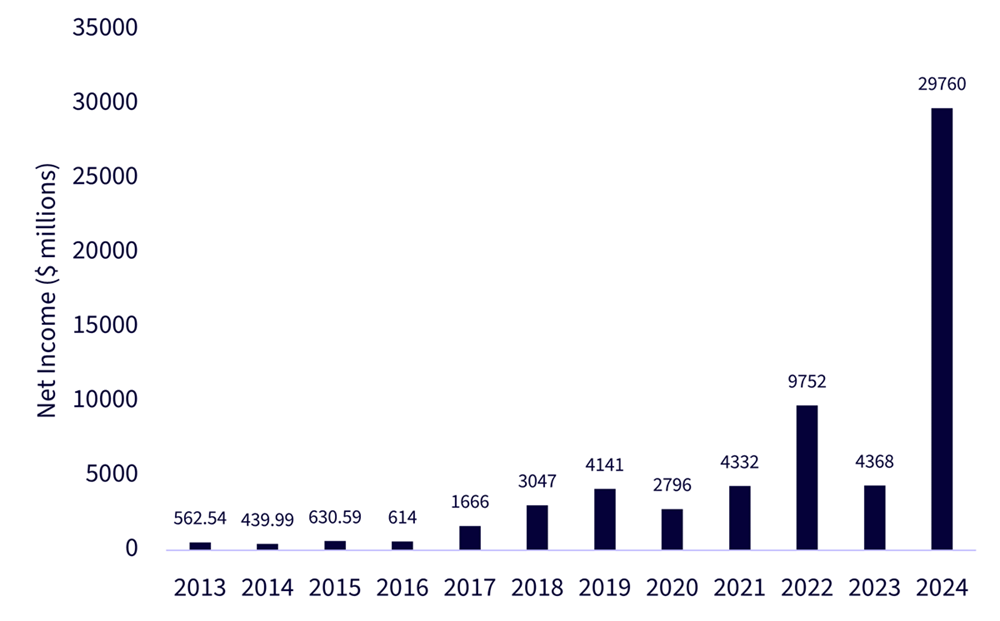

Now, revenues are not profits. However, the growth story of Nvidia’s net income is even more impressive than the revenue growth component, as we see in Figure 2:

Source: Nvidia’s Securities and Exchanges Commission (SEC) filings, specifically the annual 10-K reports for each of the specified years. Past performance is not indicative of future results.

We would go so far as to say that Nvidia’s results over the period examined in this piece are so remarkable that it would be difficult for any company to compare. When considering thematic investments, like venture capital, there can be a ‘power law’ at work, meaning that instead of all companies delivering a result close to ‘average’, we may tend to see a small number of firms delivering astronomical results and other companies tending towards terrible results. Fortunately, the astronomical results can cancel out the terrible results over time.

As we prepare for the next 10 years, we certainly would not bet against Nvidia – even if we don’t know if the company will do another 10x of its annual revenues. For strategies focused on AI, it’s an important company to be in the mix, but we would advocate recognising that Nvidia cannot experience success, and the AI megatrend will not move forward based on a single company. The semiconductor value-chain is complex, and we would advocate thinking about the relationships exemplified within it – for instance the fact that Taiwan Semiconductor Manufacturing Co. (TSMC) is fabricating Nvidia’s advanced chips. Nvidia is not, currently, making physical chips themselves.

When considering different AI strategies, we would note that it is more important to look under the hood and simply understand—what is the Nvidia exposure? What is the Magnificent 78 exposure? There are no black and white, correct and incorrect answers, but it’s important to make sure the degree of exposure to these different kinds of things is monitored over time and fits the view the investor is looking to implement.

1 Source: McCrum, Dan. “Nvidia is nuts, when’s the crash?” Financial Times. 16 February 2024.

2 Source: https://companiesmarketcap.com/nvidia/marketcap/ (Nvidia’s market cap on 18 February 2023 was roughly $532 billion, while on 22 February 2024 it was around $1.9 trillion)

3 Source: Benjamin Graham, frequently popularized by Warren Buffett, and visible in the 1987 Berkshire Hathaway letter to shareholders: https://www.berkshirehathaway.com/letters/1987.html

4 Source: https://en.wikipedia.org/wiki/ChatGPT

5 Source: McCrum, 16 February 2024.

7 Source: https://www.pinecone.io/learn/series/image-search/imagenet/

8 ‘Magnificent 7’ stocks are a group of high-performing companies in the US stock market: Alphabet (GOOGL; GOOG), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), Microsoft (MSFT), NVIDIA (NVDA), and Tesla (TSLA).

WisdomTree Artificial Intelligence UCITS ETF - USD Acc

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.