Gold Monthly: Rebounding after a Violent Drawdown

Published May 7, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- After a historic surge in January 2026 followed by the sharpest drawdown since 2013 in March, gold rebounded in April as liquidity-driven selling fades, reinforcing the case for maintaining exposure through strategies like the WisdomTree Efficient Gold Plus Equity Fund (GDE) to capture the recovery alongside equity upside.

- Despite near-term volatility driven by geopolitical shocks, rising yields and a stronger U.S. dollar, structural demand from Asian investors, central banks and new buyers like Chinese insurers is accelerating—supporting a higher long-term price regime and favoring diversified exposure via funds like WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN) that combine gold and miners.

- With Asian gold ETP flows exceeding $14 billion year-to-date and the dollar weakening again in April, investors should view recent pullbacks as tactical entry points to allocate to gold-integrated strategies that hedge macro risks while preserving portfolio flexibility.

In January 2026, gold posted its largest monthly gain since September 1999, before recording its sharpest decline since June 2013 in March.1 The first quarter of the year has therefore been exceptionally eventful for the yellow metal.

In April, gold began to recover part of its March losses, although the rebound remains incomplete.

We believe gold is transitioning towards a new, higher equilibrium price level, supported by a broadening investor base. Chinese insurance companies, Indian pension funds and digital asset issuers such as Tether represent relatively new sources of demand.2 At the same time, gold exchange-traded product inflows in both China and India have increased significantly over the past year.3

While this transition is likely to remain volatile, it suggests gold prices may ultimately stabilize at higher levels. For long-term investors, such periods of volatility may present opportunities rather than risks.

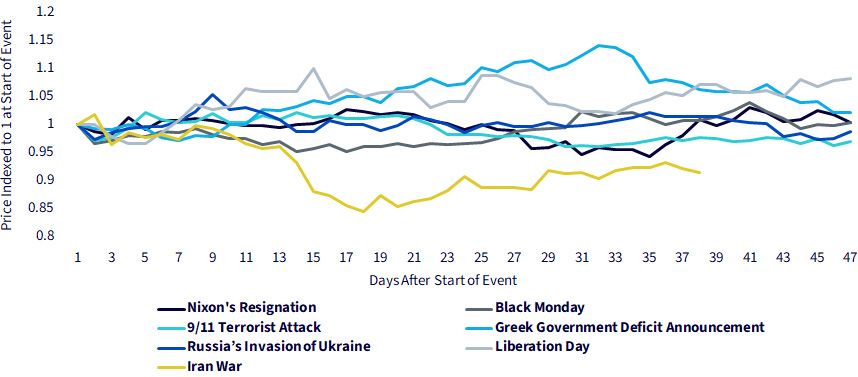

Geopolitical Risk—Initial Drawdown Before Recovery

Gold is traditionally viewed as a hedge against geopolitical risk. However, its response is often non-linear, with initial declines followed by subsequent gains.

The underlying mechanism is consistent. A geopolitical shock typically triggers declines in risk assets such as equities, leading to margin calls and a scramble for liquidity. Gold, as a highly liquid asset, is often sold to meet these obligations, creating temporary downward pressure on prices.

This should not be interpreted as a loss of confidence in gold. Rather, it reflects gold’s role as a source of liquidity in times of stress. Historically, once these forced-selling dynamics subside, gold prices tend to recover as the geopolitical risk premium becomes the dominant driver.

Following the recent escalation in tensions involving Iran, gold came under pressure from liquidation flows. The drawdown was sharper than in many previous geopolitical episodes, partly because prices were already correcting from elevated levels reached in January 2026. By late March, a turning point appeared to have been reached, with gold posting relatively consistent gains through April.

A fragile ceasefire, extended in late April 2026, provided some relief to risk markets.4 However, the broader situation remains uncertain. Limited escalation does not yet imply meaningful de-escalation, and ongoing tensions, particularly around the Strait of Hormuz, are likely to sustain geopolitical and inflationary concerns, which could remain supportive for gold prices.

Figure 1: Gold’s Price Performance after Geopolitical Events

Source: Bloomberg Finance L.P., WisdomTree, 1974-2026. Past performance is not indicative of future results.

Gold as a Source of Liquidity in Times of Stress for Central Banks

It is not only investors who sell gold in times of stress; central banks can behave similarly. Turkey provides a clear example. In March 2026, the central bank mobilized approximately 58–60 tonnes of gold within a two-week period to support the Turkish lira.5

Importantly, part of this activity involved gold swaps rather than outright sales, effectively collateralized foreign exchange (FX) intervention, in which gold remains on the balance sheet. The timing of these swaps is not publicly disclosed.

