WDAF LN

WisdomTree Asia Defence UCITS ETF - USD Acc

Published March 31, 2026

Associate Director, Quantitative Research & Multi Asset Solutions

As the US refocuses and pushes allies to shoulder more of their own defence burden, Asia is emerging as an increasingly important part of the global defence buildout. What may once have looked like a series of geopolitical flashpoints is increasingly taking shape as a regional, multi-year industrial trend.

This is not only a story of increasing defence budgets. It is also a story of expanding domestic capability, firmer procurement plans and a broader listed opportunity set. Across the region, governments are responding to a tougher security backdrop with resilient defence spending growth, clear strategic priorities, and a strong push to build local industrial capacity.

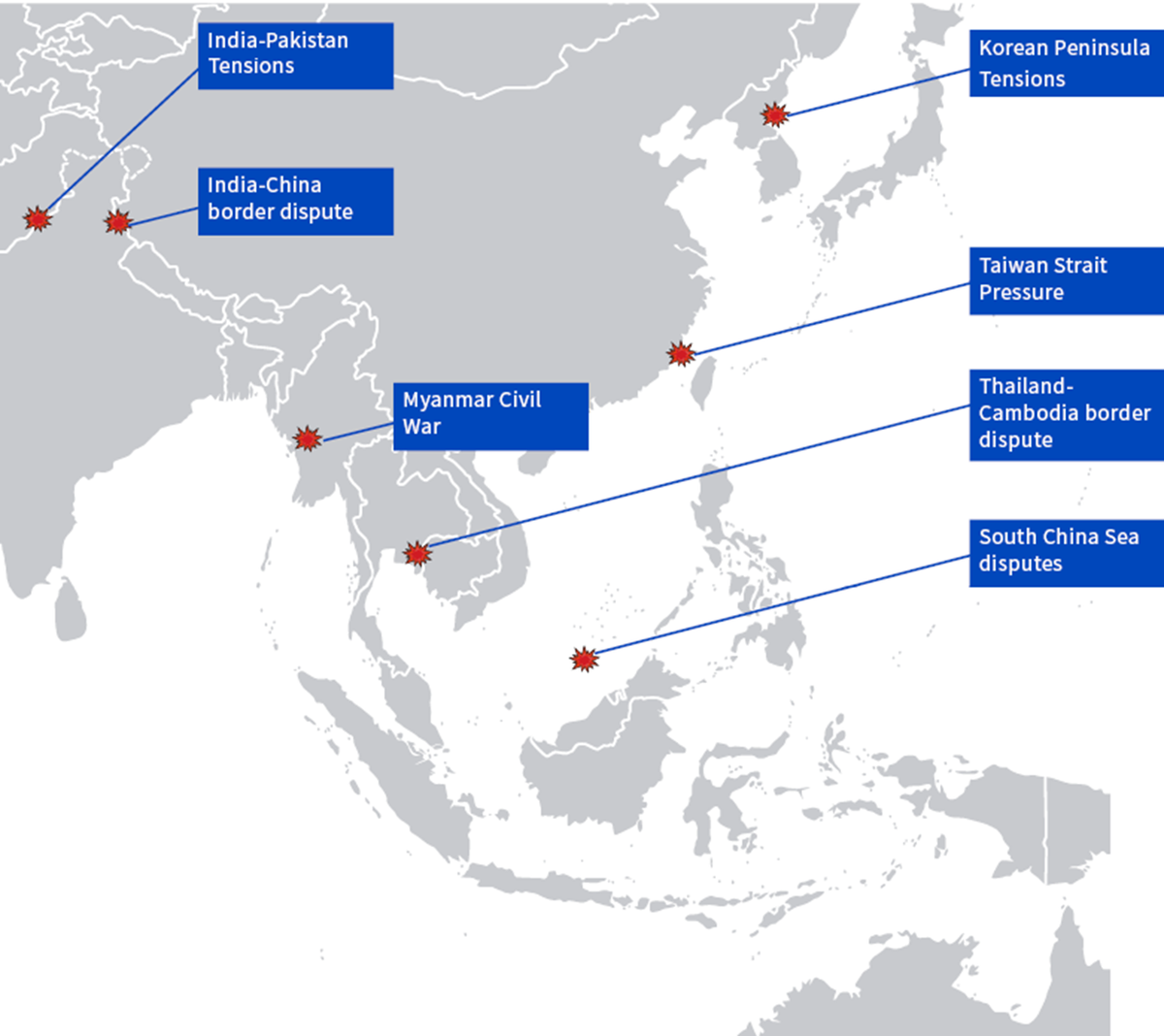

Persistent threat environment: Tensions around the Taiwan Strait, the Korean Peninsula and the India-Pakistan border continue to keep readiness high. That supports demand not only for new platforms, but also for munitions, maintenance, upgrades, training and sustainment. Once readiness requirements move up, these categories tend to become more recurring and less discretionary.

Source: Peace Research Institute Oslo (PRIO), WisdomTree.

Strategic autonomy: As the US asks allies and partners in Asia to shoulder more of the burden, governments across the region are placing greater weight on self-reliance. That means more local production, more domestic qualification, more in-country maintenance and a larger role for national champions. In investment terms, it means a greater share of defence spending can remain within local industrial ecosystems rather than flowing abroad.

