Discounting the D.C. Effect in the Bond Market

Published March 12, 2025

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- The bond market’s early-year narrative of rising yields shifted rapidly as policy uncertainty, changing tariff prospects and federal worker layoffs drove the 10-Year U.S. Treasury yield back to pre-election levels.

- Concerns over federal employment cuts have heightened scrutiny on private payrolls. The February jobs report revealed a healthy labor market but early signs of the “D.C. effect” are impacting federal job numbers.

- While recent bond market rallies reflect investor caution, the next phase of Washington’s fiscal policy—including potential tax cut extensions—could introduce new headwinds for U.S. Treasuries.

One thing we have seen underscored in 2025 is that the bond market can change its mind very quickly, particularly as it relates to policy emanating from Washington, D.C. Following President Trump’s election win, the dominant theme in the U.S. Treasury (UST) arena was that his Administration’s policies would lead to higher budget deficits, increasing UST supply and, ultimately, higher rates for maturities like the 10-Year yield.

Fast-forward to about 50 days into the new federal government setting and the narrative has shifted in a rather visible fashion. Now, the UST market is looking at the uncertainty quotient of changing tariffs combined with the prospect of federal worker layoffs and the 10-Year yield has fallen more than 50 basis points from its mid-January high watermark. It now resides where it was trading prior to Election Day (see below).

Figure 1: U.S. Treasury 10-Year Yield

Source: Bloomberg, as of 3/7/25.

Certain Uncertainty

In terms of potential tariff impacts, the one thing we can be certain of is continued uncertainty. The ultimate impact on the U.S. economy and inflation is still an unknown at this point. However, we may be seeing signs of some effects in the recent merchandise trade data where imports surged. Conventional wisdom appears to be that this increase in goods being brought into the U.S. is due to domestic businesses frontloading imports before the tariffs take hold. If that’s the case, these higher imported goods could end up becoming a build-up in inventories and serve as a somewhat offsetting factor in the real GDP calculation.

Jobs, jobs, jobs

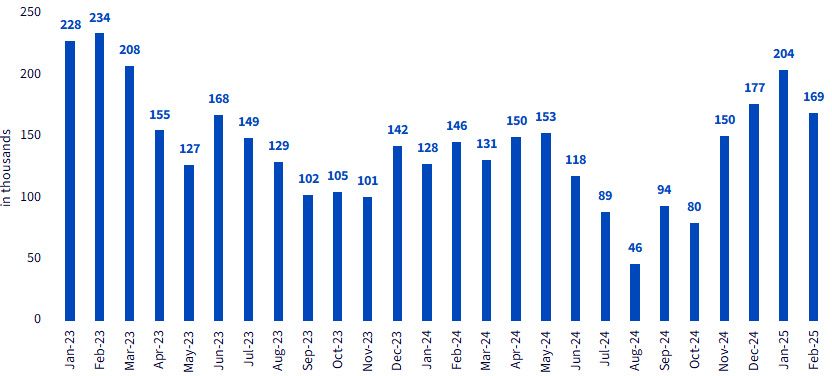

That brings us to perhaps the more pertinent part of the equation: the labor markets. Concerns are mounting in the bond market that a surge in federal government layoffs will not only negatively impact upcoming monthly employment reports, but that there could also be an adverse ripple effect into the private sector. Against this backdrop, in the months ahead, investors may not only focus on the traditional total nonfarm payroll number but also give heightened scrutiny to the private payroll figure.

Figure 2: U.S. Total Private Payrolls, 3-Month Moving Average

Source: Bureau of Labor Statistics, as of 3/7/25.

With that being said, the February jobs report revealed a still relatively healthy labor market setting, but it also began to show signs of the potential “DC effect,” i.e., federal employment. While the gain in total nonfarm payrolls came in relatively close to consensus (+151,000 vs. +160,000, estimated), federal employment did fall by 10,000. However, private payrolls produced a consensus-like gain of +140,000.

Given the current situation, it is also important to focus on how the underlying labor market trend was behaving as we entered into this uncertainty. As the above chart reveals, while the three-month moving average for private payrolls did drop from the prior month’s reading, the level still came in at a relatively good showing of +169,000. In fact, other than the robust performances of early 2023, the current level stands above the majority rate of increases witnessed over the last two years.

Where Does the Bond Market Go from Here?

While it does seem reasonable to dial down real GDP estimates, bond investors are faced with a validation moment in the UST market once again. Future evidence will be needed to support the recent rally in rates, let alone go lower from here. Furthermore, the next phase in the D.C. playbook—extending tax cuts, etc.—may not prove to be very bond market friendly. In other words, it will remain a very fluid situation.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.