While such actions may initially appear negative for gold prices, they reinforce gold’s role as a highly liquid and trusted reserve asset. Both investors and central banks turn to gold in times of stress, not as a rejection of the asset, but as validation of its utility.

Historical precedent supports this interpretation. Following significant gold sales in 2023 to stabilize domestic markets after an earthquake, Turkey subsequently rebuilt its gold reserves over the following months.6 A similar pattern may emerge over time.

While most central banks have yet to report March 2026 activity to the International Monetary Fund (IMF), February purchases were strong, following a lull in January when prices were elevated. Poland was the largest reported buyer, adding 20 tonnes, its highest monthly purchase since February 2025. This brings its total gold reserves to 570 tonnes (31% of total reserves), with a stated target of 700 tonnes.7

Uzbekistan added 8 tonnes, bringing reserves to 407 tonnes (88% of total reserves), while the People’s Bank of China extended its buying streak to 16 consecutive months, with holdings reaching 2,308 tonnes (around 10% of total reserves).8

Recent discussions in Poland have also highlighted the potential use of gold reserves as a financial tool. Policymakers have explored the possibility of leveraging gold holdings to support defence spending, although proposals remain controversial and lack full government approval. Details remain unclear, particularly regarding whether this would involve outright sales or more complex financial operations.

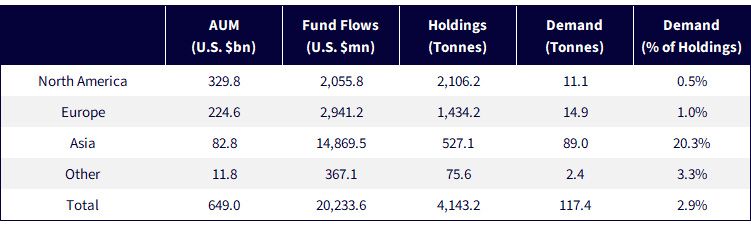

Asia is Dominating Exchange-Traded Product Flows

As we can see in Figure 2, Gold exchange-traded products have been dominated by Asian products so far this year, with over U.S.$14bn of flows. That demand represents more than 20% of Asian gold ETP holdings, underscoring the rapid pace of gold accumulation in the region. In 2025, gold AUM in Asia doubled. As mentioned earlier, Chinese insurance companies and Indian pension funds have recently become new eligible buyers of the gold ETPs.

The year started off strong for North American gold ETP demand with more than $11.5bn inflows in January and February combined. However, by the end of March, those inflows had been fully reversed. By April 17, year-to-date flows had returned to a net inflow of over $2bn. In Europe, on the other hand, January and February were relatively slow months, and March saw only small outflows. But April proved to be a strong month, with close to $3bn of inflows through April 17.

Figure 2: Exchange-Traded Product Flows in Gold, by Region

Source: World Gold Council, January 1, 2026–April 17, 2026. Past performance is not indicative of future results.

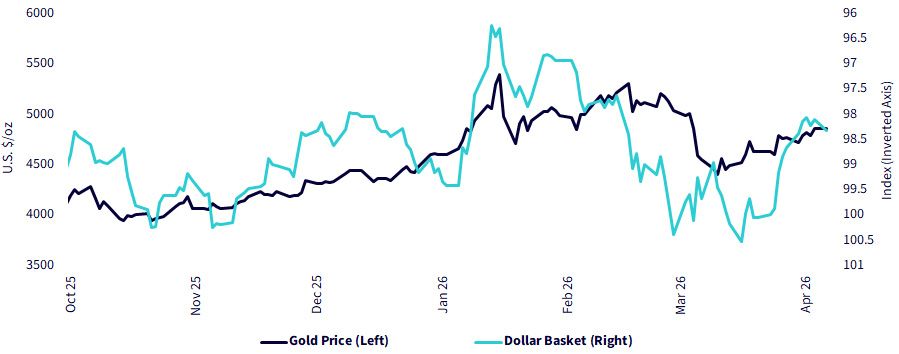

Dollar Depreciating Once Again

In February and March, gold came under pressure from a strengthening U.S. dollar. As a net energy exporter, the United States has been relatively insulated from recent geopolitical tensions compared to many other economies. As a result, the U.S. dollar outperformed other traditional haven assets such as the Swiss franc, Japanese yen, and gold during this period.