Policy and spending support: In several major Asian markets, stronger defence spending is now supported by formal strategy documents, updated doctrine, and longer funding horizons. That improves revenue visibility, supports capacity expansion and gives companies greater confidence to invest in production lines, inventories and supply chains. This is important because it turns a geopolitical concern into a more investable industrial theme.

Cross-sectoral synergies: Defence modernisation increasingly extends to drones, cyber, space, and other dual-use sectors. This is not just about shipbuilders or aircraft manufacturers. It is also about subsystem suppliers, enabling technologies and dual-use businesses that sit deeper in the value chain.

The country cases help to show why the theme has momentum. The drivers vary by market, but the direction is consistent.

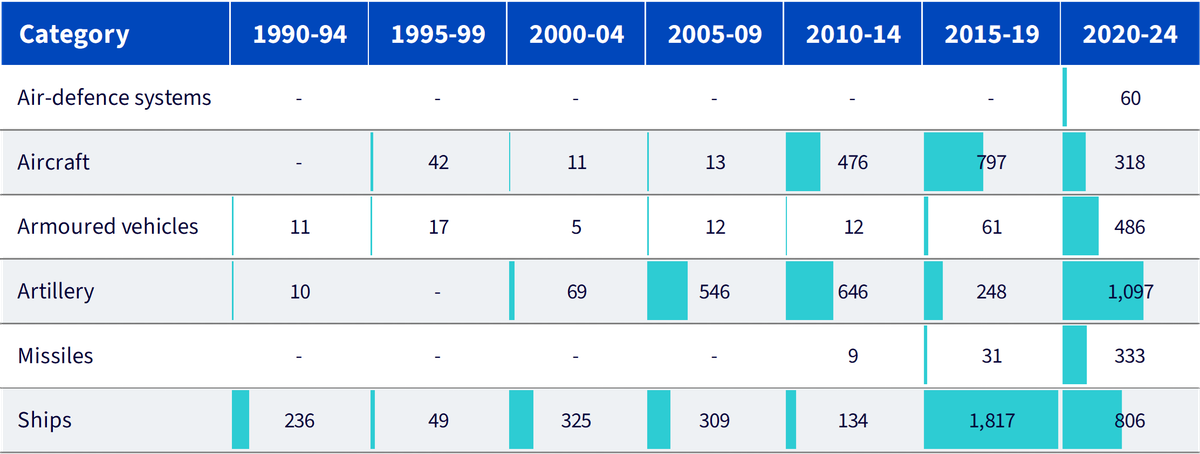

Source: SIPRI Arms Transfers Database, Mar. 2025. The bars compare the values of exports of different categories of major arms in each period, calculated using SIPRI trend-indicator values. SIPRI Trend-Indicator Values (TIVs) are SIPRI’s standardised measure of the volume of international transfers of major conventional weapons, based on the military resources transferred rather than their financial value. Historical performance is not an indication of future performance and any investments may go down in value.

