XSOE

Emerging Markets ex-State-Owned Enterprises Fund

Published November 15, 2024

Director, Research

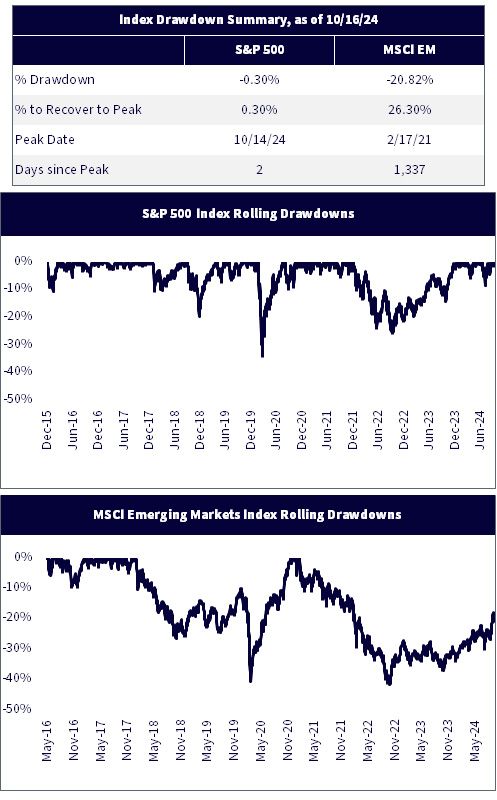

The S&P 500 has repeatedly hit new all-time highs this year.

The MSCI EM Index is still 20% below its early 2021 peak.

For investors looking for valuation and mean reversion opportunities, EM is a clear favorite over the U.S.

Just to retrace back to its high-water mark of over three years ago, the EM index would have to return over 26%, as shown in figure 1.

Sources: WisdomTree, FactSet, S&P, Russell, MSCI. Indexes are price return indexes measured in USD. You cannot invest directly in an index. Past performance is not indicative of future returns. Starting points based on data availability. S&P 500 start on 12/31/15. MSCI EM start on 5/31/16.

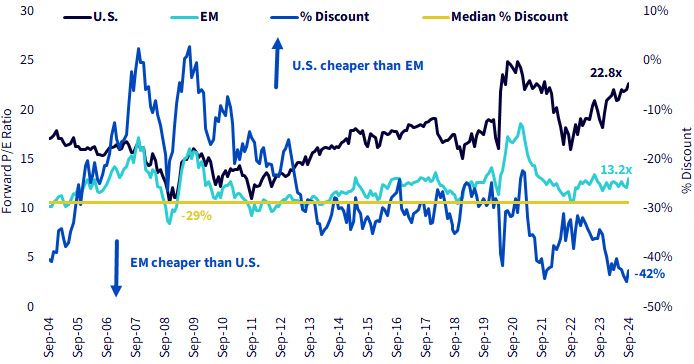

From a valuation perspective, figure 2 shows us that EM is trading at a 42% discount on forward P/E relative to the U.S.—one of the largest discounts going back two decades.

Sources: WisdomTree, FactSet, MSCI, 9/30/04–9/30/24. U.S. = MSCI USA. EM = MSCI Emerging Markets. You cannot invest directly in an index. Past performance is not indicative of future returns.

WisdomTree offers a robust lineup of EM options for investors looking to capitalize on valuation opportunities in EM, and it’s an exposure we’ve been recognized for in the industry.

Late last month, WisdomTree won “Best Emerging Markets Equity ETF Issuer ($10bn+)” at the ETF Express US Awards.1

Our largest family of products in EM is our ex-state-owned family. WisdomTree designed proprietary ex-state-owned Indexes to represent broad regional and country-specific exposures. SOEs are defined in our Indexes as companies with 20% or more of their shares owned by the government.

Our two broad EM Funds that track these Indexes are the WisdomTree Emerging Markets ex-State-Owned Enterprises Fund (XSOE) and the WisdomTree Emerging Markets ex-China Fund (XC).

The Indexes tracked by these two Funds underwent their annual rebalances this October. Each Index had modest turnover (<10% one-way turnover).

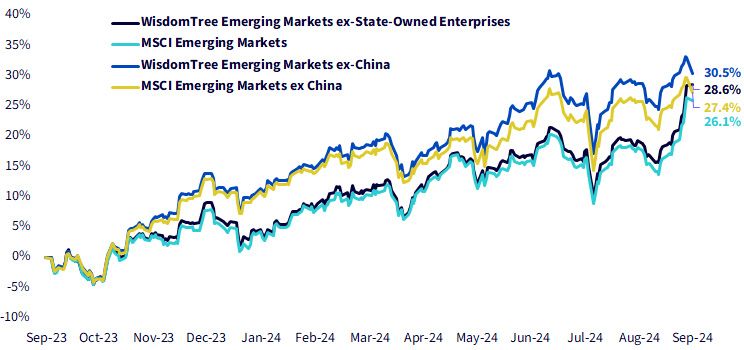

Over the last 12 months, as of the September 30 screening date, the WisdomTree Emerging Markets ex-China Index (WTEMXC) outperformed the WisdomTree Emerging Markets ex-State-Owned Enterprises Index (EMXSOE) by nearly 200 basis points. This performance spread was consistent with the relative performance between the MSCI EM Index and the MSCI Emerging Markets ex China Index, which is shown in figure 3.

