WCLD

Cloud Computing Fund

Published June 5, 2026

U.S. Head of Research

Director, Model Portfolios

WisdomTree’s Strategic Model Portfolios are intended to be exactly what they are called: strategic. In a typical year, the Model Portfolio Investment Committee (MPIC) initiates between four to six trades in the models, and in some years even fewer, because rebalancing is driven strictly by market conditions rather than by any preset calendar cadence. The objective is to adjust the portfolios as market conditions evolve to the point where they change the risk-reward profile of key factors, styles or regions.

The first four months of 2026 have presented such a shift.

The MPIC made several trades at the end of April in the models’ equity, fixed income, and thematic exposures, which we will highlight below.

Increasing U.S. Large Cap Growth

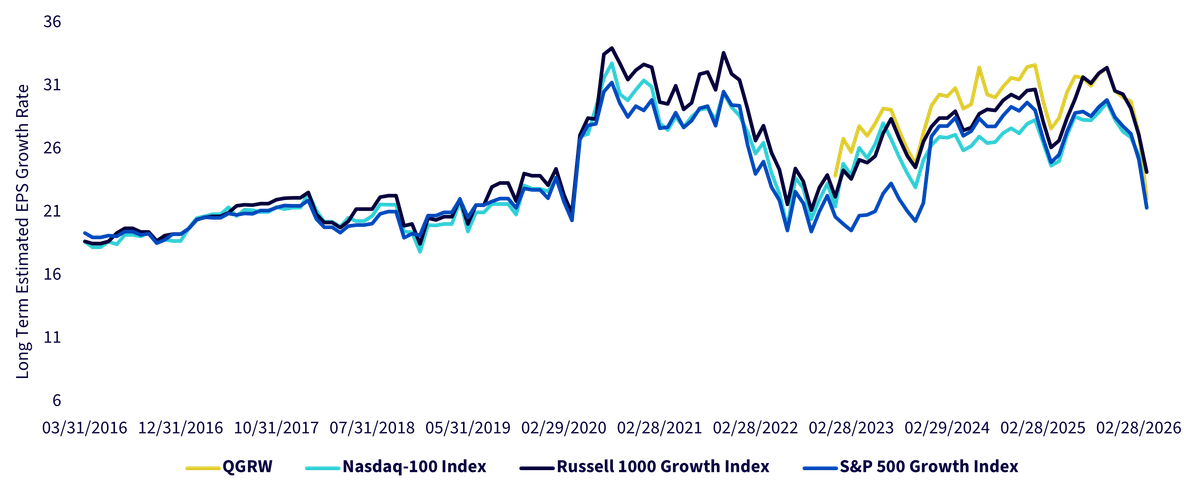

After outperforming from the 2022 lows, U.S. growth stocks experienced a sharp selloff during the geopolitical volatility earlier this year, particularly in technology and AI related sectors. In our view, the market reaction became disconnected from earnings fundamentals. Over recent weeks, many large cap growth companies have delivered strong results, reinforcing that secular demand trends remain intact despite macro uncertainty.

The combination of falling prices despite improving earnings had a significant impact on valuations. It has been rare to see U.S. large cap growth stocks trading at relatively attractive valuations in recent years, but the recent reset has done exactly that. At the end of March, the S&P 500 Growth Index was trading at the lowest multiple since October 2023. This reading was just the 36th percentile of its 10-year history, at a time when many other indexes and styles were well above their respective historical averages. Along the same vein, the WisdomTree US Quality Growth Fund (QGRW) was trading at the cheapest valuation since its inception in 2022 - despite having generated a total return of over 150% over that time.

Figure 1: Historical Valuations

Source: WisdomTree, as of 3/31/26.

On top of depressed valuation was weak investor sentiment and positioning. The rolling 90-day flows for the largest Nasdaq 100 ETF went negative for the first time in several years in Q1. Institutionally, non-dealer positioning in Nasdaq futures and options contracts was among the lightest in the last 4 years. Positioning has become an increasingly important driver of forward returns as trading ease and velocity has risen, and we believe that these data points represent contrarian opportunities for reversion.

High quality stocks like these do not go on sale often, and there are even fewer times when you can say the largest names in the stock market are under-owned. As such, the Model Portfolio IC decided to take advantage of this opportunity by selectively upgrading growth stocks– exactly like we did with WisdomTree Value Fund (WTV) recently.

