DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Published 10 September 2024

Equities have displayed remarkable strength in H1 2024. Performance has been supported by robust earnings and positive momentum despite the re-rating of interest rate cut expectations. Yet, it’s important to note that leadership within the stock markets remains quite narrow on a relative basis owing to earnings concentration and the AI frenzy. We are seeing signs of moderating rather than collapsing US growth, normalising labour markets and disinflation, which support the case for the Federal Reserve (Fed) to lean towards easing. Growing earnings alongside a dovish Fed are likely to provide support for the ongoing bull market, while political uncertainty should drive volatility higher.

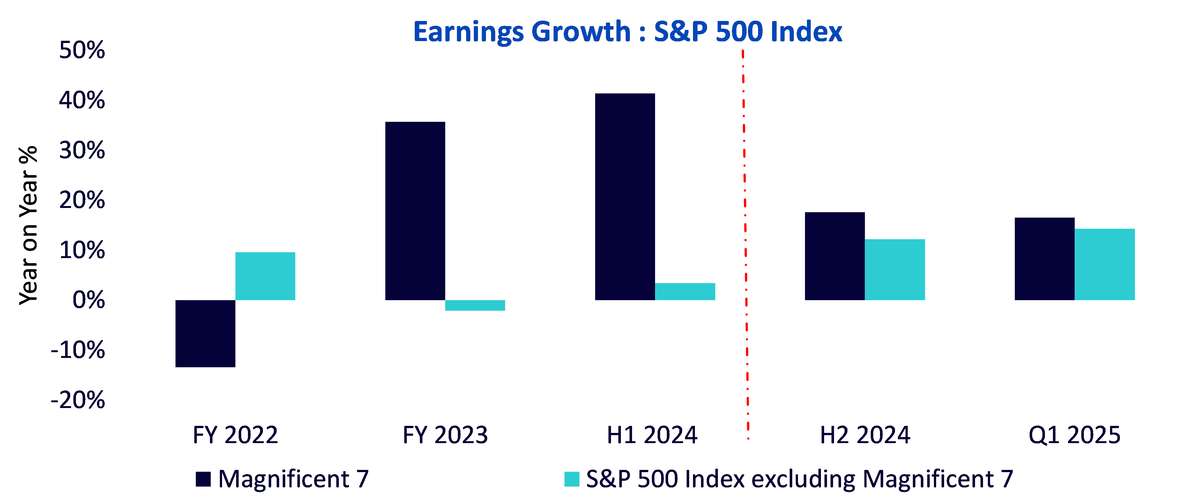

The Magnificent Seven1 has been the most crowded trade amongst investors for 16 straight months. US equities have been more concentrated than at any point since the mid-1970s. A risk of returns being so concentrated within such a small segment of the market is that when those companies fail to meet expectations, their performance suffers. Forward earnings growth looks set to expand beyond the current leaders.

Source: Factset, S&P, WisdomTree. Data as of 30/6/2024. Fiscal year (FY) is a 12-month accounting period that a business uses for financial and tax reporting purposes. It’s also known as a financial year. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

The Russell 2000 Index of small cap stocks has lagged in performance when compared to their large cap peers over the past decade. With nearly 40%2 of the Russell 2000 Index having low or no earnings over the past 12 months, the higher rate environment has added to further downside pressure on small cap stocks. Timing the reversion can be challenging and might not be necessary with small caps. Instead, adopting a barbell approach that combines large cap equity exposure with small caps is likely to provide a more balanced US equity allocation.

In sharp contrast to the US, value stocks drove strong returns across emerging markets (EMs) and have continued to outperform growth since 1990. EM equities rose by 7.5% in H1 2024, but still lagged developed market equities3. EMs have been resilient in the face of the high interest rate environment, China’s growth challenges, and a stronger dollar in 2024.

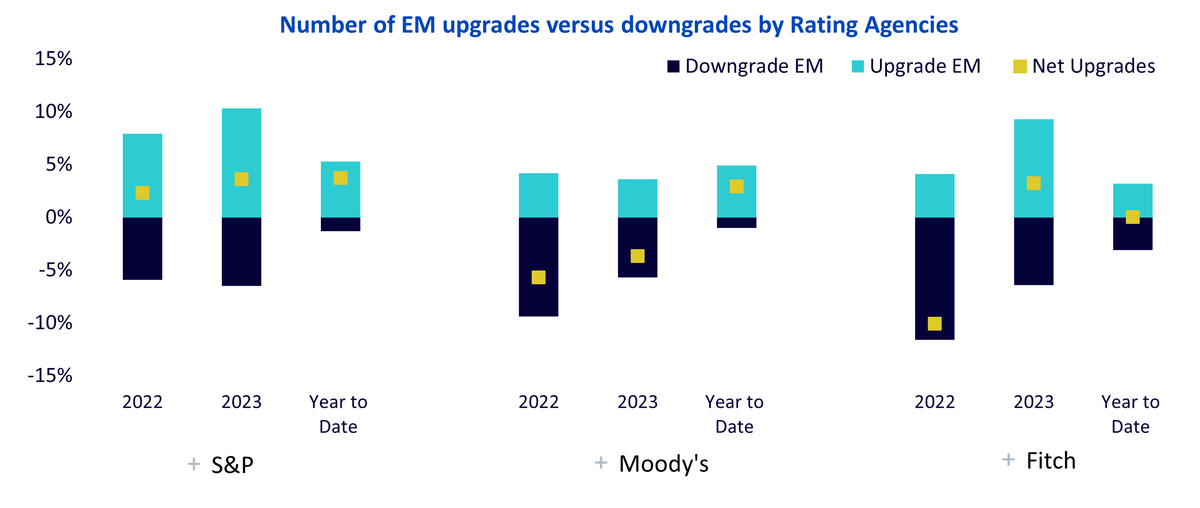

Looking ahead, we expect resilient economic growth and supply chain rebalancing alongside a monetary easing cycle by the Fed to offer a plethora of opportunities across EMs. The improvement in growth and inflation fundamentals have been supported by a wave of structural reforms in Brazil, Indonesia, India, the United Arab Emirates, and Saudi Arabia. This has driven a wave of upgrades in EM sovereign credit ratings over the past two years. This remains key for EMs, as the combination of improving sovereign credit ratings alongside positive outlooks will have a meaningful impact on lowering their cost of debt over the medium term.

