WTMF

Managed Futures Strategy Fund

Published December 8, 2025

Director, Quantitative Research

Global Head of Research

Periods of heightened macro uncertainty often remind investors of the value of diversification that truly behaves differently. WisdomTree's Managed Futures Strategy Fund (WTMF) seeks to capture that principle in practice—systematically identifying price trends across commodities, equities, currencies, rates and even digital assets, then taking long or short positions accordingly. Rather than relying on static diversification, it adapts as market dynamics shift, targeting positive returns regardless of direction. In 2025, this flexibility has paid off. With strong bullish signals across energy, precious metals, equities and cryptocurrencies, and tactical shorts in grains and select softs, the strategy has capitalized on dispersion rather than suffered from it.

The result: performance that stands apart from traditional 60/40 portfolios and even many alternative peers—delivering low correlation, smoother return profiles and a timely reminder that in a world of crowded trades, trend-following remains one of the few true diversifiers left.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/12/25, with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The Fund's strategy changed effective June 4, 2021. Prior to June 4, 2021, Fund performance reflected the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree Managed Futures Index. Since June 4, 2021, the Fund has followed an actively managed strategy that seeks to achieve positive total returns in rising or falling markets that are not directly correlated to broad market equity or fixed income returns. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Interpreting the Attribution: How the Strategy Works across Asset Classes

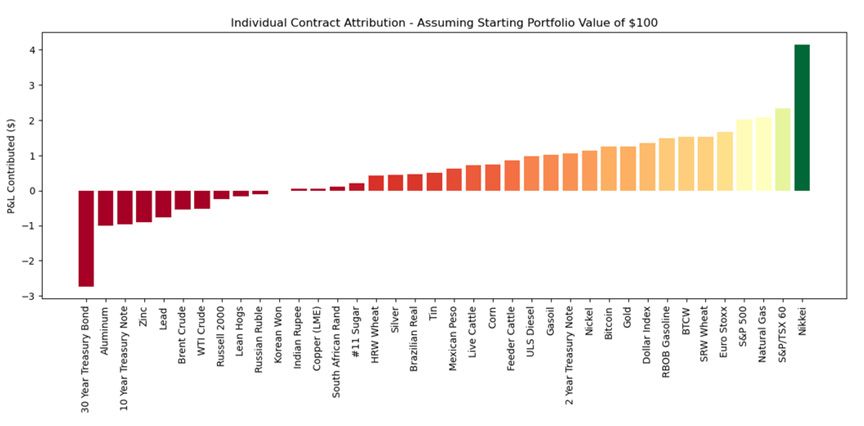

The equity component was a clear driver of positive returns—visible on the far right of figure 3, where indexes like the S&P 500 and Nikkei stand out. This reflects how the strategy increases exposure during strong, steady markets to capture upside when risk and momentum indicators are favorable. When conditions begin to deteriorate, exposure is trimmed or fully hedged, preserving capital during downturns. This dynamic approach—alternating between offense and defense—helps smooth returns and limit drawdowns without employing leverage.

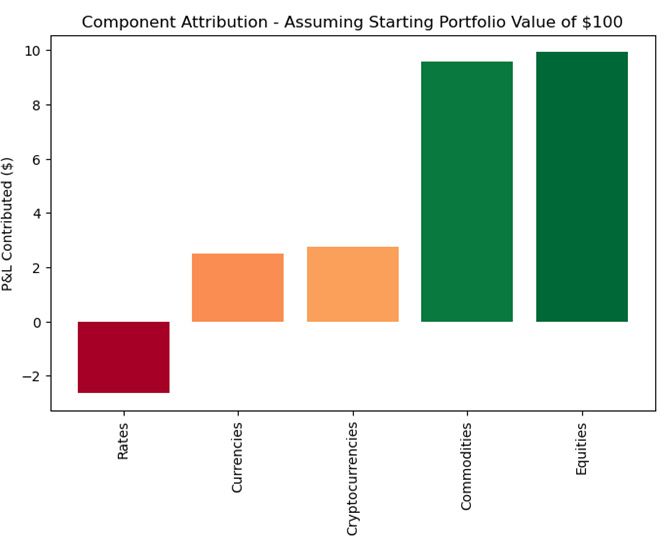

Commodities also delivered strong performance (figure 2), with the majority of individual contracts contributing positively to returns—just behind equities in terms of total return contribution. As shown in figure 3, gains from natural gas, gasoline and several agricultural and industrial contracts outweighed small losses in a few metals like aluminum and zinc. This broad-based strength across the commodity complex highlights how the strategy effectively captured persistent price trends while maintaining balanced exposure across sectors.