However, as is clear in Figure 3, the U.S. dollar resumed its depreciating trend in April, providing support for gold prices. Widening twin deficits are likely to drive structural dollar weakness over time, although U.S. energy strength may partially offset this dynamic.

Figure 3: Gold and U.S. Dollar Basket

Source: Bloomberg Finance L.P., WisdomTree, October 2025-April 2026. Past performance is not indicative of future results.

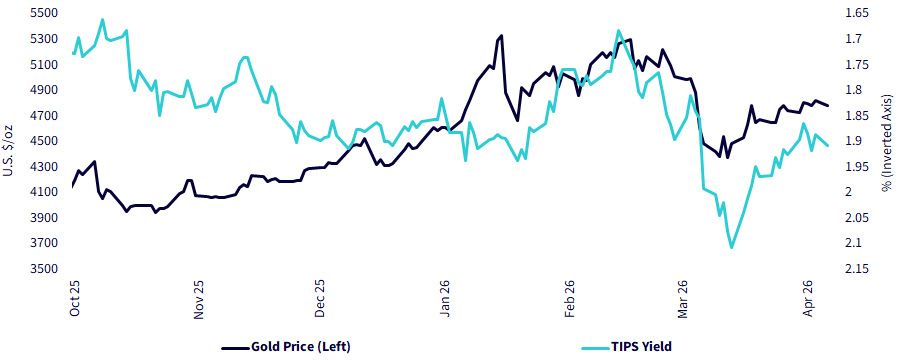

Bond Headwinds Ease

While the relationship between gold and bond yields has appeared more unstable in recent years, a short-term inverse relationship remains observable.

The rise in bond yields in March 2026 once again weighed on gold prices, with weaker Treasury auctions reflecting supply-related pressures. In April, demand at both 3-year and 10-year auctions has been closer to expectations, contributing to a moderation in yields.

This easing in yields has supported gold’s recovery in April. We see this story playing out in Figure 4.

Figure 4: Gold versus Real Rates (U.S. Treasury Inflation-Protected Securities Yields)

Source: Bloomberg, WisdomTree, October 2025-April 2026. Past performance is not indicative of future results.

Conclusion

Gold’s recent correction appears to have been driven more by liquidity pressures than by any meaningful shift in fundamentals. As these pressures fade, the underlying drivers of demand are reasserting themselves.

We see a supportive backdrop emerging: structural demand is broadening across regions and investor types, central banks remain engaged and macro conditions, ranging from geopolitical uncertainty to a softer U.S. dollar, are increasingly aligned with higher gold prices.

While volatility is likely to remain elevated, we view this as a feature of transition rather than a sign of fragility. In our view, gold is in the process of establishing a higher trading range, with pullbacks likely to be met by renewed demand.

At WisdomTree, we have addressed one of the primary issues faced by gold investors or investors considering becoming gold investors: How can a gold exposure fit within a broader allocation? Put more simply—what has to be sold to make room for gold?

WisdomTree’s efficient capital solutions represent strategies that incorporate multiple exposures in a single trade. Effectively, instead of needing to choose either ‘this or that’ these tools allow investors to allocate to both this AND that within a single strategy. Two strategies focused on gold have been generating live performance for more than three years:

- WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN): Often, when looking at gold, investors end up thinking about equities of companies that mine gold, which in many cases are paying dividends and running businesses highly exposed to gold’s price movements, and exposure to the metal. GDMNis designed such that for each hypothetical $100 invested, $90 is exposed to gold mining equities, $10 is exposed to short-term U.S. Treasury futures, and $90 is exposed to gold futures. In this way, the strategy provides exposure to both a measure of gold prices and gold miners, taking away the need to choose one or the other.