Source: S&P Global, Moody’s, Fitch, Bloomberg. Data as of 30/6/2024. Historical performance is not an indication of future performance, and any investments may go down in value.

Europe’s strong equity market performance has been supported by an economic recovery in Europe driven by improvements in the services sector. At face value, things look good in Europe; however, if we look beneath the surface, Europe’s share in global market capitalisation has been falling behind for many years compared to the US and EMs that have consistently outpaced Europe in terms of economic growth. This coincides with the shrinking of Europe’s economy. Europe’s share of global market capitalisation has declined from 30% in 2000 to just 14% as of Q3 2024. High fragmentation across the continent alongside lower liquidity and different sets of national rules have also played a role. Industry-specific drivers such as the low share of technology firms across Europe also resulted in its dwindling share of total market capitalisation.

The volatile political landscape wreaked havoc on European equities in Q2 2024. It has since stabilised, but not fully recovered. Europe is a very global market from a revenue perspective, deriving more than half of its revenue (56%) outside Europe4. EMs are the most important region for European companies, accounting for 31% of the market’s aggregate revenue, followed by North America at 22%3. Amid the weaker backdrop in China, Europe faces a higher downside risk to the growth outlook in H2 2024.

In addition, under the scenario of a Trump re-election, renewed trade frictions could have markedly negative effects on the eurozone, primarily via heightened trade policy uncertainty. This is likely to strengthen the case for European Central Bank (ECB) rate cuts in 2025. We continue to expect the ECB to cut rates twice in H2 2024, with the first cut in September. ECB cuts should support investment activity. More importantly, rising wages and falling inflation are likely to raise the purchasing power of consumers. The European consumer contributes 17% of the total revenues for corporates.

Claiming European stocks are cheap is almost cliché at this point. Ordinary dividends (excluding special payments) are expected to reach 4% in Europe, reaching a new high of €463 billion5. In particular, we continue to favour value and small caps as core positions. The decline in interest rates could act as a catalyst for the small cap cohort, especially given their heightened sensitivity to tightening credit conditions.

Japan’s economic growth should benefit from a technical upturn in H2. CapEx is poised to remain on a firm uptrend supported by the need to address labour shortages, strengthen supply chains, and support decarbonisation. The recovery in CapEx is likely to be a potential theme supporting Japanese equities over the coming years.

The price-to-book (PBR) reform initiated by the Tokyo Stock Exchange (TSE) is likely to continue to support value sectors in Japan. Currently a high percentage of nearly 40% of companies still trade at a PBR below 1, creating further room to unlock shareholder value6. The ratio of companies that increased dividends in the last fiscal year (FY) reached the second highest since 1985 providing evidence of the PBR initiative. In addition, share buybacks announced along with fiscal year results also reached their highest levels in terms of both number and value since FY 2009. The slew of investments by foreign funds in Japanese equities can be seen as an encouraging reaction to corporate reforms.

Fund | Investment | Tenure |

|---|---|---|

Bain Capital | Upcoming investment of JPY5trn in Japan | 5 years |

Blackstone | JPY1.5trn investment in Japan | 3 years |

KKR | Investment of more than JPY1trn in Japan, same scale as the investment since | 10 years |

CVC | Establishment of Asia Fund including Japan of US$6.8bn, 50% larger than previous | |

Carlyle | New JPY430bn fund specialising in Japanese companies. Carlyle will increase the |

Source: Nikkei Shimbun, WisdomTree. Data as of 30 June 2024.

A gradual yen appreciation would support recovery in real wages and revival of household purchasing power. Fundamentally, large cap Japanese export stocks remain in pole position. The current foreign exchange assumption is a conservative JPY144 per dollar, expecting a stronger yen. The yen’s fall in April to June 2024 (average of JPY156 per dollar) served as a reserve. The yen would need to average JPY140 per dollar over the last three quarters of the fiscal year to align with the corporate assumption for FY24. Given the recent trajectory of the yen, we don’t expect companies to have to lower their guidance.

Equity markets posted a strong first-half performance in 2024. Continued global earnings growth should lend a positive tailwind for a continuation of the rally. Yet global equity markets are not only concentrated by name, but also by sector and factor, opening up a plethora of opportunities. The most attractive risk/reward prospects appear to be offered by overlooked areas of the market – small caps, dividend, and value stocks. From here on, we expect the US election cycle to trigger volatility as investors assess and discount the various options before them. China is up against some acute challenges, creating further opportunities across other EMs.

The full outlook can be viewed here.

1 Magnificent Seven is a group of mega cap stocks: Apple, Alphabet, Microsoft, Amazon.com, Meta Platforms, Tesla and Nvidia.

2 Bloomberg, July 2024.

3 Bloomberg, MSCI Emerging Markets Index from 31 December 2023 to 30 June 2024.

4 Factset, as of 30 June 2024.

5 S&P Global, as of 31 May 2024.

6 FactSet, WisdomTree, as of 30 June 2024.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.