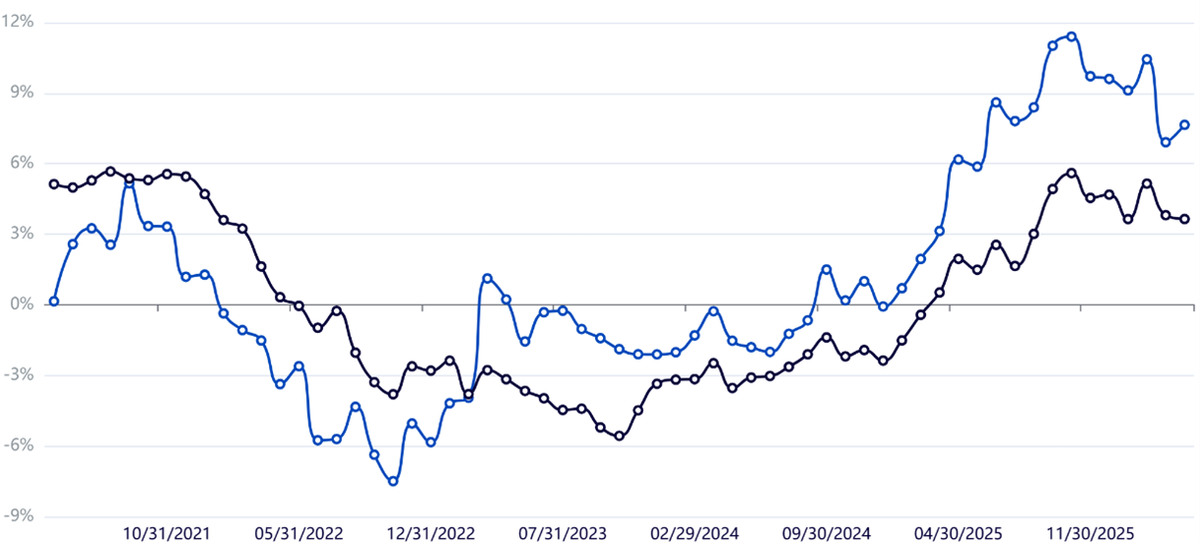

Increasing Emerging Market Local Debt

Within our Fixed Income Model Portfolio, we are increasing diversification and seeking more attractive income opportunities by shifting part of our U.S. core bond exposure into emerging market local debt.

We also believe the relative opportunity set within fixed income has shifted. U.S. credit spreads remain historically tight, limiting the amount of incremental compensation investors receive for taking additional credit risk domestically. In contrast, many emerging market economies continue to exhibit improving inflation dynamics, disciplined monetary policy and relatively solid fundamentals while offering materially higher yields.

Figure 2: Rolling 3-Year Total Returns: WisdomTree Emerging Market Local Debt (Blue) vs. Bloomberg U.S. Aggregate Index (Black)

Source: WisdomTree, for the period4/30/21–4/30/26. You cannot directly invest in an index. Past performance is not indicative of future results.

After rebounding earlier this year, the U.S. dollar appears increasingly vulnerable to moderation over the medium term. We saw in 2025 how quickly dollar weakness can create meaningful tailwinds for non-U.S. assets, particularly emerging market currencies. While currency moves are never linear, we believe the current environment provides an opportunity to add non-dollar exposure to the portfolios.

Importantly, this helps broaden the portfolio’s sources of income and return while reducing reliance on a single rate or currency regime.

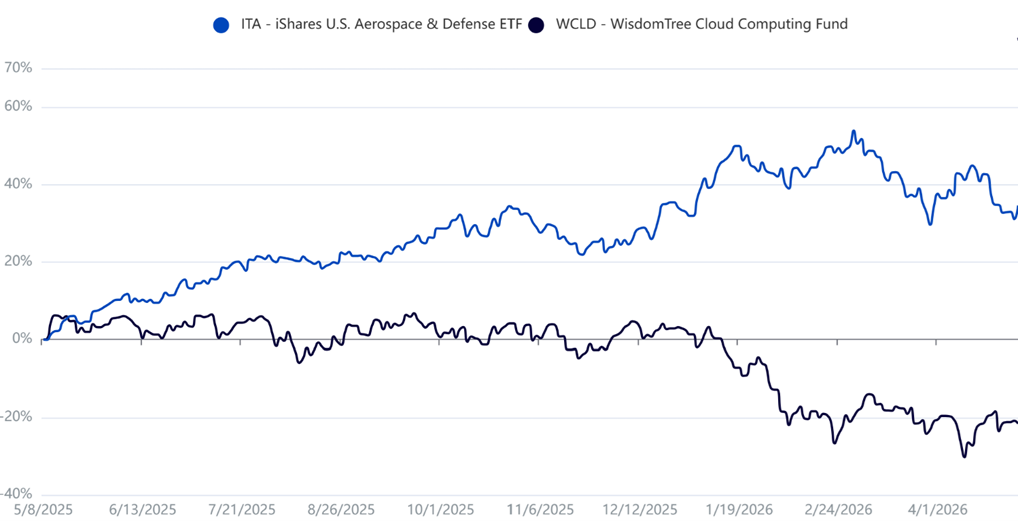

Reducing U.S. Defense Exposure and Increasing Cloud Computing Exposure

Our final portfolio adjustment reflects a disciplined rebalancing of relative winners and losers.

Defense stocks performed exceptionally well in recent quarters, especially during the escalation of conflict with Iran as investors priced in rising geopolitical risk and increased military spending expectations. While we continue to recognize the long-term importance of the sector, much of that positive narrative is now reflected in valuations. Performance has begun to consolidate following the sharp rally earlier this year.

