Hard Money Forecasts: Bitcoin and Gold in 2030 and Beyond

Published October 15, 2025

Blake Heimann

Associate Director, Quantitative Research

Introduction

As inflation proves persistent, sovereign debt escalates and institutional trust wanes, investors are reassessing positioning and evaluating hard-asset allocations in their portfolios. Gold has long been the inflation hedge of choice, but bitcoin has emerged as a credible digital complement. Over the past decade, the investment case for bitcoin has matured from a speculative experiment in cryptocurrency to a scarce, digitally native asset with long-term store-of-value characteristics—earning it the moniker "digital gold."

Building on this narrative, we introduced a disciplined, scenario-based framework to forecast future valuations of both gold and bitcoin this summer in our full paper. Using macroeconomic dynamics and monetary supply analysis, the framework offers actionable perspectives for investors seeking long-term portfolio resilience.

The Historical Backdrop

Since 1970, the global money supply has exploded from under $1 trillion to over $100 trillion—a 100x expansion. This tidal wave of fiat creation, fueled by loose monetary policy and perpetual bailouts, has eroded long-term purchasing power.

As a result, hard-money assets, those that cannot be easily printed or manipulated, have gained traction. Gold, with its 5,000-year track record, remains the traditional hedge. But bitcoin has joined the conversation, offering a verifiably scarce, decentralized and digital alternative.

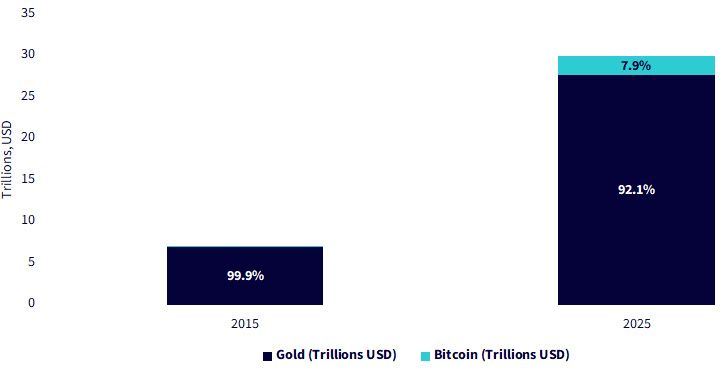

Together, bitcoin and gold now account for approximately ~29% of the estimated global money supply, with bitcoin commanding about 8% of the hard money basket.1 This shift reflects a growing institutional and retail pivot toward assets resistant to monetary dilution.

Figure 1: Hard-Money Basket, Now and 10 Years Ago

Sources: Bloomberg, CoinGecko, World Gold Council, as of October 10, 2025. Historical performance is not an indication of future performance and any investments may go down in value.

The Forecasting Framework

To assess the future value potential of these assets, WisdomTree applies a valuation model grounded in monetary dynamics. The model estimates future market capitalizations and subsequent prices for bitcoin and gold based on four variables:

- Forecasted global money supply under deflationary, base and inflationary scenarios.

- The share of that supply allocated to hard-money assets.

- Bitcoin's share within the hard-money basket.

- Projected supply of bitcoin and gold over time.

Pricebitcoin = M × H × B / Sbitcoin

Where M = total money supply, H = allocation to hard assets, B = bitcoin's share, Sbitcoin = circulating supply of bitcoin. Gold price can be modeled similarly.

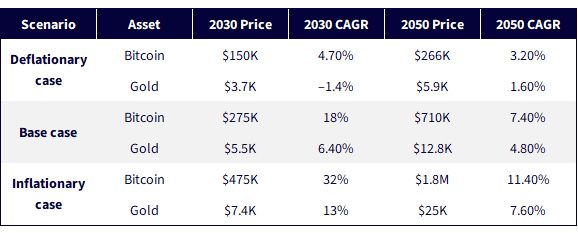

Assumptions and Results

We model three future scenarios for money supply growth and its implications for bitcoin and gold prices.

Deflationary case—hard assets shrink as a share of the pie:

Global money supply compounds at 3%, reaching ~$120 trillion by year end 2030.

Hard-money assets fall to 25% of money supply, resulting in a ~$30 trillion combined market capitalization for bitcoin and gold.

Bitcoin remains supply-capped, and gold supply grows at 1.5% per year with a decay factor of 0.95.2

Base case—reversion to historical norms supports both bitcoin and gold:

Money supply grows 5%, reaching ~$134 trillion by year end 2030.

Hard-money assets rise modestly from current levels to 35% of supply, creating a $47 trillion market.

Bitcoin captures 12% of the hard-asset basket as adoption continues.

Supply constraints mirror those in the deflationary case.

Inflationary case—fiat panic fuels a flight to digital scarcity:

Money supply grows 7%, reaching $150 trillion by year end 2030.

Hard-money asset share climbs to 45%, still below the 1970s’ peak.

Combined hard-asset market capitalization hits $65 trillion.

Bitcoin captures 15%, reflecting growing institutional interest and skepticism of fiat systems.

Supply assumptions remain unchanged.

These assumptions drive three distinct trajectories for bitcoin and gold, which we summarize below.

