WQTM

Quantum Computing Fund

Published November 26, 2025

Global Head of Research

Quantum mechanics has always delighted in paradoxes: the cat that’s both alive and dead, the particle that is also a wave. So perhaps it’s fitting that the world of quantum investing would take on a similar ambiguity. In October, reports surfaced suggesting that the Trump administration was in active discussions to take equity stakes in pure-play quantum computing firms like D-Wave, IonQ and Rigetti. Hours later, another report denied that any such talks were occurring1. Like a superposition2, both statements seemed true until observed, and neither confirmed anything definitive. The mere possibility, however, was enough to send these quantum names surging by double digits in a single trading session.3

Whether or not Washington ever takes those stakes may matter less than what the rumors represent. We’re witnessing a fusion of industrial policy and market psychology unlike anything since the postwar era. The Barron’s cover story on “How Trump Sparked a New Era of State Capitalism”4 frames it bluntly: Uncle Sam has become one of the most influential investors in America, converting subsidies and grants into equity positions across sectors from chips to minerals. The goal is dual: fortify supply chains and project national resilience. But in practice, each intervention rewrites the rules of private enterprise. Investors are suddenly learning to price political intent as a new risk premium, or opportunity.

Intel offers the clearest recent precedent. Once a symbol of American decline in semiconductors, it became a beneficiary of this new policy wave: A government grant turned into a 10% equity stake, followed by private inflows from SoftBank and NVIDIA. The outcome wasn’t just liquidity; it was legitimacy. Markets re-rated Intel not because of immediate profit improvement, but because a credible buyer of last resort had stepped in. The Trump stake bought Intel time, and time bought Intel confidence.5 In a capital-intensive business where psychology often leads fundamentals, that confidence can be worth tens of billions.

The quantum computing sector, still years away from commercial scale, now sits at the intersection of technology’s most speculative promise and the state’s most strategic ambitions. If Intel’s revival showed that a government stake can restore belief, the quantum paradox6 shows that even rumors of involvement can reprice entire industries. The outcome, whether the talks were real, denied or both, illustrates how markets are beginning to trade not just on the physics of qubits7, but on the politics of capital allocation. In that sense, quantum may be the perfect metaphor for this new industrial era: everything is uncertain until it isn’t.

For investors, the task now is to separate the narrative superposition from measurable progress. The four public quantum names, D-Wave, IonQ, Rigetti and Quantum Computing Inc., occupy a strange position in markets: companies with negligible revenues, immense optionality and capitalization structures that trade more on faith than fundamentals. They’ve each become proxies for different visions of quantum’s future, hardware, software and hybrid approaches to algorithmic acceleration. In that sense, they are not yet competing with one another so much as competing for belief: which firm can convince investors, partners and perhaps governments that their qubits will collapse the probability wave8 first. Whether state capital enters the picture or not, the real investment question may be whether confidence alone can sustain a quantum ecosystem long enough for the technology to prove itself.

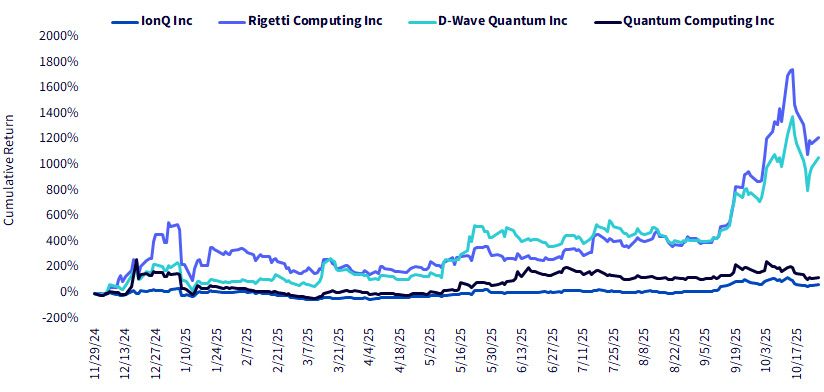

As we see in figure 1:

In our discussions with investors, we note that it’s far easier to write catchy headlines than it is to remember that the process to get to universal, fault-tolerate quantum computing9 will take a series of advances occurring over the coming years.