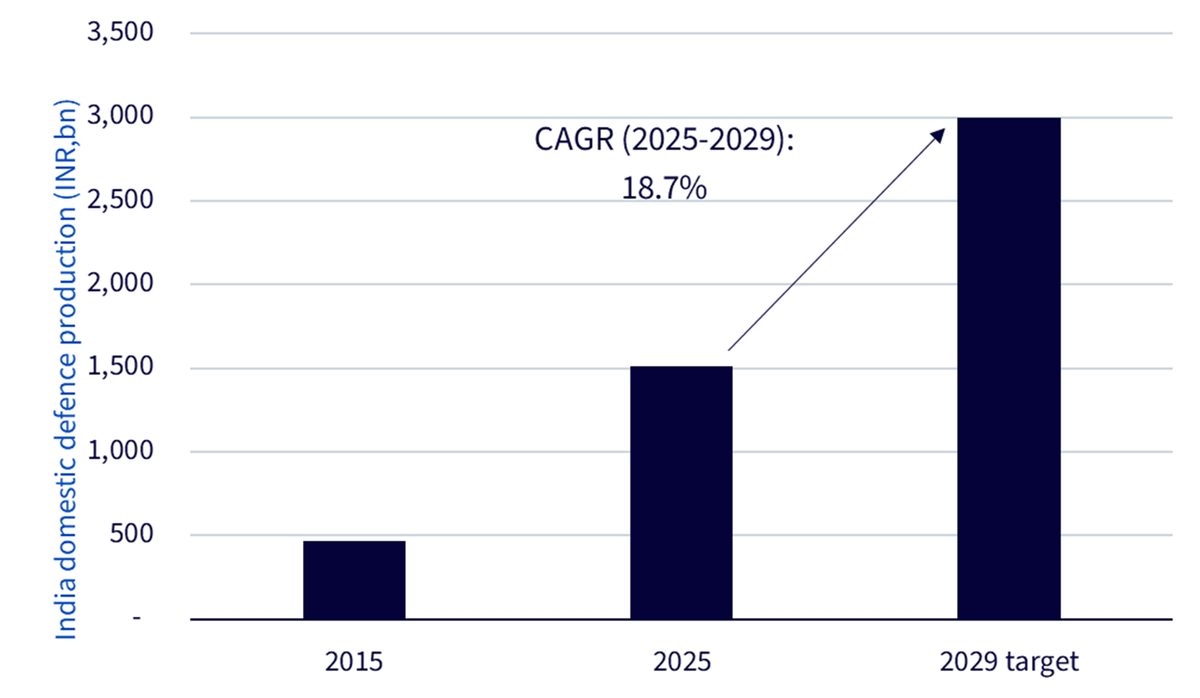

Source: United Service Institution of India, Assessment of India’s Indigenous Defence Manufacturing Capabilities, May 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Taken together, they reinforce the same broader point. Asia defence is becoming more structural, more local and more investable.

WisdomTree Asia Defence UCITS ETF (WDAF) is designed to give investors targeted exposure to Asia Pacific ex-China companies with meaningful involvement in the defence industry. Following the successful launch of WisdomTree Europe Defence UCITS ETF (WDEF), the WisdomTree Asia Defence UCITS ETF extends that approach to another region where defence spending, strategic autonomy and industrial buildout are becoming increasingly important.

The exchange-traded fund (ETF) tracks the WisdomTree Asia Defence UCITS Index, which targets companies deriving at least 10% of their revenue from defence activities and tilts towards those with higher exposure. This creates a more focused, pure-play profile, screening out diversified conglomerates where defence is only marginal, while giving greater weight to companies more directly positioned to benefit from Asia’s military modernisation cycle.

