Pre-FOMC: A Different Type of Taper

Published April 17, 2024

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- Although no rate cuts yet, the Federal Reserve is considering reducing the pace of quantitative tightening (QT).

- The Fed’s ultimate goal is to have only Treasuries on its balance sheet.

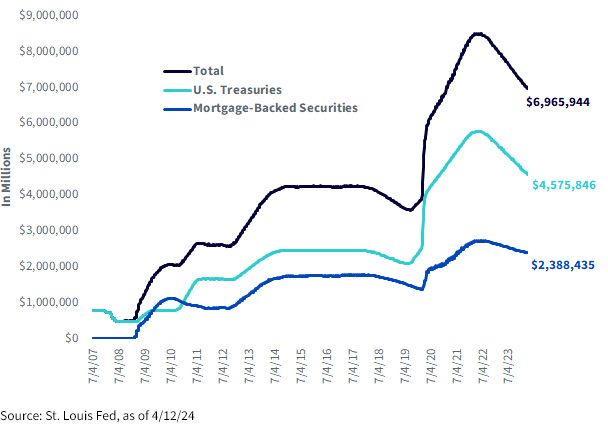

- The reduction in the Fed’s securities holdings through QT has resulted in a decrease of more than $1.5 trillion, from a peak of $8.5 trillion in May 2022 to $6.97 trillion as of the writing of this document.

Following last week’s “hotter” than expected CPI release, the sole focus for the money and bond markets was to, yet again, dial back their Fed rate cut expectations. However, there is another aspect of Fed policy decision-making that has been flying under the radar, and that involves its balance sheet. With the May 1 FOMC meeting only two weeks away, I thought it would be a good idea to discuss this part of monetary policy because, at this point, it appears as if this facet may make headlines well before actual rate cuts do.

So, what exactly am I referring to when talking about the Fed’s balance sheet? The simple answer is the Securities Held Outright line items. For a little Fed Balance Sheet 101, this is also known as the System Open Market Account or SOMA. The reader probably is more familiar with the terms quantitative easing (QE) and quantitative tightening (QT) when addressing the Fed’s balance sheet.

Securities Held Outright by the Fed

Recall that while the policy maker was busy implementing historic rate hikes from 2022–2023, it was also reducing its holdings of Treasuries and mortgage-backed securities (MBS), which had ballooned in size as a result of the COVID-19-related QE program. This latter portion of monetary policy tightening was QT. Fast-forward to the present, and it appears as if the FOMC is ready to start paring back the pace of QT, even if it is not ready to start implementing rate cuts.

Let’s look at the Fed’s securities holdings to get some perspective on how the current QT program has been working. At its peak, SOMA reached as high as $8.5 trillion in May 2022, and since QT went into effect in June of that year, total holdings have dropped more than $1.5 trillion to $6.97 trillion as of this writing. This reduction is the result of the Fed’s present plan to let its Treasury and MBS positions roll off by a combined $95 billion per month. Remember, the Fed is not outright selling any securities; it is just not reinvesting the total amount of holdings that are maturing or being redeemed.

Based on last week’s release of the March FOMC minutes, the Fed seems to be considering reducing the aforementioned roll-off amount in half, which could amount to roughly $50 billion per month. In addition, the policy maker’s preference seems to be to pare back only the pace of QT that includes the Treasuries portion of its overall holdings, not MBS.

Interestingly, several Fed officials have gone on record that the ultimate goal would be to have only Treasury securities on its balance sheet. However, this could take quite some time, as the Fed’s balance sheet is holding nearly $2.4 trillion in MBS, and the current pace of the roll-off here is $35 billion per month.

Conclusion

While the money and bond markets await guidance on rate cuts, they may be getting another announcement as soon as the upcoming May FOMC meeting that a “QT taper” is on the immediate horizon instead.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.