HYZD

Interest Rate Hedged High Yield Bond Fund

Published September 22, 2025

Director, Fixed Income

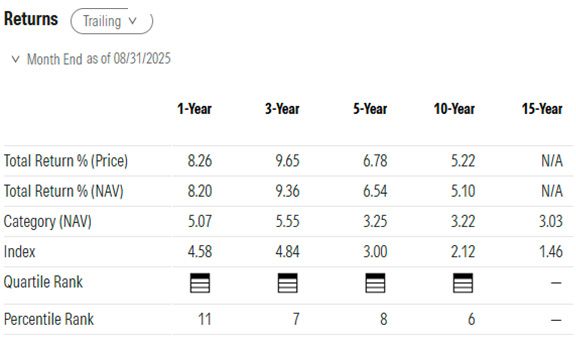

Among WisdomTree's suite of fixed income strategies, one Fund that often flies under the radar, but that has been steadily delivering strong results, is the WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD). As seen in figure 1, HYZD has consistently ranked strong across 1-, 3-, 5- and 10-year periods.

Source: MorningStar, as of 8/31/25. Morningstar, Inc., 2025. All rights reserved. Rankings shown for the Nontraditional Bond category. Morningstar Percentile Rankings are based on total returns. As of 9/30/25, the Morningstar Nontraditional Bond category included 244 funds for the 1-year period, 235 funds for the 3-year period, 216 funds for the 5-year period, and 149 funds for the 10-year period. Percentile rankings represent the fund’s total-return percentile rank compared to all funds in the same Morningstar category for each respective period. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers is responsible for any damages or losses arising from any use of this information. The Morningstar Rating™ for funds, or "star rating," is calculated for managed products with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive five stars, the next 22.5% receive four stars, the next 35% receive three stars, the next 22.5% receive two stars, and the bottom 10% receive one star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three- and five-year Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns. Past performance, rankings and ratings are no guarantee of future results. The % of Peer Group Beaten is the funds' total-return percentile rank compared to all funds within the same Morningstar Category and is subject to change each month. Regarding ranking of funds, 1 = Best. Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. For the most recent month-end and standardized performance, click here.

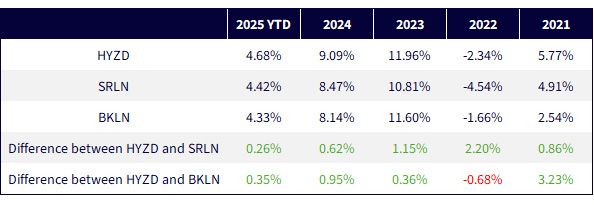

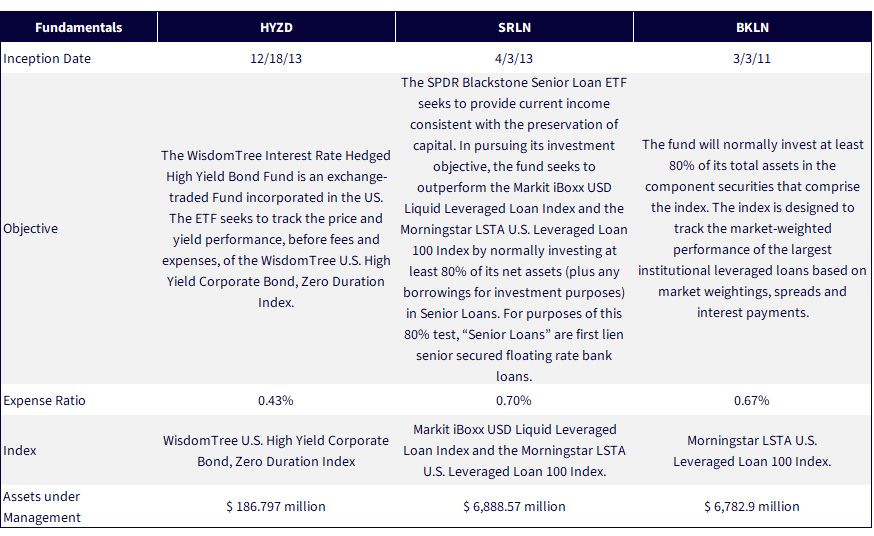

Recently we have received many questions about how HYZD stacks up compared to the senior loan category, mainly represented by the two biggest funds in the category: SPDR Blackstone Senior Loan ETF (SLRN) and Invesco Senior Loan ETF (BLKN). We could dedicate a whole blog post on why HYZD has outperformed these two Goliaths in the senior loan fund category; but the goal of this piece is to look at these categories fundamentally and explain why we believe interest rate hedged high-yield bonds and HYZD represent a stronger substitute than senior loans in fixed income portfolios.

Sources: WisdomTree, Bloomberg, as of 8/31/25. Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. For the most recent month-end and standardized performance, click the respective ticker: HYZD, SLRN, BKLN.

