IHDG

International Hedged Quality Dividend Growth Fund

Published June 3, 2025

Equity Strategist

The decline of the U.S. dollar (USD) in 2025 is startling global markets and prompting many investors to question the efficacy of currency hedging their international investments.

However, historical context is sorely needed.

Through May 14, the Bloomberg U.S. Dollar Index (BBDXY) is down 5.9% year-to-date, a much steeper print than the 2.7% decline registered in the first quarter. The magnitude of the sell-off is certainly generating headlines in financial media, with no shortage of culprits to blame: economic effects from the White House’s tariff agenda, fiscal deficit concerns, the end of “American exceptionalism” or a combination of all three.

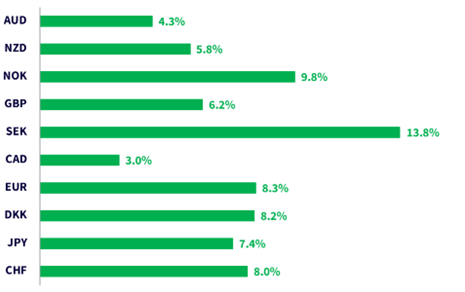

Meanwhile, foreign currencies are enjoying a reprieve from the relative weakness and strong-dollar environment that characterized the past few years. Each currency within the G10 basket has appreciated versus the dollar year-to-date, with most stronger by at least 6%.

Sources: WisdomTree, FactSet, as of 5/14/25. Past performance is not indicative of future results. CAD = Canadian dollar, NOK = Norwegian krone, NZD = New Zealand dollar, AUD = Australian dollar, GBP = Great British pound, SEK = Swedish krona, DKK = Danish krone, EUR = euro, CHF = Swiss franc, JPY = Japanese yen

However, we think the dollar’s swoon in 2025 is more palatable than investors realize, and talk of impending “dollar doom” is just a fancy phrase of fearmongering. Most importantly, it should not discourage asset allocations or long-term investment strategies that utilize currency hedges for international positions.

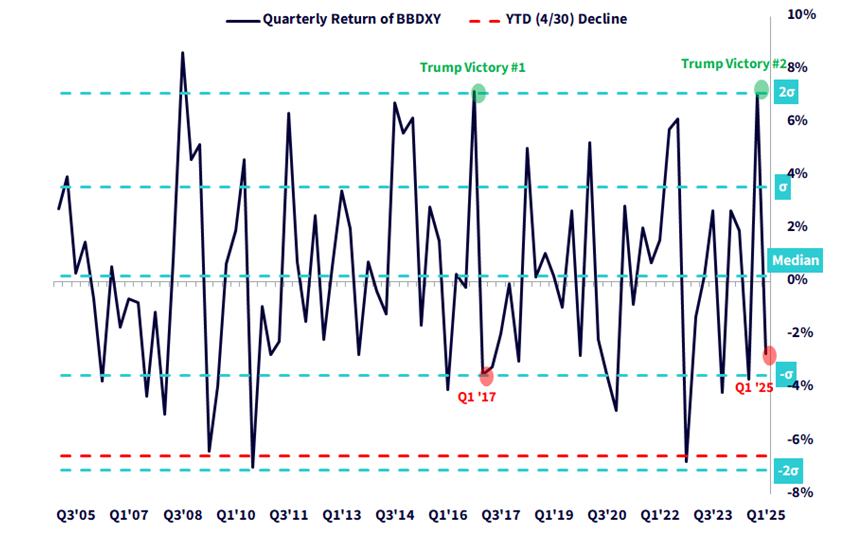

During Q1, the dollar fell 2.7%, which was approximately a one-standard-deviation downside move when observing quarterly returns dating back to the Index’s 2004 inception.

But this followed a historic 7.1% gain in Q4 2024, inspired by markets’ anticipation, and the eventual confirmation, of a Trump presidential victory and a Republican sweep of both Congressional houses in the 2024 election. The late-2024 rally was a two-standard-deviation event, and one of only three such positive moves in the 81 observations since Q1 2005.

Sources: WisdomTree, Bloomberg, as of 4/30/25. Past performance is not indicative of future results. You cannot invest directly in an index.

The previous two-standard-deviation positive jolt coincided with Trump’s first victory in Q4 2016. The dollar’s response was nearly identical to the post-2024 election reaction, gaining 7.15%.

The numerical magnitude of its appreciation in both cases is likely a coincidence, but it suggests a possible pattern in the market’s election response that may dampen concerns about the dollar trajectory going forward.

