Staking a “Claim” With Inverted Curves

Published June 26, 2024

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- The U.S. economy has not entered a recession despite the inverted yield curve, which historically predicted recessions, and this may be due to the relatively solid labor market setting.

- The monthly Employment Situation report and the initial jobless claims series are crucial indicators for the money and bond markets, as well as for the Federal Reserve (Fed).

- The current level of new jobless claims is significantly lower than the levels prior to the past four recessions and the average level of claims over a 40-year period, indicating a relatively strong labor market.

Remember when an inverted yield curve used to predict recessions? Here we are about two years removed from the Treasury yield curve moving into negative territory, and the U.S. economy has yet to move into recession territory. The economy’s resilience has certainly been a surprisingly welcome development and has left many a market participant wondering what happened. Indeed, history has shown us that the track record of inverted yield curves predicting a recession was almost foolproof. Now, I certainly don’t want to put a whammy on things, but if you’re wondering why an economic downturn has yet to occur, perhaps you don’t need to look any further than the relatively solid labor market setting.

There is no question that the monthly Employment Situation report is essentially either 1 or 1A in terms of importance, not just for the money and bond markets but for the Fed as well. Recently, inflation data has also snuck into the top category, but that’s for another blog.

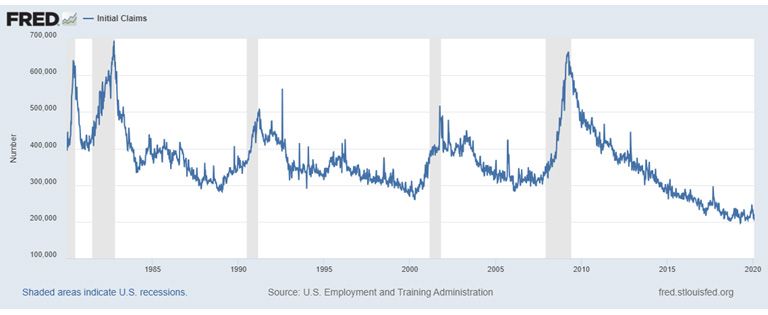

Source: St. Louis Fed, as of 6/21/24.

Another set of employment data that is rather useful to focus on is the initial jobless claims series. This report comes out weekly and offers investors and policy makers a more “real-time” look at labor market trends. In addition, it is one of the 10 leading economic indicators.

This series has captured its own fair share of headlines since the Fed began its aggressive rate hike cycle, as market participants have been looking for clues to any adverse impact this tightening episode may have had on the labor markets. Once again, in surprising fashion, the level of new weekly unemployment claims has remained historically low despite the rise in interest rates.

There have been periods in the last year or so when the level of new claimants would rise unexpectedly, but then in future reports, the number would come back down again. More recently, the weekly reading rose to a 10-month-high watermark, and needless to say, there was some chatter that this increase could finally be a sign that the labor markets may be beginning to soften up.

While perhaps that may prove to be the case, I thought it would be prudent to put the level of jobless claims into some perspective and not rush to any conclusions. In order to get a more accurate picture, I decided to go back and look at the 40-year period prior to COVID-19 for some guidance. Interestingly, this also coincides with many analyses regarding the inverted yield curve and recession relationship.

So, what does one discover about the current reading of 238,000 new jobless claims? Two very important factoids:

- It is at least 100,000 or more below the levels that existed prior to the past four recessions.

- It is 125,000 below the average level of claims for this 40-year period.

Conclusion

While the monthly inflation data might be getting “top billing” of late, investors should also remember the importance of labor market trends and their impact on Fed policy, a point Chairman Powell reiterated at the June FOMC presser. Against this backdrop, the weekly jobless claims report can serve as a useful indicator for investors to focus on, but as yet, it is not flashing any warning signals.

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.