At the same time, cloud computing and broad software stocks have undergone a meaningful correction. Concerns surrounding AI spending efficiency and near-term monetization pressured the sector despite continued strength in enterprise demand and digital infrastructure spending. While threats from AI are legitimate, we believe the selloff may have moved beyond justification.

Figure 3: 1-Year Performance

Source: WisdomTree, for the period 4/30/25 – 4/30/2026. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: ITA, WCLD.

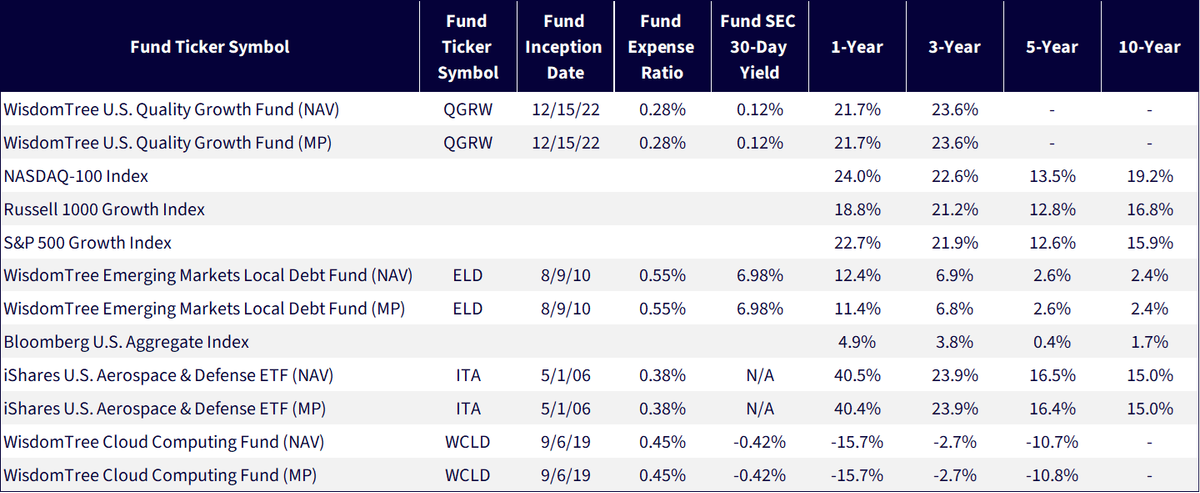

Figure 4: Standardized Performance

Source: WisdomTree, Morningstar, as of 3/31/26. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: QGRW, QQQ, IWF, IVW, ELD, ITA, WCLD.

To be clear, we are not saying that the risks of investing in defense stocks are comparable to the risks of investing in cloud computing stocks. However, in our view, this dislocation has created an attractive contrarian opportunity. As a result, in the Geopolitically Risk Aware Model Portfolio we have taken profits from defense holdings and reallocated into cloud computing stocks.

Conclusion

These portfolio changes are rooted in a consistent framework: focus on areas where fundamentals are improving, valuations are more compelling and market positioning creates asymmetrical opportunity. As a result, we believe the combination of renewed growth leadership, broader fixed income diversification and selective exposure to dislocated technology themes positions portfolios for the next phase of the market cycle.

There are risks associated with investing, including possible loss of principal.

WTV: Value stocks, as a group, may be out of favor with the market and underperform growth stocks or the overall equity market.

Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended.

WCLD: The Fund invests in cloud computing companies, which are heavily dependent on the Internet and utilizing a distributed network of servers over the Internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress, and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the Internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties and the Index may not perform as intended.

ELD: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions.

Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. In addition, when interest rates fall income may decline. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

QGRW: Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For financial advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy.

For retail investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. The performance of your account may differ from the performance shown for a variety of reasons, including but not limited to: your investment advisor, and not WisdomTree, is responsible for implementing trades in the accounts; differences in market conditions; client-imposed investment restrictions; the timing of client investments and withdrawals; fees payable; and/or other factors. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

U.S. Head of Research

Bradley Krom joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.

Director, Model Portfolios

Joe Tenaglia joined WisdomTree as Asset Allocation Strategist in 2016. He is responsible for building and managing WisdomTree’s CIO-managed and custom model portfolios. In this role he focuses on asset allocation, security selection, and portfolio construction for the firm’s open architecture models, with objectives ranging from strategic to tactical. Joe sits on WisdomTree’s Model Portfolio Investment Committee, which oversees the firm’s ETF models and helps shape and communicate WisdomTree’s thoughts on the markets. Prior to joining WisdomTree, he held roles at Emerging Global Advisors (acquired by Columbia Threadneedle) and BNY Mellon. Joe received his B.S. in Finance and Marketing from Boston College. He is a holder of both the Chartered Financial Analyst designation and Chartered Market Technician designation.