Sources: WisdomTree, Bloomberg and, for Google’s Willow chip announcement date, Google Research, “Meet Willow, our state-of-the-art quantum chip” [blog post], Google, 12/9/24. Past performance is not indicative of future returns.

At WisdomTree, we’ve designed our quantum computing methodology to systematically identify and weight the companies driving progress across the full stack of this emerging field, from the physics of qubits to the commercialization of cloud-based quantum services. The WisdomTree Quantum Computing Fund (WQTM) is the specific strategy reflecting this process.10

Each company is assigned a Relevancy Score, ranging from 1 to 3, reflecting the significance of its quantum computing involvement and its impact on the field’s advancement. Importantly, what we note below are guidelines to help investors understand what we mean when we say the relevancy score, but we are recognizing as well that quantum computing is a fast-moving space. If new details and important focal points are coming to light as quantum computing evolves, our framework is flexible enough to account for this in the future. We look at how what’s important or impactful in quantum computing is evolving, as well as what different companies are doing and how that may be evolving.

This layered approach ensures the portfolio remains anchored in the technology’s frontier while acknowledging the broader ecosystem that will make large-scale, universal, fault-tolerant quantum computing viable. In the latter part of 2025, we recognize the difference between what might provide utility in the near term, and what might be more geared toward the future fault-tolerant era in this space.

Alongside Relevancy, every company is tagged as Pure or Diversified, based on business focus and quantum revenue concentration.

This Purity dimension balances exposure: pure plays drive thematic precision and upside potential, while diversified leaders provide the potential for liquidity and volatility mitigation.

Once relevancy and purity are established, our methodology applies a two-stage weighting process. Equal-weighted starting positions are first adjusted upward for higher Relevancy Scores and then further scaled by Purity, giving pure and highly relevant firms the largest representation in the final Index. The outcome is a quantitatively disciplined yet thematically expressive portfolio, where index weights reflect not market cap dominance but quantum significance.

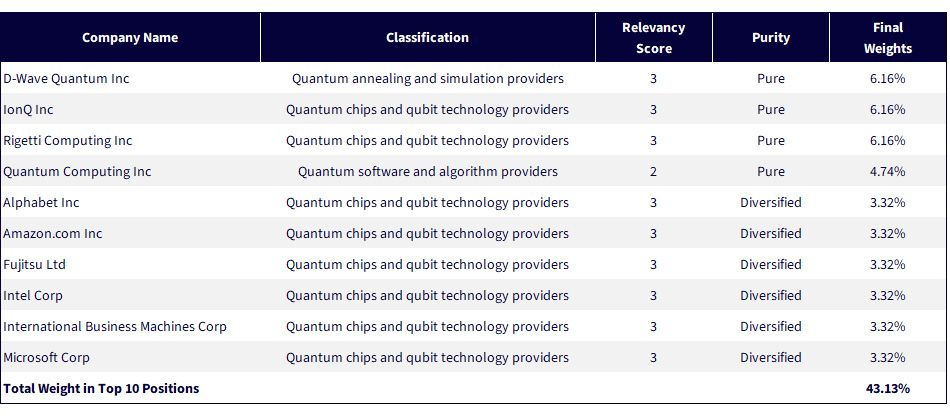

Visible in figure 2, as of the most recent rebalance in August 2025, the top 10 holdings represent 43.1% of the total Index, led by D-Wave, IonQ and Rigetti, each receiving the highest possible Relevancy and Purity designations. This structure helps ensure that if the market re-rates the sector, whether from government partnership rumors or real technical milestones, WisdomTree investors are positioned to capture the potential upside.

Sources: WisdomTree, Classiq, with data shown as of the August 2025 rebalancing process. Subject to change.

