DGRS

U.S. SmallCap Quality Dividend Growth Fund

Published April 28, 2025

Head of Equity Strategy

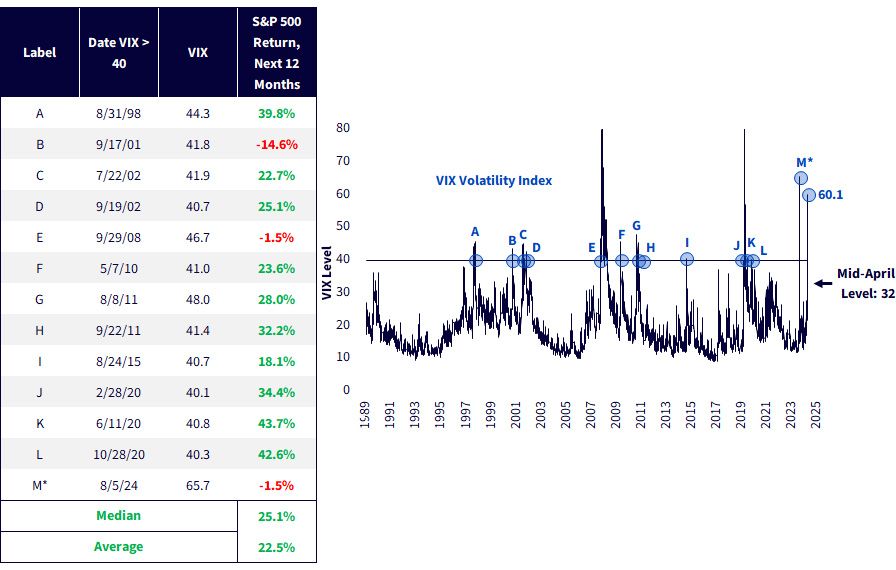

With the Chicago Board Options Exchange's CBOE Volatility Index (VIX) back at 32, investors may overlook a critical event from April: the index's surge to 60 during peak market panic. Historically, such volatility has coincided with systemic shocks, including 9/11, the global financial crisis (GFC) and the COVID-19 outbreak. A VIX reading above 40 has often marked market bottoms, with subsequent 12-month equity gains in many cases. Figure 1 illustrates that most past volatility spikes were followed by positive returns.

Source: Refinitiv, as of 4/7/25. S&P 500 Total Returns. Highlighted spikes above 40 must occur at least one month after the previous volatility spike. *Asterisk on 5/5/24, as it hit 65.7 intraday but closed lower than 40, at 38.7. One year has not yet passed since that specific event. You cannot directly invest in an index.

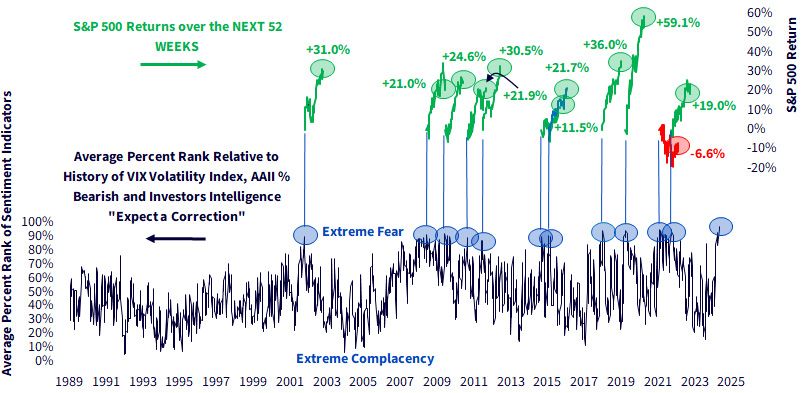

Figure 2 averages three fear gauges: the VIX, AAII bearish sentiment and the Investors Intelligence "stock market correction" anticipators. Averaging their historical percentiles yields a unified fear gauge.

Today's reading is the highest on record. This is in a sample set that includes September 11, plus all those banks and insurers dying in the GFC, Covid and so on.

In nearly every prior instance of comparable fear, stocks rose a year later.

Source: Refinitiv, 1/5/1990–4/16/2025. One bull market is colored blue to separate it from another nearby bull market. The gauge captures the average percent rank of the VIX volatility index, AAII "bearish" respondents and I.I. respondents who expect a stock market correction. You cannot directly invest in an index.

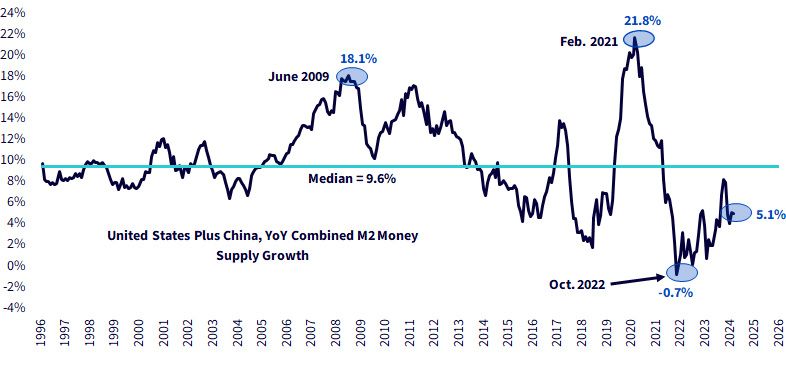

The stagflation narrative needs perspective. Combined U.S. and Chinese M2 is up just +5.1%, well below the 9.6% norm (figure 3). Unlike 2022's inflation, driven by aggressive quantitative easing, today we're deep into a tightening cycle. Despite widespread stagflation fears, reality suggests modest growth with fading inflation pressures.