Currency exposures, such as positions in the Mexican peso and Brazilian real, contributed modestly, reflecting how the model follows momentum in the U.S. dollar. Strength in the dollar translates into long U.S. Dollar Index futures, while signs of weakness favor a tilt toward emerging-market currencies.

The Bitcoin sleeve contributed positively as well, benefiting from sustained upward momentum. The position scales between full, partial and no exposure, depending on the strength of the signal—participating in major uptrends while sidestepping abrupt corrections.

Attribution for long duration Treasuries was negative for the period, with a majority of the hit borne by longer-dated 30-Year Treasuries. The pivot to 2-Year Treasuries during positive correlation periods between equities and Treasuries helped offset some of these negative returns and contributed positively amid the higher-rate environment.

Figure 2: Attribution of the Current Strategy (Asset Class Level)

Sources: WisdomTree, FactSet, for period from 6/4/21 to 10/31/25. Past performance is not indicative of future results. The Fund's strategy changed effective June 4, 2021. Prior to June 4, 2021, Fund performance reflected the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree Managed Futures Index. Since June 4, 2021, the Fund has followed an actively managed strategy that seeks to achieve positive total returns in rising or falling markets that are not directly correlated to broad market equity or fixed income returns.

Figure 3: Attribution of the Current Strategy (Individual Contracts Level)

Sources: WisdomTree, FactSet, for period from 6/4/21 to 10/31/25. Past performance is not indicative of future results. The Fund's strategy changed effective June 4, 2021. Prior to June 4, 2021, Fund performance reflected the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree Managed Futures Index. Since June 4, 2021, the Fund has followed an actively managed strategy that seeks to achieve positive total returns in rising or falling markets that are not directly correlated to broad market equity or fixed income returns.

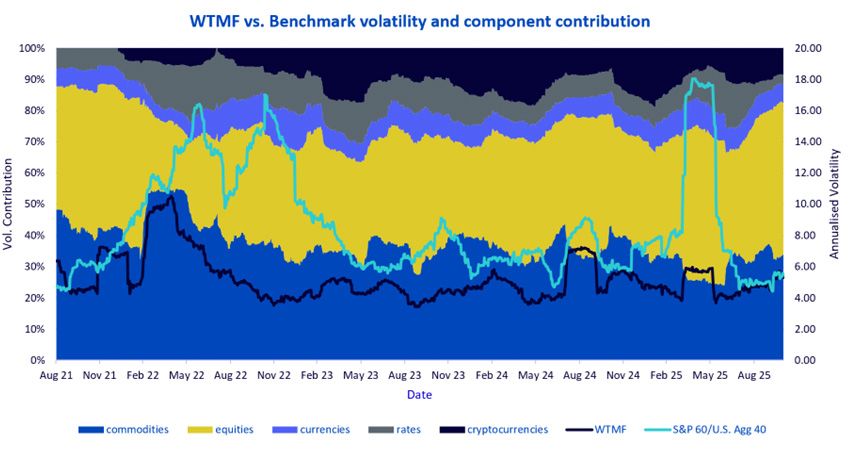

WTMF's results reflect the payoff of a disciplined, diversified and adaptive process. Over the past three years, the Fund has delivered strong risk-adjusted returns with meaningfully lower volatility than a traditional 60/40 benchmark. Figure 4 shows how sources of risk—commodities, equities, rates, currencies and crypto—shift dynamically through time, keeping portfolio volatility controlled even in turbulent periods. This ability to modulate exposure across uncorrelated assets allows WTMF to stay engaged in trending markets while cutting risk when conditions deteriorate. The outcome: smoother performance, balanced sources of return and a volatility profile that reinforces the power of a systematic, non-levered approach.

Sources: WisdomTree, FactSet, for period from 6/4/21 to 10/31/25. Volatility is three-month rolling, annualized. Past performance is not indicative of future results.

There are risks associated with investing, including possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors that contribute to the Fund's performance, as well as its correlation (or non-correlation) to other asset classes. These factors include the use of long and short positions in commodity futures contracts, currency forward contracts, swaps and other derivatives. Derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks and historically have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue.

The Fund should not be used as a proxy for taking long-only (or short-only) positions in commodities or currencies. The Fund could lose significant value during periods when long-only indexes rise (or short-only indexes decline). The Fund's investment objective is based on historic price trends. There can be no assurance that such trends will be reflected in future market movements.

The Fund generally does not make intra-month adjustments and therefore is subject to substantial losses if the market moves against the Fund's established positions on an intra-month basis. In markets without sustained price trends or markets that quickly reverse or “whipsaw," the Fund may suffer significant losses.

The Fund is actively managed; thus, the ability of the Fund to achieve its objectives will depend on the effectiveness of the portfolio manager.

Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

Managed Futures Strategy Fund

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.