Stock Market Implications of Bonds’ Margin Call

Published September 9, 2022

Head of Equity Strategy

The bond market has had a rough two years.

The Bloomberg U.S. Aggregate Bond index started slipping, albeit gently, in August 2020. Last year the grind continued, with the index declining by a not frightful but annoying 1.7%.

Then came 2022.

With the index down by more than 10% this year, bond investors are bracing for a portent that has been rare, at least for as long as I’ve been in this business: three quarters in a row of red ink in the fixed income page of the brokerage statement. It may or may not come to pass—bonds were down 0.06% in July and August, so a little rally in bonds in September would end the streak.

Nevertheless, 2022 has been weird. In “normal” times, bonds would be expected to thrive in a weakening economy. But this year, that old truism has been thrown out the window.

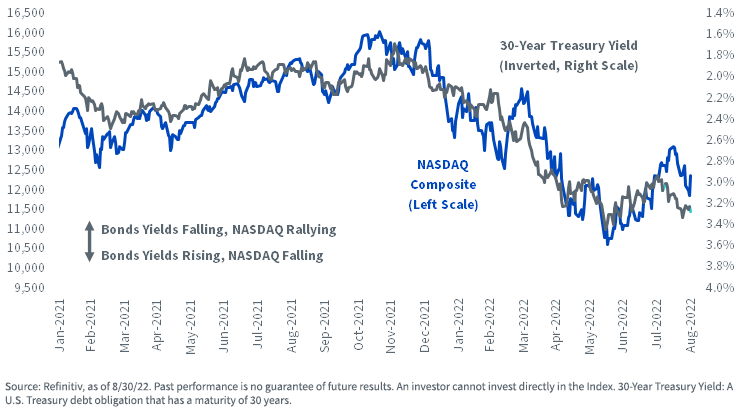

The NASDAQ is taking its cue from the long bond yield. It’s down 23%, and the S&P 500 Growth index is tracking it with a 21% loss. This puts the relative haven status of the S&P 500 Value Index, which is down “only” 7%, into perspective.

Figure 1: The NASDAQ Is Tied to Bond Yields

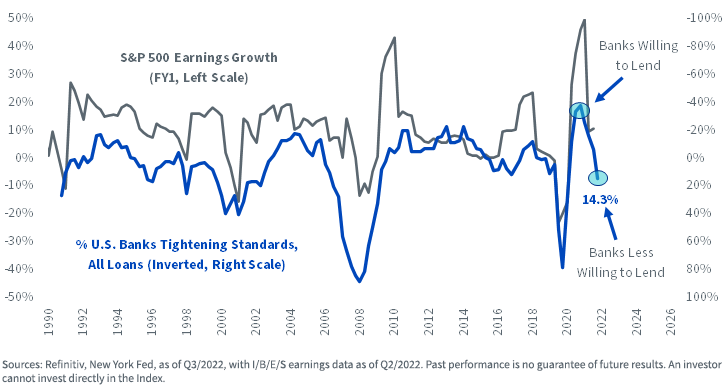

Stock market earnings look suspect. I think that is a problem for the very high beta stocks that tend to populate growth baskets.

Consider this. The New York Fed’s Q3 Senior Loan Officer Survey found that a net 14% of U.S. banks are tightening their lending standards. In figure 2, we can see three episodes over the last quarter-century in which that metric has deteriorated from net easing to a net tightening of this severity. Those episodes were in 2000, 2007 and 2020—all good times to make a prediction that earnings would decline.

Granted, I don’t know if making a comparison to the global financial crisis is warranted at this stage of the game, so take this with a grain of salt. Nevertheless, a scenario that sees S&P 500 earnings growth declining in 2023 is plausible, reasonable and possible.

Figure 2: Tightening of Bank Lending Standards Bodes Ill for S&P 500 Profits

Should that come to pass, we would have a situation where the entire yield curve may be following the Fed higher on rates, while at the same time, equity investors are finding little solace in earnings reports.

We don’t know if current relationships will hold, but it seems to me that if the bond market wants to sell off and S&P earnings want to lay an egg, then growth stocks are a problem child in 2023.

In other words, growth stocks are now the anti-diversification, pro-concentration asset class. As the bond market receives its proverbial margin call, there may come that time that every investor dreads: scanning the holdings list for something to sell.

If it’s the Bloomberg Aggregate that gives investors headaches in the coming months and years, it might just be the NASDAQ-style holdings that meet the sell button. If the bond market’s action continues to punish growth stocks, our dividend strategies may represent something of a shelter.

Unless otherwise stated, data is as of 8/30/22.

Categories

About the contributor

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.