GDE

Efficient Gold Plus Equity Strategy Fund

Published June 18, 2025

Global Head of Research

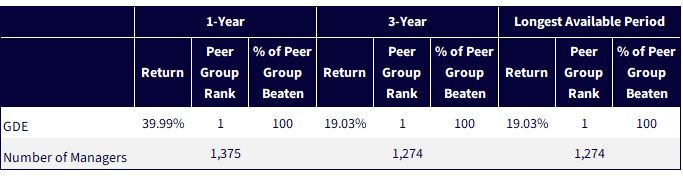

In the vast universe of investment strategies, only a select few ever ascend to the absolute top of their peer group—and even fewer stay there. In the highly competitive Morningstar U.S Large Blend category, which includes titans of index tracking, smart beta innovations and active strategies alike, ranking #1 over both one-year and three-year horizons is statistically exceptional. It's not just about relative outperformance—it's a signal that something unique is happening under the hood. Out of more than 1,000 contenders,1 the WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) has achieved precisely that. This isn't a lucky streak or a niche anomaly; it's a deliberate convergence of two of the most potent return-generating forces in the current market regime: U.S. large-cap equity momentum and gold's renaissance as both an inflation hedge and portfolio diversifier.

What makes GDE's ascent particularly compelling is that it doesn't rely on complicated security selection, precise timing or opaque models. The equity sleeve is straightforward: a market capitalization-weighted allocation to the 500 largest U.S. stocks—a segment that has led the equity markets, with mega-cap resilience dominating the performance tables. But layered onto this equity core is the innovation. GDE overlays gold futures exposure in a capital-efficient structure, using only $10 of collateral for every $90 in gold futures while maintaining full equity exposure. In effect, GDE deploys a 90/90 structure: $90 in equities, $90 in gold and $10 in cash collateral, made possible through the futures market. This layered approach allows investors to hold dual exposures without requiring dual capital commitments.2

The period during which GDE climbed to the top of the Morningstar charts coincided with two reinforcing macro trends: the dominance of large-cap U.S. equities and a breakout in gold prices. The strategy didn't just benefit from exposure—it benefited from efficient exposure. Gold futures have surged amid declining real yields, central bank accumulation and heightened geopolitical risk.3 Meanwhile, U.S. large caps have defied pessimism and rate volatility to deliver strong returns, especially as investors concentrated on a narrow band of mega-cap winners. GDE captured both themes with precision, translating macro-level alignment into benchmark-beating performance. It's rare to be number one.

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 6/13/25, but showing returns for the period ended 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance.The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

As we noted, Morningstar places GDE within the broader U.S. Large Blend category. The leveraged exposure to gold futures is a very unique proposition.

Adding gold futures exposure on top of traditional equities is driving these results, but being the literal number one fund in any period in such a broad category is, in our opinion, an impressive feat.

Source: Morningstar Direct. The longest available period is from 4/1/22 to 3/31/25, based on 4/1/22 being the closest next-month start relative to GDE's inception on 3/17/22. For completeness, we show it, but it is the same period as the "3-Year" in this particular case. Morningstar ratings are based on risk-adjusted return. Past performance is not indicative of future results.

As with any investment strategy, the elements that have driven GDE's standout performance—surging gold prices and strong large-cap equity returns—are not static. Gold, in particular, is notorious for episodes of volatility and long stretches of subdued returns. GDE's embedded leverage, while essential to its capital efficiency, magnifies both gains and losses, introducing risk during periods when either equities or gold underperform. Moreover, the psychological barrier of "I've already missed it" can paralyze investor decision-making, especially when looking at charts already steeped in green. But history shows that gold's price drivers—real interest rates, currency shifts and geopolitical uncertainty—rarely move in a straight line. The environment that pushed gold to new highs in recent quarters may evolve, but it is far from resolved.

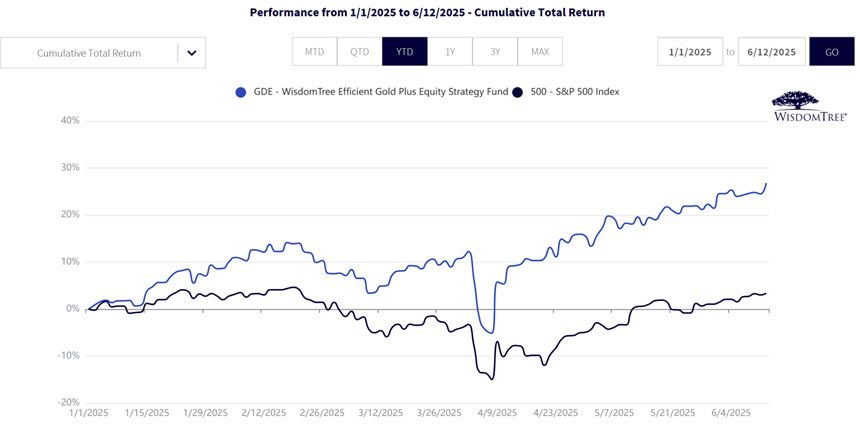

Much has been made of 2025's volatility in equity markets so far—we believe many wouldn't realize how GDE has been able to navigate this to a significant advantage with the efficient gold exposure.

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 6/13/25, but showing returns for the period ended 6/12/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

One of the most significant advantages of GDE is that it helps investors sidestep a false dilemma: choosing between equity participation and gold exposure. Many investors are understandably hesitant to shift capital into gold after a strong run, fearing they'll miss out on the next leg higher in equities—especially with mega-cap stocks continuing to drive benchmark returns. But GDE's structure offers a solution that reframes the conversation: It doesn't require an investor to give up equity exposure to gain access to gold. Instead, through capital-efficient layering of gold futures atop a traditional equity core, GDE enables simultaneous participation in both trends. This dual exposure can be a game-changer for portfolio construction—preserving upside potential while embedding diversification. While no strategy is without risk, and past performance is no guarantee of future results, GDE offers a thoughtful way to expand opportunity sets without diluting core equity allocations. It's not about timing gold—it's about holding both, smartly.

1 Shown in figure 1b. Source: Morningstar Direct. The longest available period is from April 1, 2022, to March 31, 2025, based on April 1, 2022, being the closest next-month start relative to GDE’s inception on March 17, 2022. For completeness, we show it, but it is the same period as the “3-Year,” in this particular case. Past performance is not indicative of future results.

2 This fund does not hold physical gold.

3 Sources: “How lower rates and central bank demand are fueling the gold rally,” Forbes, 3/25/24; “What does the record price of gold tell us about risk perceptions in financial markets?,” European Central Bank, 5/25. https://www.ecb.europa.eu/press/financial-stability-publications/fsr/focus/2025/html/ecb.fsrbox202505_02~7f616fcd3f.en.html

You cannot invest directly in an index.

There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Morningstar, Inc., 2019. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance, rankings and ratings are no guarantee of future results. The % of Peer Group Beaten is the fund’s total-return percentile rank compared to all funds within the same Morningstar Category and is subject to change each month. Regarding ranking of funds, 1 = Best.

Efficient Gold Plus Equity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.