Figure 2: Model Results

Source: WisdomTree, October 2025. Cumulative average growth rate calculated using prevailing prices at time of writing: bitcoin $120,000 and gold $4,000 per oz. CAGR = compound annual growth rate. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Bitcoin and gold serve distinct yet complementary roles in an investment portfolio. Gold brings historical legitimacy and stability. Bitcoin brings programmable scarcity and asymmetric upside potential. Together, they may offer a multifaceted mitigation against fiat debasement and systemic shocks.

The case for these hard-money assets is turbocharged by the structural reality of modern monetary policy. With central banks locked into expansionary frameworks, assets that sit outside the fiat system stand to benefit, bitcoin disproportionately so in high-inflation scenarios.

Strategy in Action: GDE and GDMN

For investors seeking gold exposure without sacrificing equity allocations, WisdomTree offers two innovative ETFs:

- WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE): 90% equity, 90% gold futures

- WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN): 90% gold miners, 90% gold futures

These capital-efficient overlays allow investors to add gold exposure using just 10% collateral cash, providing efficient access without rebalancing from existing equity holdings.

Recent 1Y performance highlights their strength:

Figure 3: Standardized Performance

Source: WisdomTree, as of 10/9/25. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDE, GDMN.

These strategies showcase how gold allocations can be layered into equity portfolios, delivering diversification benefits while maintaining growth exposure.

Conclusion

Whether positioning for inflation protection, diversification or systemic uncertainty, gold and bitcoin present a compelling case. WisdomTree's macro-driven valuation framework avoids hype, instead grounding forecasts in monetary history and disciplined scenario analysis.

1 Source: Bloomberg, CoinGecko, World Gold Council, as of October 10, 2025 . Historical performance is not an indication of future performance and any investments may go down in value

2 Each year, the mining growth rate is multiplied by 0.95, and therefore the growth rate decays by 5%. Historically, gold has been mined at a rate between 0.5% and 1.5% of supply. Current levels are closer to the latter rate, but World Gold Council estimates depleting below-ground supply that aligns with reduced mining production in the years to come.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ, and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund-to-fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Material must be preceded or accompanied by a prospectus. Click the respective ticker to view the fund prospectus: GDMN, GDE.

GDMN: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“gold miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of gold miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

There are risks associated with investing, including the possible loss of principal. Crypto assets, such as bitcoin and ether, are complex, generally exhibit extreme price volatility and unpredictability, and should be viewed as highly speculative assets.

Crypto assets are frequently referred to as crypto “currencies,” but they typically operate without central authority or banks, are not backed by any government or issuing entity (i.e., no right of recourse), have no government or insurance protections, are not legal tender and have limited or no usability as compared to fiat currencies Federal, state or foreign governments may restrict the use, transfer, exchange and value of crypto assets, and regulation in the U.S. and worldwide is still developing.

Crypto asset exchanges and/or settlement facilities may stop operating, permanently shut down or experience issues due to security breaches, fraud, insolvency, market manipulation, market surveillance, KYC/AML (know your customer/anti-money laundering) procedures, non-compliance with applicable rules and regulations, technical glitches, hackers, malware or other reasons, which could negatively impact the price of any cryptocurrency traded on such exchanges or reliant on a settlement facility or otherwise may prevent access or use of the crypto asset.

Crypto assets can experience unique events, such as forks or airdrops, which can impact the value and functionality of the crypto asset. Crypto asset transactions are generally irreversible, which means that a crypto asset may be unrecoverable in instances where: (i) it is sent to an incorrect address, (ii) the incorrect amount is sent, or (iii) transactions are made fraudulently from an account. A crypto asset may decline in popularity, acceptance or use, thereby impairing its price, and the price of a crypto asset may also be impacted by the transactions of a small number of holders of such crypto asset. Crypto assets may be difficult to value and valuations, even for the same crypto asset, may differ significantly by pricing source or otherwise be suspect due to market fragmentation, illiquidity, volatility and the potential for manipulation.

Crypto assets generally rely on blockchain technology and blockchain technology is a relatively new and untested technology which operates as a distributed ledger. Blockchain systems could be subject to internet connectivity disruptions, consensus failures or cybersecurity attacks, and the date or time that you initiate a transaction may be different than when it is recorded on the blockchain. Access to a given blockchain requires an individualized key, which, if compromised, could result in loss due to theft, destruction or inaccessibility. In addition, different crypto assets exhibit different characteristics, use cases and risk profiles.

Information provided by WisdomTree regarding digital assets, crypto assets or blockchain networks should not be considered or relied upon as investment or other advice, as a recommendation from WisdomTree, including regarding the use or suitability of any particular digital asset, crypto asset, blockchain network or any particular strategy. WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor, end client or investor, and has no responsibility in connection therewith, with respect to any digital assets, crypto assets or blockchain networks.

Categories

About the contributor

Blake Heimann

Associate Director, Quantitative Research

Blake Heimann joined WisdomTree in 2020 and supports the creation, maintenance, and reconstitution of WisdomTree’s indices. Blake began his career in finance in 2017 as an Analyst at TD Ameritrade and, later, a Quantitative Analyst with a focus on the development of machine learning applications in finance.

Blake has bachelor’s degrees in Mathematics and Economics from Iowa State University, as well as a master’s in Computer Science from Georgia Tech, with a specialisation in Machine Learning. He is currently pursuing a master’s in Finance from the London School of Economics