Quantum computing today sits in a peculiar state of duality; its commercial impact remains years away, yet its strategic importance is already undeniable. Governments debate whether to invest; investors debate whether to believe. And while both sides toggle between speculation and conviction, the real progress continues in laboratories, data centers and chip foundries across the world. The companies at the heart of this movement—those engineering qubits11, building error-correction algorithms and designing quantum operating systems—are shaping an infrastructure that will one day be as indispensable as semiconductors or cloud computing. The paradox is that you don’t wait for quantum computing to be certain before it becomes investable; you position for its inevitability while uncertainty is still priced in.

That’s precisely what WisdomTree’s methodology is designed to do. By combining quantitative discipline with qualitative insight, balancing relevancy, purity and ecosystem breadth, we’ve constructed a framework that is designed to capture the economic nucleus of quantum progress, not just its headlines. The outcome is an exposure that naturally tilts toward the innovators most likely to define the field’s future, while maintaining diversified ballast in enabling technologies and adjacent infrastructure. If the sector rallies, whether from a government catalyst, technical breakthrough or sudden re-rating of possibility, our structure helps ensure participation with purpose. In an industry where timelines stretch across decades, WisdomTree’s approach is about more than capturing returns; it’s about securing a front-row seat to the next computational epoch.

1 Sources: The Wall Street Journal Staff, “Trump administration in talks to take equity stakes in quantum computing firms,” The Wall Street Journal, 10/22/25; M. Tatananni and A. Clark, “Trump administration denies negotiating stakes in quantum computing companies: These stocks leaped on the news,” Barron’s, 10/23/25.

2 Superposition is the quantum principle that a qubit can occupy multiple states at once—such as 0 and 1—until it is measured. This property allows quantum computers to explore many possibilities in parallel.

3Source: M. Tatananni and A. Clark, 10/23/25.

4 Source: J. Light, “How Trump sparked a new era of state capitalism,” Barron’s, 10/22/25.

5 Source: M. Acton, “Intel shares jump on improved revenue as turnaround shows progress,” Financial Times, 10/23/25.

6 A quantum paradox is an apparent contradiction that arises when quantum behavior defies classical intuition, revealing how quantum systems operate differently from everyday physics. These paradoxes often highlight foundational limits of measurement, determinism, and observation.

7 Qubits are the basic units of quantum information that can exist in a combination of 0 and 1 simultaneously. They enable quantum computers to process information in ways impossible for classical bits.

8 A probability wave (or wavefunction) describes the mathematical distribution of all possible states a quantum system can occupy. Measuring the system collapses this wave into a single outcome.

9 Refers to methods that allow quantum computers to operate reliably even when individual qubits and operations experience errors. It relies on quantum error-correcting codes to ensure stable, scalable computation.

10 WQTM is designed to track the total return performance, before fees and expenses, of the WisdomTree Classiq Quantum Computing Index.

11 The physical hardware implementations of qubits—such as superconducting circuits or trapped ions—that embody the idealized quantum information unit in real devices. They come with real-world constraints like noise, decoherence, and fabrication limits.

For current holdings of WQTM, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the potential loss of principal. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. The economic, political, regulatory and other events and conditions that affect issuers and investments in the United States differ significantly from those associated with other countries and regions. U.S. financial markets have become increasingly globalized, becoming more integrated with financial markets around the world, and, as a result, U.S. financial markets are increasingly vulnerable to the risks that may affect non-U.S. financial markets. The Fund’s investments in the U.S. are particularly subject to the risk that they, and the U.S. economy more generally, will be adversely affected by a decrease in imports or exports, changes in trade regulations, inflation and/or an economic recession in the U.S. The Fund invests primarily in the securities of quantum computing companies. Companies engaged in the development of quantum computing or machine learning technology may be significantly impacted by rapid technological advancements, product obsolescence, intense competition, consumer demand and government regulation. Such companies are also heavily dependent upon patent and intellectual property rights. Tariffs placed on specialized components and/or raw materials used by such companies may increase costs and delay progress associated with research and developments in quantum computing and machine learning. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Quantum Computing Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.