EEIE LN

WisdomTree Europe High Dividend UCITS ETF

Published 30 April 2026

Head of Research, WisdomTree Europe.

Looking back at Q1 2026, global equities entered the year carrying much of the same optimism that had closed out 2025. Inflation was easing, central banks were expected to move gradually towards policy loosening, and investors remained willing to pay for earnings resilience and the structural growth story around artificial intelligence. As the quarter unfolded, markets were shaped by a series of geopolitical shocks, first in Greenland and then in Iran, which unsettled sentiment. Energy prices moved higher, expectations for rate cuts became less certain, and volatility picked up towards the end of the period. Even so, the broader message remained relatively constructive, as earnings expectations held firm, valuations came in, and equities proved more resilient than the headlines suggested.

This instalment of the WisdomTree Quarterly Equity Factor Review examines how a more fragile macroeconomic backdrop reshaped factor leadership in the first quarter and what that may mean for portfolios as 2026 progresses.

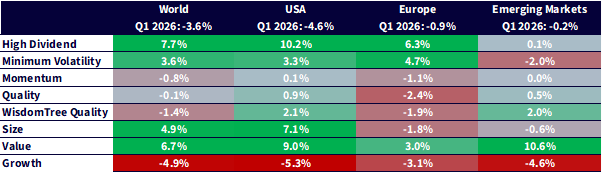

After a strong start to the quarter, equities reversed course as tensions around the Strait of Hormuz weighed on sentiment, clouding the outlook for the global economy and reviving memories of the 2022 inflation shock. Over the three months, the MSCI World Index fell 3.2% and US equities lost 4.6%.1 Europe and Emerging Markets proved more resilient, declining just 0.9% and 0.6%, respectively. Europe continues to benefit from substantial fiscal support, particularly through defence and infrastructure spending, as well as a strong shareholder-return culture focused on dividends and share buybacks.

On the factor front, Q1 looked less like a regime shift and more like a continuation of recent trends, albeit with one important change in tone:

Source: WisdomTree, MSCI, Bloomberg L.P. 13 December 2025 to 31 March 2026. Calculated in US Dollars for all regions except Europe, where calculations are in EUR. Historical performance is not an indication of future performance and any investments may go down in value.

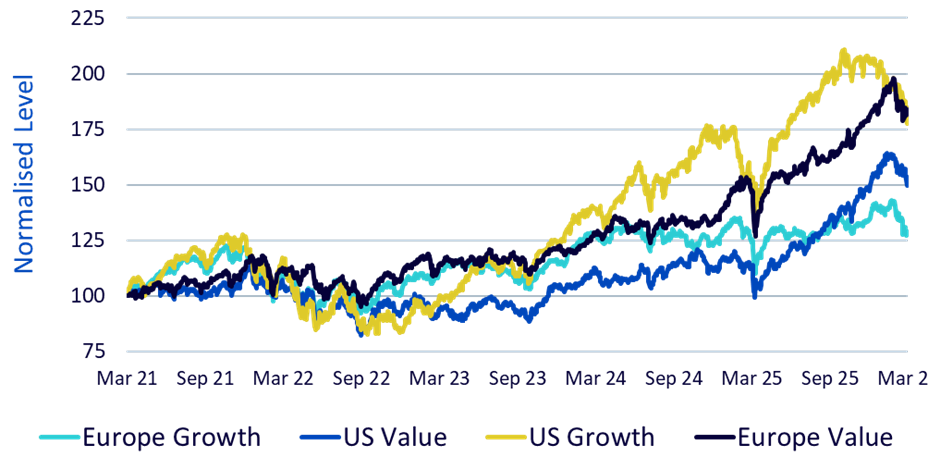

US growth stocks, led by the Magnificent Seven,2 have dominated headlines for years. This narrative has arguably overshadowed other important sources of equity performance. While it is widely recognised that US Growth has delivered an impressive 84% return over the past five years, fewer investors may realise that Europe Value has generated 83% over the same period.

More recently, momentum has clearly shifted towards Europe Value. European equities have outperformed US markets since early 2025, particularly when accounting for currency effects for euro-based investors, and Value has consistently led the factor scorecard in recent cycles.

This momentum has not emerged in isolation. Europe is increasingly supported by a domestic reflation story, driven by fiscal expansion and rising spending, particularly in defence, infrastructure and electrification. In this environment, value and dividend segments appear well-positioned, supported by stronger cash flows, greater pricing power and less reliance on falling interest rates.

Source: WisdomTree, MSCI, Bloomberg L.P. 31 March 2021 to 31 March 2026. Europe indices are in EUR, US indices are in USD. Historical performance is not an indication of future performance and any investments may go down in value.

Looking ahead, the rest of 2026 is likely to reward selectivity more than broad market exposure. The macroeconomic backdrop remains uneven, with policy paths diverging across regions and markets still sensitive to inflation, energy and growth surprises. In that environment, Europe may be well positioned for Value and High Dividend, where valuations remain more supportive, and earnings leverage to industrial, defence and infrastructure themes is stronger. In the US, where valuations and concentration remain higher, Quality may offer a more defensive way to stay invested.

While factor trends can provide useful insights, they are subject to change and may not persist. Equity markets remain sensitive to macroeconomic developments, including inflation, interest rates and geopolitical risks. Investors may experience losses and should consider the risks associated with factor investing, including periods of underperformance.

1Source: WisdomTree, MSCI, Bloomberg L.P. 13 December 2025 to 31 March 2026.

2The Magnificent Seven stocks are a group of high-performing and influential companies in the US stock market: Alphabet, Amazon, Apple, Tesla, Meta Platforms, Microsoft, and Nvidia.

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.