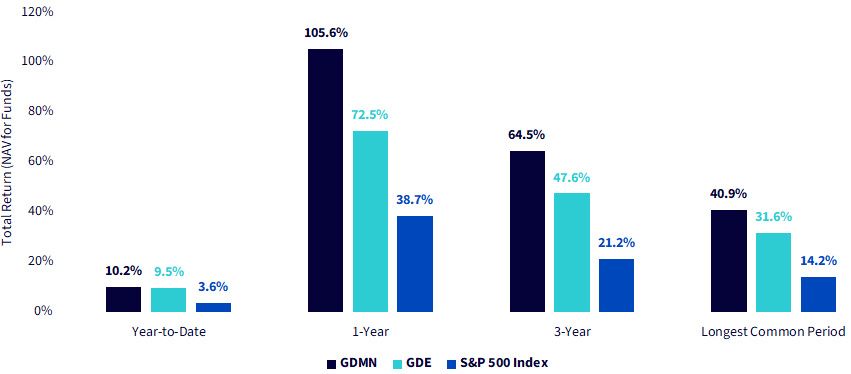

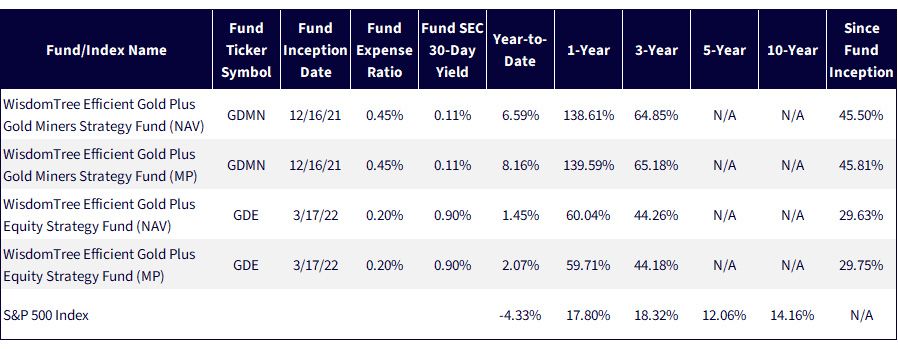

Given everything that has happened so far in 2026, it’s important to keep coming back to how these strategies are doing, as well as how they have done over the more medium-term time frames we are starting to be able to see. Strategies like these, in our view, earn their position more in volatile times when investors are less sure about gold’s price trajectory. Figures 5a and 5b paint this picture.

Figure 5a: The Performance Picture as of April 21, 2026

Figure 5b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically, data is from the PATH Fund Comparison Tool, accessed as of April 22, 2026, but showing returns for the period ended April 21, 2026 for Figure 5a and March 31, 2026 for Figure 5b. NAV denotes total return performance at net asset value. MP denotes market price performance. Longest common period goes back to GDE’s inception. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, GDMN, GDE.

- Source: Bloomberg Finance L.P.

- Sources: Insurance Journal (February 10, 2025). China frees possible $27 billion from insurers to buy gold; Mantra Mint (2026). Gold demand 2026: China insurance, India ETFs and central bank buying; Times of India (February 20, 2026). Why a crypto firm is buying more gold than most central banks.

- Source: World Gold Council (2026). Gold ETF flows: Q1 2026 update.

- Source: Kirby, P. (April 22, 2026). Trump extends Iran ceasefire as talks continue. The Guardian.

- Source: Karakaya, K., Ryan, J. and Akman, B. (March 26, 2026). Turkey’s $8 billion gold drawdown since Iran war hits bullion. Bloomberg News.

- Sources: World Gold Council (2023). Central bank demand flipped negative in April amid Turkish selling; World Gold Council (2023). Central banks and gold reserves: Turkey returns to gold accumulation following three-month liquidation.

- Source: International Monetary Fund (2026). International Financial Statistics: Poland—Total reserves and gold holdings [Data set].

- Source: International Monetary Fund (2026).

Source: Bloomberg Finance L.P.

Sources: Insurance Journal (February 10, 2025). China frees possible $27 billion from insurers to buy gold; Mantra Mint (2026). Gold demand 2026: China insurance, India ETFs and central bank buying; Times of India (February 20, 2026). Why a crypto firm is buying more gold than most central banks.

Source: World Gold Council (2026). Gold ETF flows: Q1 2026 update.

Source: Kirby, P. (April 22, 2026). Trump extends Iran ceasefire as talks continue. The Guardian.

Source: Karakaya, K., Ryan, J. and Akman, B. (March 26, 2026). Turkey’s $8 billion gold drawdown since Iran war hits bullion. Bloomberg News.

Sources: World Gold Council (2023). Central bank demand flipped negative in April amid Turkish selling; World Gold Council (2023). Central banks and gold reserves: Turkey returns to gold accumulation following three-month liquidation.

Source: International Monetary Fund (2026). International Financial Statistics: Poland—Total reserves and gold holdings [Data set].

Source: International Monetary Fund (2026).

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal.

GDMN: The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political, or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic, or regulatory conditions affecting that country or region, or emerging markets generally. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended.

GDE: The Fund is actively managed and invests in U.S. listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended.

Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributors

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Nitesh Shah

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.