DGRW

U.S. Quality Dividend Growth Fund

Published October 23, 2025

Equity Strategist

Thus far in 2025, the U.S. equity market has sent a perplexing signal to long-term investors: quality doesn't seem to matter. Through September, low-quality or "junk" companies—those with weak balance sheets, poor return on equity (ROE) or even negative earnings—have outpaced their higher-quality counterparts by wide margins. This reversal of fortune for companies that emphasize profitability, capital efficiency and operational consistency underscores that the market's appetite for speculation has reemerged in full force.

Investors who have historically sought exposure to strong, resilient business models have recently been punished. Markets have instead rewarded firms with shakier fundamentals, reflecting a speculative fervor that's reminiscent of late-cycle exuberance rather than disciplined long-term investing.

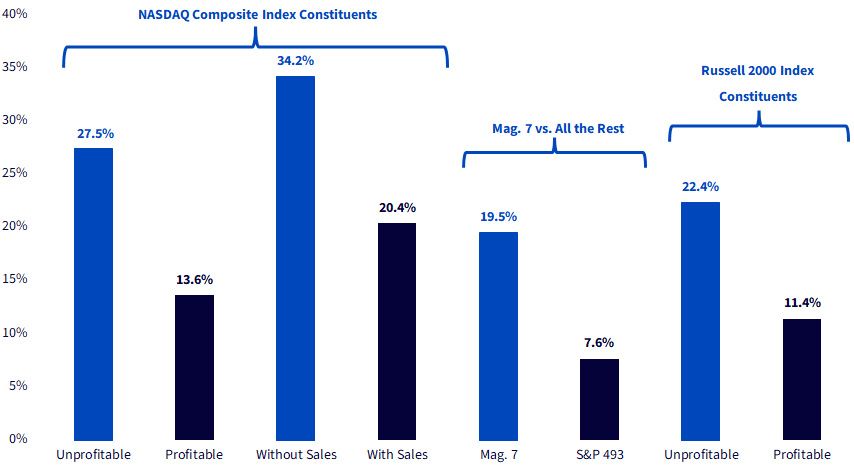

Nowhere is this trend more visible than in the performance of companies on the NASDAQ®. Over the year, NASDAQ®-listed companies without revenues outperformed those with revenuesby about 14%, on average, while unprofitable companies doubled the returns of profitable ones. The market has shown a clear preference for promise over performance.

Sources: WisdomTree, Bloomberg, for the period 9/30/24–9/30/25. Past performance is not indicative of future results. You cannot invest directly in an index. Unprofitable (Profitable) NASDAQ® companies are defined as active, NASDAQ® Composite Index-listed companies with negative (positive) trailing 12-month earnings per share. Non-Revenue (Revenue-Generating) NASDAQ® companies are defined as active, NASDAQ® Composite Index-listed companies that have not yet produced revenue (are currently generating revenue). Mag. 7 represented by the Bloomberg Magnificent 7 Index, which consists of Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla. Unprofitable (Profitable) Russell 2000 companies are defined as active companies in the Russell 2000 Index with negative (positive) trailing 12-month earnings per share. S&P 493 represented by the S&P 500 Index, excluding the seven companies comprising the Magnificent 7. Returns represent the arithmetic average trailing one-year return among constituents. Chart inspired by Schroders Equity Lens, October 2025.

Meanwhile, the Magnificent 7 is outperforming the rest of the S&P 500 by about 12%, on average, in a signal of weak breadth and narrow, concentrated market leadership.

This phenomenon isn't confined to large caps, either. Across the size spectrum, the same story plays out: unprofitable small-cap companies have doubled the returns of their profitable peers. This divergence highlights a concerning market dynamic, where speculation and momentum reign supreme over fundamentals.

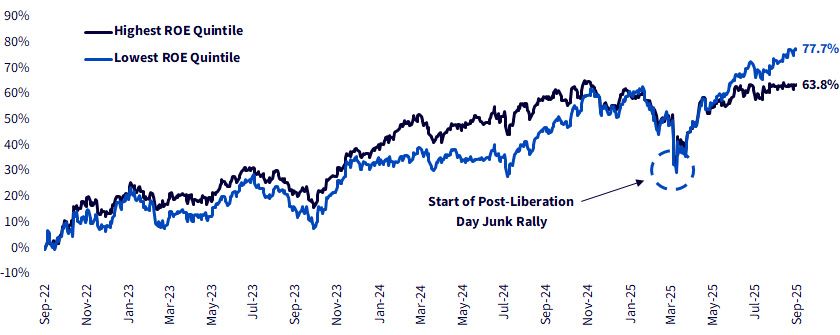

The junk trend is most visible when comparing the returns of the highest (and lowest) ROE quintiles of the MSCI USA Index over the past three years. The sharp reversal in favor of low-ROE stocks over the past year stands in contrast to the longer-term pattern of high-quality leadership. What we are witnessing now is, in essence, a short-term rally against the grain of a more enduring quality premium.

Sources: WisdomTree, FactSet, MSCI, for the period 9/30/22–9/30/25. Past performance is not indicative of future results. You cannot invest directly in an index. U.S. equities measured by MSCI USA Index. Quintiles rebalanced and equally-weighted at the end of September between 9/30/22–9/30/25.

These developments are antithetical to sound, long-term investing. Historically, companies with high ROE, solid balance sheets and consistent profitability have delivered stronger, more sustainable performance over full market cycles. While 2025's "junk rally" may persist longer than expected, we believe it will ultimately revert to a more fundamentals-driven market environment.

At WisdomTree, our equity strategies (especially those targeting quality as an investment factor) are grounded in the belief that strong fundamentals should not be ignored. Instead, they should be rewarded in investors' equity allocations.