To be eligible, companies must also meet minimum market capitalisation and liquidity requirements. The strategy further applies controversial weapons screening1.

Each selected company is assigned an Exposure Score from 1 to 3 based on the revenue exposure to defence activities.

The Index is weighted by market capitalisation adjusted by the Exposure Score, subject to the capping2 and liquidity adjustment criteria. Companies with higher market capitalisation and Exposure Scores are assigned greater weights. The Index is rebalanced on a quarterly basis.

The portfolio is designed to reflect the breadth of Asia’s defence buildout while maintaining a clear focus on companies with meaningful exposure to the theme.

Source: WisdomTree. Holdings are based on target weights as of 27 February 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

As shown in Figure 1, the Index includes companies across Japan, South Korea, India, Australia and Southeast Asia. It is reconstituted quarterly to reflect changes in the defence sector.

Figure 5: Top 10 holdings in WisdomTree Asia Defence UCITS Index

Top 10 Holdings | Country | Weight |

|---|---|---|

Hanwha Systems Co Ltd | South Korea | 12.70% |

Korea Aerospace Industries Ltd | South Korea | 11.40% |

Hanwha Aerospace Co Ltd | South Korea | 7.70% |

Bharat Electronics Ltd | India | 6.90% |

Kawasaki Heavy Industries Ltd | Japan | 6.00% |

Hindustan Aeronautics Ltd | India | 5.10% |

Mazagon Dock Shipbuilders Ltd | India | 4.90% |

Singapore Technologies Engineering | Singapore | 4.10% |

Mitsubishi Heavy Industries Ltd | Japan | 3.90% |

Hanwha Ocean Co Ltd | South Korea | 3.80% |

Total 10 weights | 66.50% |

As shown in Figure 2, the strategy’s top holdings illustrate its design logic. As of late February 2026, the portfolio’s 10 largest positions, ranging from Hanwha Aerospace and Korea Aerospace Industries in South Korea to Hindustan Aeronautics, Mazagon Dock Shipbuilders and Bharat Electronics in India, represented about 66.5% of the total weight.

These companies are not just national champions. They are increasingly becoming exporters of security. Hanwha’s joint venture in Poland for missile production, India’s Cochin Shipyard expansion and Japan’s Kawasaki Heavy Industries’ global supply chain all point to Asia’s rise not only as a defence buyer, but also as a defence supplier.

Asia’s defence cycle is becoming more structural and more investable, driven by a tougher threat backdrop, rising strategic autonomy and deeper industrial capacity across the region. The WisdomTree Asia Defence UCITS ETF (WDAF) provides targeted, rules-based exposure to that opportunity, with a portfolio tilted towards companies with more direct defence revenue exposure.

Ticker | Exchange | ISIN | Bloomberg Code | Listing Currency | Base Currency | TER % |

|---|---|---|---|---|---|---|

WDAF | LSE | IE000017NMH7 | WDAF LN | USD | USD | 0.50% |

WDAP | LSE | IE000017NMH7 | WDAP LN | GBx | USD | 0.50% |

WDAF | Borsa | IE000017NMH7 | WDAF IM | EUR | USD | 0.50% |

WDAF | Xetra | IE000017NMH7 | WDAF GY | EUR | USD | 0.50% |

WDAF | SIX | IE000017NMH7 | WDAF SW | USD | USD | 0.50% |

WDAF | Paris | IE000017NMH7 | WDAF FP | EUR | USD | 0.50% |

1 The strategy seeks to exclude companies that are involved in certain controversial weapons, such as anti-personnel mines, cluster munitions, chemical and biological weapons, depleted uranium weapons and white phosphorus weapons and those that support nuclear weapons programs to states outside the Treaty on the Non-Proliferation of Nuclear Weapons (commonly known as the Non-Proliferation Treaty or “NPT”).

2 The maximum weight of any security with an Exposure Score 3 is capped at 7.5% and other securities are capped at 4%.

WisdomTree Asia Defence UCITS ETF - USD Acc

Associate Director, Quantitative Research & Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).