Sources: Refinitiv, Federal Reserve, PBoC, as of February 2025; YoY change US M2 plus China M2 (in USD).

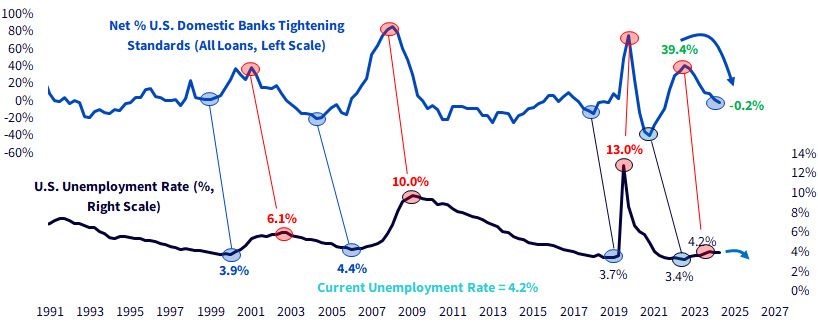

Right now, the narrative is that unemployment is heading higher. But if banks maintain or further ease lending standards, as they have for seven consecutive quarters, it could bolster labor market stability (figure 4). That trend could reverse with the public's newfound skittishness—but it's no certainty.

Source: Fed Senior Loan Officer Survey as of Q1/2025. Unemployment rate as of March 2025.

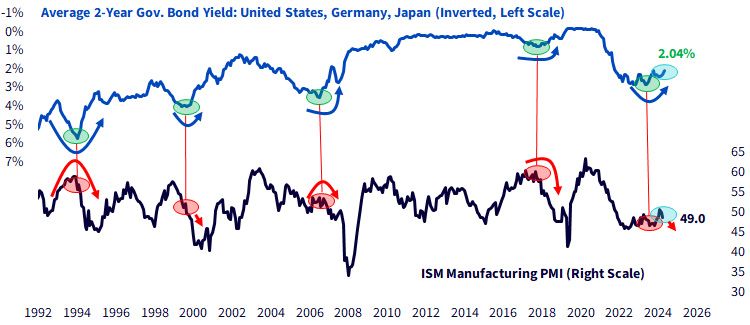

Figure 5 is nerve-racking. It shows an average of the two-year government bond yields from the U.S., Germany and Japan. The yield curve can give a clue that the system is facing forthcoming industrial weakness. Historically, yield-curve inflections have anticipated drops in the ISM Manufacturing PMI, currently at a soft 49.0.

Sources: Refinitiv, ISM, as of March 2025 for PMI and 4/17/25 for bond yields.

The preceding charts form the basis for portfolio action. I've put together a few investor types, along with ETFs that may work for each profile.

You sold into weakness. Now, the market has stabilized, but re-entering feels premature. For this investor, a strategy like the WisdomTree Equity Premium Fund (WTPI) may offer a measured way back in. WTPI implements a put-writing overlay, which has historically dampened downside volatility while generating options income.

Use case: rebuilding exposure gradually; targeting reduced drawdown risk amid tariff wars.

If you believe tariff tensions will ease—or simply that the correction has priced in too much fear—then small caps are a high-beta rebound play. The WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS) has felt the full brunt of bears' selling this year. A relief rally could manifest in this heavily punished corner of the market.

If your outlook is cautious but you're not abandoning equities, our dividend-focused value strategies have historically held up in down markets. Over the decade ending March 2025, the S&P 500 Value Index captured 99% of the market's downside—basically one-for-one. But the WisdomTreeHigh Dividend Fund (DHS) posted a down capture of just 82%.

For investors who want to stay in large caps with income support, the WisdomTree U.S. LargeCap Dividend Fund (DLN), offers another defensive profile (with 91% down capture and 86% up capture).

Use case: defensive core allocation; income-focused exposure.

If you believe inflation will persist longer than consensus—and that geopolitical risks will continue to drive gold demand—consider pairing equity and commodity exposures. The WisdomTree Efficient Gold Plus Gold Miners Fund (GDMN) blends physical gold with mining equities in a single wrapper, and it's our top year-to-date performer.

For a broader footprint, the WisdomTree Efficient Gold Plus Equity Fund (GDE) overlays gold exposure on a diversified equity portfolio. Both aim to preserve purchasing power if growth slows while inflation lingers.

Use case: own what's working now.

Notice I didn't mention cash or bonds. The investor types above come from very different starting points—some cautious, some opportunistic, some worried about inflation—but each one is staying in the market. Whether it's WTPI, DGRS, DHS, DLN, GDMN or GDE, the common thread is engagement. I think running for cover is not the play here.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTPI: The Fund will invest in derivatives, including S&P 500 Index put options (“SPX Puts”). Derivative investments can be volatile, and these investments may be less liquid than securities, and more sensitive to the effects of varied economic conditions. The value of the SPX Puts in which the Fund invests is partly based on the volatility used by market participants to price such options (i.e., implied volatility). The options values are partly based on the volatility used by dealers to price such options, so increases in the implied volatility of such options will cause the value of such options to increase, which will result in a corresponding increase in the liabilities of the Fund and a decrease in the Fund’s NAV. Options may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The potential return to the Fund is limited to the amount of option premiums it receives; however, the Fund can potentially lose up to the entire strike price of each option it sells. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs.

DHS/DLN/DGRS: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

GDMN: The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains.

GDE: The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains.

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.