Diversifying your portfolio with gold

Published 6 September 2023

Diversification is an investment strategy that consists of mixing various investments within a portfolio to reduce risk: basically ‘not putting all your eggs in one basket’ for investors. The lower the correlation between the assets in the portfolio, the greater the benefits of diversification.

Gold has a low correlation with traditional assets

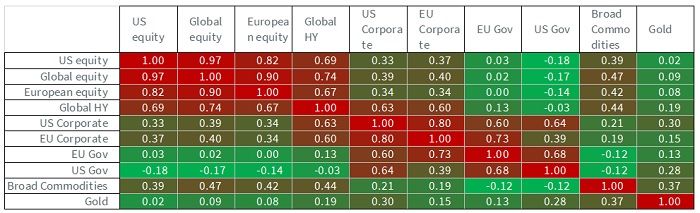

As shown in Figure 1, gold has a low correlation with stocks and bonds. While gold is technically a commodity, it behaves very differently to most cyclical commodities. The drivers of gold price (such as inflation, bond yields, exchange rates and market sentiment) make the metal appear more like a currency than a regular commodity. So, even though gold futures are part of a broad commodity allocation, they have a relatively low correlation with the rest of the commodity complex (0.37) and so they can also be considered as a separate line item for further diversification.

Figure 1: Correlation matrix

Gold has strong defensive traits

Gold prices tend to rise in financial crises, economic downturns, and geopolitical shocks. Equities are quite the opposite: they tend to falter in financial crises, early phases of economic downturns, and are sometimes vulnerable to geopolitical shocks.

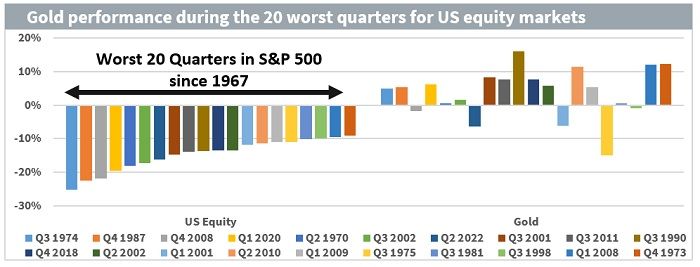

Gold has, historically, performed well during equity market crises. Gold has returned positive performance in 15 out of the 20 worst quarters of performance for the S&P 500. Of the remaining five quarters, gold has outperformed the S&P in four quarters. The only quarter when gold fell harder than equities - Q3 1975 - came a year after abnormally large gains in gold prices (in 1974 gold prices rose 72% and then corrected downward 24% in 1975).

Figure 2: Gold performance during the 20 worst quarters for US equity markets

Gold performs well in deep recessions and strong expansions

Gold has, historically, performed well in times of inflation. Given that inflation is often elevated in times of strong economic growth, gold is not just a defensive asset. In fact, no other asset behaves like gold: the metal performs strongly in both economic downturns and upturns. This uniqueness in behaviour once again makes it a strong candidate for diversification.

As a point of illustration, we look at the performance of assets in different points in the economic cycle. Composite Leading Indicators (CLIs), provide signals of turning points in the economic cycle1. Figure 3 below shows various phases of the economic cycle derived from CLIs.

Figure 3: Composite Leading Indicator of economic conditions

Source: WisdomTree, OECD, Bloomberg. OECD calculates the index so that the long-term average is 100. The index is designed to correlate and provide timely leads on economic output gaps (economic performance relative to potential). Deep recession equates to the lowest quartile of data. Strong expansion relates to highest quartile of data. June 1989 to June 2023. Historical performance is not an indication of future performance and any investments may go down in value.

Using the CLI from Figure 3, we look at the performance of assets in Figure 4. Gold performs better than any other asset in deep recessions. It also strongly outperforms defensive assets in times of economic expansion. It even outperforms bonds (government and corporate) in times of mild recession.

Figure 4: Asset performance in different phases of the economic cycle, with gold and silver

Source: WisdomTree, Bloomberg, Organisation for Economic Cooperation and Development. Period June 1989 to June 2023. Asset descriptions at the end. Historical performance is not an indication of future performance and any investments may go down in value.

How much gold should an investor add to a portfolio to benefit from diversification?