The lagging returns of China—reversed somewhat in recent weeks amid government stimulus speculation—and the ever-present political risks of Chinese investments has increased attention to allocations to ex-China EM options like XC.

Sources: WisdomTree, FactSet, 9/29/23–9/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

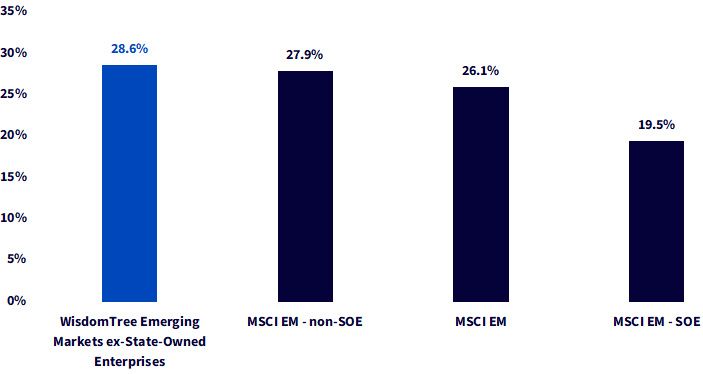

Each of the WisdomTree Indexes outperformed the respective MSCI EM index over the last 12 months. The underperformance of state-owned enterprises—excluded from both our Indexes—explains why.

In figure 4, we see that while the overall MSCI EM Index was up 26.1%, SOEs were up just 19.5%, lagging non-SOE companies by over 800 basis points.

The WisdomTree Emerging Markets ex-State-Owned Enterprises performed slightly better than the MSCI EM – non-SOE group, with a return of 28.6% over the one-year period.

Sources: WisdomTree, FactSet, 9/29/23–9/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

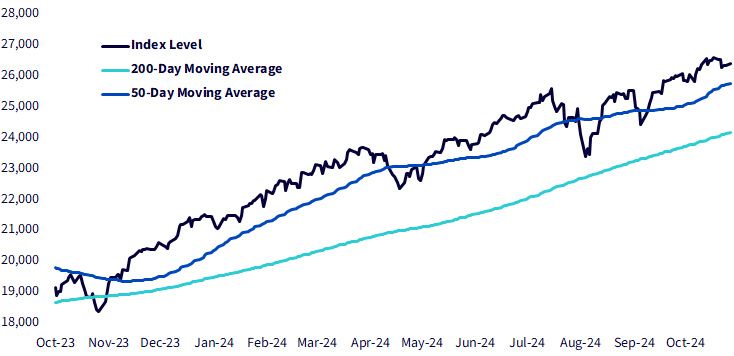

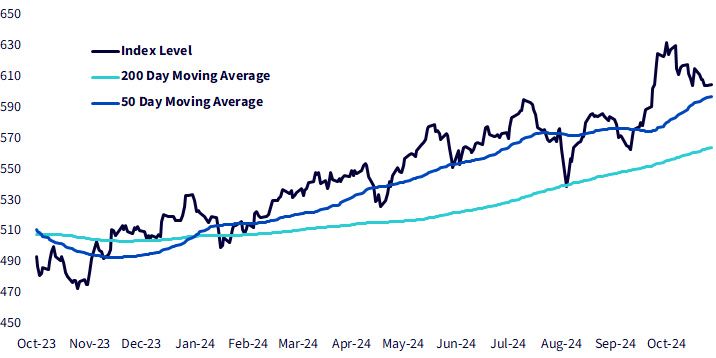

As previously noted, the U.S. has been on a tear so far this year with returns of well over 20%.

But the returns of broad EM have been strong as well—up over 13%.

Comparing recent trends in returns from the moving averages of the MSCI U.S. and EM indexes in figures 5 and 6 we see a similar compelling picture of strong momentum where the short-term (50-day) moving average is well above the long-term (200-day) moving average in both markets.

Sources: WisdomTree, MSCI, 10/1/23–10/28/24. Index levels based on gross total return levels for the MSCI USA Index and net total return levels for the MSCI EM Index. Past performance is not indicative of future returns. You cannot invest directly in an index.

We understand many investors are more tactical asset allocators in EM. To this point, the bull case for an allocation today is a combination of historically low relative valuations and the tailwinds of a positive momentum backdrop.

And when comparing EM options and the various risks involved, systematically removing SOEs is one way to mitigate the risks inherent in investing alongside the government.

1 US Awards Winners 2024, ETF Express, https://etfexpress.com/wp-content/uploads/2024/11/ETF-US-Awards-24-ver-3.pdf.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

XC: Investments in emerging markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks. The Fund’s investment strategy limits the types and number of investment opportunities available and, as a result, the Fund may underperform other funds. The Fund’s exposure to certain sectors, countries or regions may increase its vulnerability to any single economic or regulatory development related to such sector, country or region. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets.

XSOE: Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Funds focusing their investments on certain sectors and/or regions increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets.

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.