In the subsequent quarter, Q1 2017, the dollar dipped 3.5%, a one-standard-deviation change comparable to this year’s decline and indicative of markets’ reconciliation of pre-election expectations with post-inauguration policy effects.

Based on this, investors might have expected dollar volatility to settle down as Trump eased into the presidency, but “Liberation Day” worsened the decline. The dollar plummeted 4% in April, bringing the cumulative year-to-date nosedive to 6.6%, which is just shy of a two-standard-deviation event if we extend Q1’s return one extra month.

But once again, context is key.

The dollar’s plunge year-to-date seems like a necessary reversal of post-election enthusiasm. Since September 2024, the dollar index is actually up by 6 basis points (bps), marking a near-complete roundtrip from its post-election high.

In other words, the dollar is essentially back to where it was half a year ago, despite an eventful, circuitous adventure along the way. If an investor knew nothing about how it returned to this point, such a negligible move over a short timeframe wouldn’t provoke concern.

In the context of portfolio construction, being indifferent about the dollar’s movements over the past seven months is equivalent to avoiding currency volatility, which is the backbone of our preference for currency-hedged international exposures.

However, many investors are now doubting foreign currency hedges amid the dollar rout and questioning their efficacy precisely when their long-term advantages are needed most.

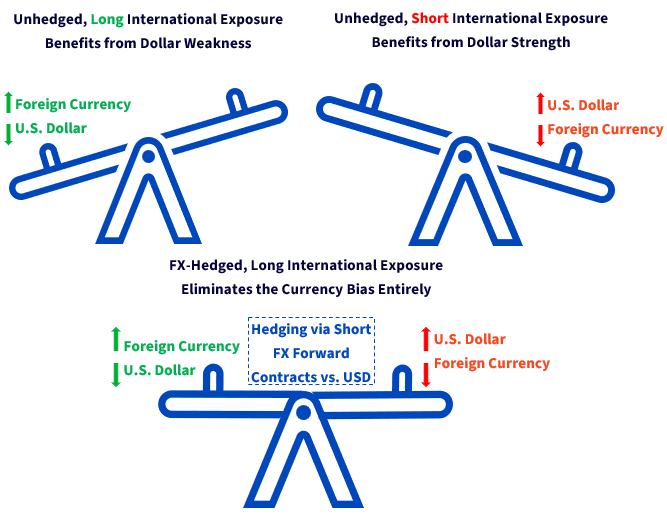

This is because many are misunderstanding a currency hedge’s true intent. They’re not meant to reverse unhedged long foreign currency exposures in favor of net long dollar exposure. Instead, they offset, or eliminate, the unhedged long foreign currency exposure so that currency does not influence performance altogether.

Visually, the relationships look like this:

Source: WisdomTree

In our view, the primary motivation for currency hedging should be a desire to reduce volatility from an international allocation because, as evinced by the dollar’s roundtrip over the past seven months, currency exposure consistently adds volatility.

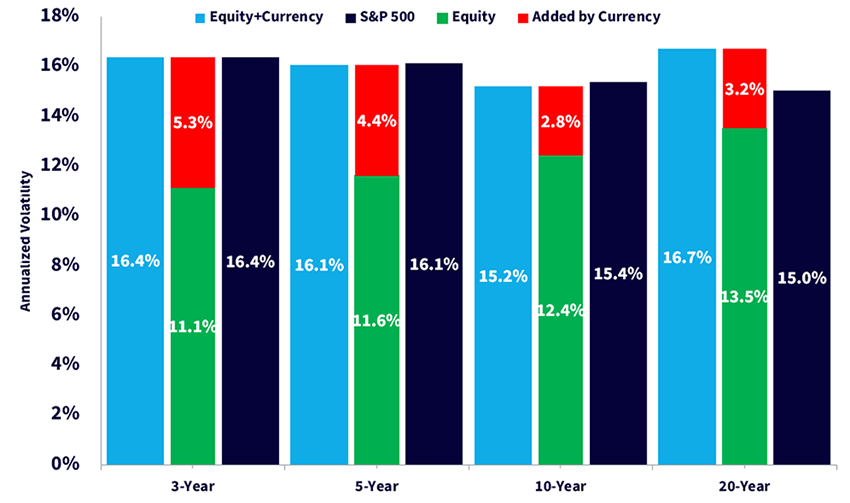

Sources: WisdomTree, MSCI, S&P, as of 4/30/25. Equity + Currency represented by the net total returns of the MSCI EAFE (USD) Index. Equity represented by the net total returns of the MSCI EAFE (Local) Index. Currency represented by the difference between the net total returns of the MSCI EAFE (USD) and MSCI EAFE (Local) Indexes.