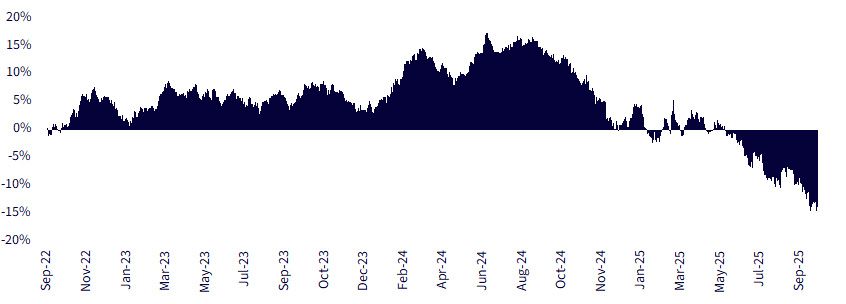

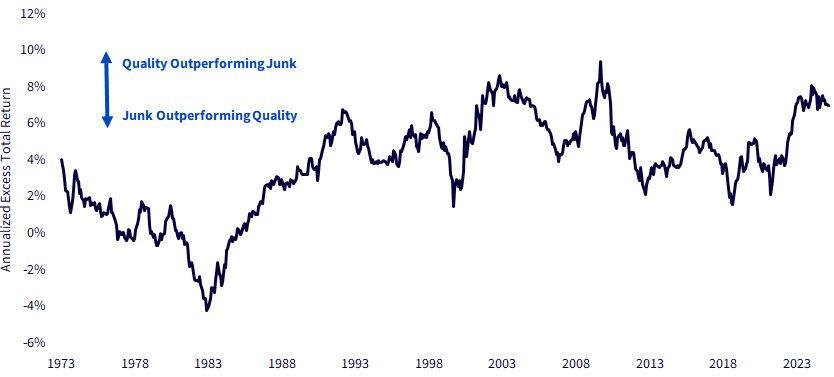

High-quality companies have historically outperformed both low-quality peers and the broader market over time, even if temporary speculative phases like the current one suggest otherwise. On a rolling 10-year basis, high-quality allocations have almost always been superior to low-quality stock baskets. Junk has not outperformed quality on a 10-year basis since the mid-1980s.

Sources: Fama French Data Library, Center for Research on Security Prices (CRSP), as of 8/31/25, which represents the most recently available data. Returns shown represent the difference in annualized total returns for a portfolio of U.S. companies with high measurements of operating profitability (defined as sales less cost of goods sold (COGS), selling, general and administrative expense (SG&A) and interest expense, then divided by book equity) versus a portfolio of U.S. companies with low measurements of operating profitability. Past performance is not indicative of future results.

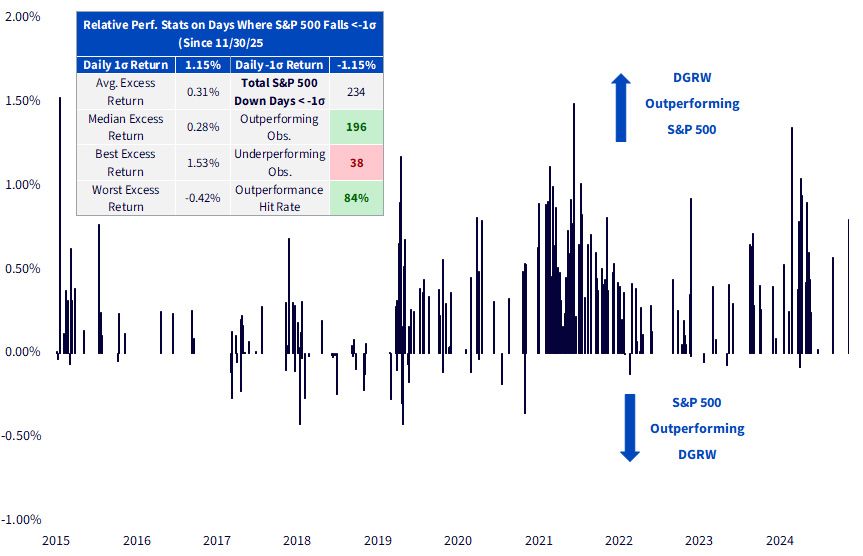

Moreover, high-quality investing may provide important defensive benefits when markets falter. The WisdomTree U.S. Quality Dividend Growth Fund (DGRW) offers a clear example.

Over nearly the past 10 years, DGRW has outperformed the S&P 500 84% of the time on days when the Index declined by roughly 1.15%—equivalent to a one-standard-deviation daily downside move. When the S&P 500 fell by 0.58% (a one-half-standard-deviation downside move), DGRW outperformed 76% of the time. Across all daily downside moves since the beginning of our daily return data series in November 2015, it has beaten the S&P 500 64% of the time, which is an impressive hit rate, in our view.

Sources: WisdomTree, S&P, as of 10/10/25. Past performance is not indicative of future results. You cannot invest directly in an index.

These results reinforce the resilience of, and need for, quality-focused strategies during turbulent periods that test investors' resolve.

The 2025 market narrative may tempt investors to question the efficacy of quality. Yet this "junk rally" is not a referendum on the merits of fundamentals—it's a temporary distortion fueled by speculative enthusiasm and narrow leadership. We believe that fundamentals may have a way of reasserting themselves, rewarding investors who stay disciplined and patient.

At WisdomTree, we remain confident that the quality premium will reemerge. The current environment may challenge conviction, but it also underscores why quality remains the cornerstone of resilient, risk-aware investing.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Quality Dividend Growth Fund

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.