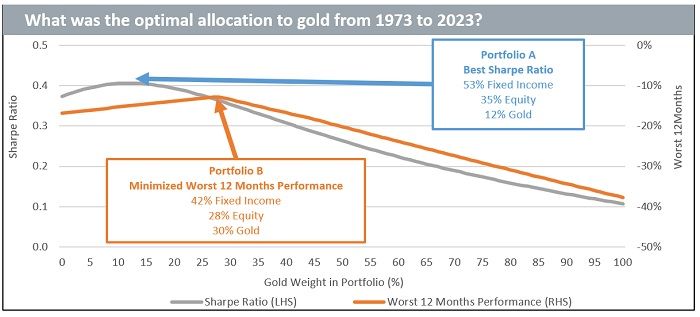

By adding gold to a traditional portfolio of stocks and bonds, it’s easy to see that the Sharpe ratio (the return of portfolio relative to its risk) can be improved. In Figure 5, we start with an illustrative portfolio of 60% bonds and 40% equities, with no gold allocation (at 0 on the x-axis). That has a Sharpe ratio of 0.37 (grey line, left axis). As we increase the allocation to gold (moving along the x-axis) and keep the rest of the example portfolio weights in a 60/40 bond-equity allocation, the Sharpe ratio starts to rise. It peaks at a gold allocation of 12%2, with a Sharpe ratio of 0.41 and then declines with higher gold allocations. Gold can be volatile asset and, therefore, detracts from the Sharpe ratio after a certain point. This is a lot more than what we believe most investors currently allocate to gold.

Another way of thinking about optimisation is to consider drawdowns: what is the worst expected performance in a 12-month period? The orange line on the right axis shows that allocations of gold up to 30%3 reduce the worst expected performance in a 12-month period. This is a lot more than what most investors currently allocate to gold.

Figure 5: What was the optimal allocation to gold from 1973 – 2023?

Source: WisdomTree, Bloomberg. Period January 1973 to June 2023. Calculations are based on monthly returns in USD. The portfolio is rebalanced semi annually. Equities are proxied by the MSCI World Gross Total return Index and Fixed Income is proxied by the Bloomberg Barclays US Treasury Total Return Index. You cannot invest directly in an index. Above numbers include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusions

Gold behaves very differently to stocks and bonds and, thus, has a low correlation with both assets. That’s why it is a great portfolio diversifier. Gold as a defensive asset provides a hedge against financial and economic turbulence. But it also performs very well in times of inflation, which is often a by-product of strong economic growth. Gold is unique in this manner and, therefore, very difficult to replace with other assets. One of the benefits of diversification is to reduce risk, as we can see in the Figures above.

Implementation solutions

WisdomTree is a market leader in gold exchange-traded products (ETPs). Since creating Europe’s first gold ETP almost two decades ago, we have continued to build our suite of gold products, offering clients best in-class features and price competitive solutions. WisdomTree Core Physical Gold (WGLD), for example, is fully backed by London Bullion Market Association (LBMA) gold bars produced after January 2022, which are bars conforming to the latest Responsible Sourcing Guidance offered by the LBMA and has a management fee of only 12 basis points. WisdomTree offers currency-hedged4, short5 and leveraged exposures6 to the metal.

Assets descriptions

Related blogs

+ Gold is expensive. Don't waste it!

+ Two ways to supercharge the diversification powers of broad commodities.

+ Looking for a free lunch? Consider putting carbon in your portfolio.

2 Source Remainder of portfolio maintains a 60/40 split, that is, 53% bonds and 35% equity.

3 Source Remainder of portfolio maintains a 60/40 split, that is, 42% bonds and 28% equity.

4 Source WisdomTree Physical Gold - EUR Daily Hedged (GBSE) and WisdomTree Physical Gold - GBP Daily Hedged (GBSP) which are physically-backed by LBMA gold.

5 Source WisdomTree Gold 1x Daily Short (SBUL) and WisdomTree Gold 3x Daily Short (3GOS), which are synthetic exposures.

6 Source WisdomTree Gold 2x Daily Leveraged (LBUL) and WisdomTree Gold 3x Daily Leveraged (3GOL), which are synthetic exposures.

Categories

About the contributor

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.