Over the most recent medium- and long-term investment horizons, currency exposure routinely added about 3%–5% incremental volatility to a broad, unhedged international equity allocation, which dragged total volatility close to that of the S&P 500. Over the 20-year interval, currency’s volatility addition made an international allocation riskier than overall U.S. markets.

The S&P 500 universally outperformed the MSCI EAFE1 over each of the above periods, so the incremental volatility attributable to currency exposure further reduced the diversification benefit from an international equity allocation.

In other words, unhedged international exposure provided much less than what it was intended to provide. A U.S. investor likely would have benefited from eschewing international equities in favor of U.S. markets, from a risk-adjusted return standpoint.

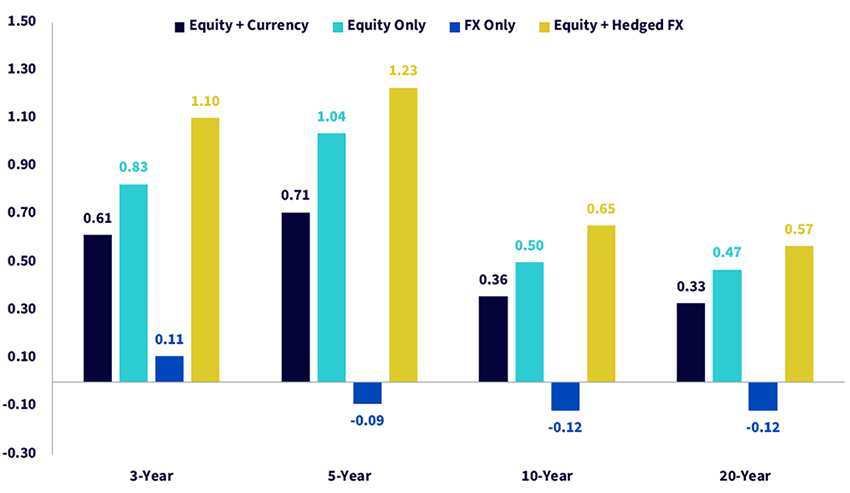

Hedging foreign currency made international equity markets undeniably more attractive. The risk-adjusted returns from a currency-hedged MSCI EAFE equity allocation were unanimously higher than an equivalent, unhedged position over each period.

Sources: WisdomTree, MSCI, S&P, as of 4/30/25. Equity + Currency represented by the net total returns of the MSCI EAFE (USD) Index. Equity represented by the net total returns of the MSCI EAFE (Local) Index. Currency represented by the difference between the net total returns of the MSCI EAFE (USD) and MSCI EAFE (Local) Indexes. Equity + Hedged FX represented by the net total returns of the MSCI EAFE (100% USD-Hedged) Index. Past performance is not indicative of future results. You cannot invest directly in an index.

The improvement is explained by the volatility reduction illustrated above, where the currency-hedged investor only endures the volatility attributable to the underlying equities themselves, bypassing currency’s contribution altogether.

But hedging simultaneously offered return improvements in the post-pandemic environment as well due to interest rate carry. Because prevailing interest rates in the U.S. have consistently exceeded those offered by central banks in the EAFE region, currency-hedged investors have been able to earn an additional 1.7% annualized return, on average, for most of the past decade.

Both influences made currency-hedged international equity exposure superior to unhedged allocations over the medium- and long-term periods. Since many investors allocate internationally for long-term diversification benefits anyway, we think hedging’s innate advantages are too important to disregard and silly to doubt, especially today.

For those considering allocations, WisdomTree offers a suite of currency-hedged ETFs that may introduce a valuable, currency risk-attentive strategy to developed international equity markets.

1Source: Bloomberg, as of 4/30/25. Using net total returns in USD terms. Past performance is not indicative of future results. You cannot invest directly in an index.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as the risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile, may be less liquid than other securities and can be more sensitive to the effects of varied economic conditions. As these Funds can have a high concentration in certain issuers, they may be adversely impacted by changes affecting those issuers. Due to the investment strategies of these Funds, they may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease doing so at any time. Please read each Fund’s prospectus for specific details regarding its risk profile.

DXJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance.

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.