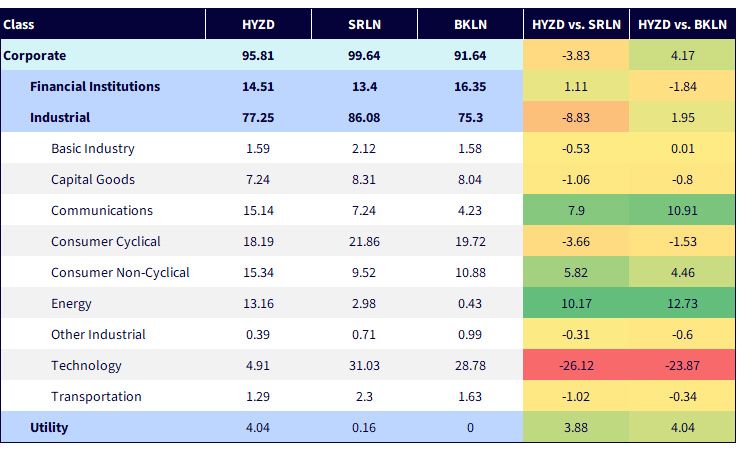

One of the biggest differences between HYZD and senior loan funds is diversification. Senior loan funds like SRLN and BKLN often concentrate their holdings in just a few sectors, most notably Information Technology. That approach can work well when those sectors are strong, but it also leaves investors more exposed if the trend is reversed. HYZD takes a more diversified approach, choosing from the wider high-yield bond market and spreading exposure across different sectors. This broader diversification helps balance risk and supports more consistent, risk-adjusted returns without leaning too heavily on a small set of sectors.

Sources: WisdomTree, Bloomberg, as of 08/31/25.

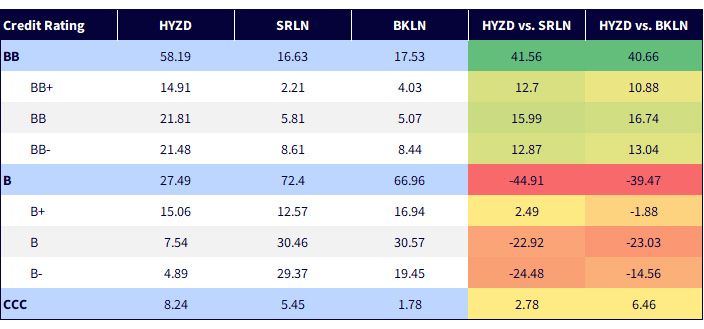

Beyond sector diversification, HYZD also stands out compared to senior loans when looked at through the credit quality lens. The Fund focuses on the higher-quality issuers of the high-yield market, reducing default and drawdown risk while still offering competitive yields. By contrast, senior loan funds tend to concentrate more heavily in lower-rated, cyclical issuers that are more vulnerable during periods of slowdown or distress. In today's mixed economic environment, we believe it's most prudent for fixed income investors to have a quality bias in their portfolios, especially in asset classes that will suffer most if the tide turns.

Sources: WisdomTree, Bloomberg, as of 8/31/25.

Liquidity often becomes a critical factor when markets become volatile. The short-term high-yield bond market is larger and more liquid than the senior loan market. Senior loans, on the other hand, can see liquidity dry up in risk-off environments, making it harder to adjust positions without absorbing losses.

Ever since the Fed started their rate hike cycle back in 2022, senior loans have been attractive for the floating rate nature of their coupons, which helped cushion the impact of rising interest rates. But with rates now elevated, and the Fed in the middle of their easing cycle, we believe this advantage will dissipate, making it harder for senior loans to offer compelling income compared to the rest of high-yield market.

When compared to senior loan strategies like SRLN and BKLN, HYZD stands out in several important ways. It offers broader sector diversification, a higher-quality credit profile, better liquidity and is more aligned with today's shifting interest rate environment. Add to that a strong track record of outperformance across multiple time periods, and the WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD) makes a compelling case. For investors looking to maintain income while adding quality bias to their fixed income portfolios, we believe HYZD presents a smarter alternative to traditional senior loan funds.

Sources: WisdomTree, State Street, Invesco, as of 09/16/25.

You cannot invest directly in an index.

Material must be preceded or accompanied by a prospectus. Click the respective ticker to view the fund prospectus: HYZD, SRLN, BKLN.

HYZD: There are risks associated with investing, including the possible loss of principal. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. The Fund seeks to mitigate interest rate risk by taking short positions in U.S. Treasuries (or futures providing exposure to U.S. Treasuries), but there is no guarantee this will be achieved. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions.

Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. The Fund may engage in “short sale” transactions where losses may be exaggerated, potentially losing more money than the actual cost of the investment and the third party to the short sale may fail to honor its contract terms, causing a loss to the Fund. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

SRLN: Investments in senior loans are subject to credit risk and general investment risk. Credit risk refers to the possibility that the borrower of a senior loan will be unable and/or unwilling to make timely interest payments and/or repay the principal on its obligation. Default in the payment of interest or principal on a senior loan will result in a reduction in the value of the senior loan and consequently a reduction in the value of the portfolio’s investments and a potential decrease in the net asset value (NAV) of the portfolio.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates rise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing in high yield fixed income securities, otherwise known as “junk bonds,” is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

BKLN: There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The fund’s return may not match the return of the underlying index. The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the fund.

Most senior loans are made to corporations with below investment-grade credit ratings and are subject to significant credit, valuation and liquidity risk. The value of the collateral securing a loan may not be sufficient to cover the amount owed, may be found invalid or may be used to pay other outstanding obligations of the borrower under applicable law. There is also the risk that the collateral may be difficult to liquidate, or that a majority of the collateral may be illiquid.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

Non-investment-grade securities may be subject to greater price volatility due to specific corporate developments, interest-rate sensitivity, negative perceptions of the market, adverse economic and competitive industry conditions and decreased market liquidity.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The fund is non-diversified and may experience greater volatility than a more diversified investment.

Reinvestment risk is the risk that a bond’s cash flows (coupon income and principal repayment) will be reinvested at an interest rate below that on the original bond.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Interest Rate Hedged High Yield Bond Fund

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.