Global Central Bank Outlook

Published December 5, 2024

Key Takeaways

- As 2025 approaches, global monetary policies diverge sharply, with the U.S. Fed navigating resilient inflation and labor markets while other central banks cautiously extend their rate-cutting cycles.

- Japan and China present contrasting economic strategies, with Japan focused on profitability and yen stabilization, while China’s low bond yields and limited stimulus measures hint at untapped equity potential.

- Europe faces economic uncertainty, with the ECB easing rates amid fragile growth and Germany’s political upheaval, while the UK’s expansionary budget sparks inflationary risks and complicates the Bank of England’s policy outlook.

Listen to the blog post below:

With the calendar quickly approaching 2025, global investors are confronted with a different landscape compared to 12 months ago. While central bank rate cuts were expected to occur in 2024, the timing and magnitude of what has transpired thus far did not necessarily live up to market expectations in some cases. That being said, the rate-cutting process has begun for a number of central banks, and in all likelihood, there will be a continuation of some sort into the new year.

U.S. Fed Watch

We often talk about how there is no “one size fits all” dynamic in central bank monetary policy, and the U.S. was certainly in no hurry to loosen policy earlier in 2024 when other central banks were cutting. Then, in September 2024, when the U.S. Federal Reserve (Fed) cut interest rates for the first time in more than four years, it went big, chopping rates by 50 basis points (bps) in one swipe. The Fed had been working under the assumption that the economy and labor market had been cooling faster than they previously thought. A drop in bond yields and U.S. dollar depreciation in September indicated the market was expecting an accelerated catch-up by the Fed. However, resilience in economic data and inflationary pressures have led the market to once again revise its view. The Fed cut by only 25 bps in November, and Chairman Powell has been sowing the seeds of doubt about the scale and pace of further moves.

Obviously, monetary policy remains highly data-dependent. Another quarter-point reduction in the Fed Funds Rate seems a likely scenario for the December Federal Open Market Committee (FOMC) meeting, data permitting. But this is where things could get very interesting. If the economic/labor market data continue to show signs of not cooling too much, and inflation gets “sticky” around current levels, a reasonable case scenario could involve the Fed taking a pause to reassess things to begin 2025. That doesn’t necessarily mean the rate-cut cycle would end. However, the policy maker would have already cut rates by 100 bps in this backdrop, so perhaps Powell & Co. “taking stock” could make sense.

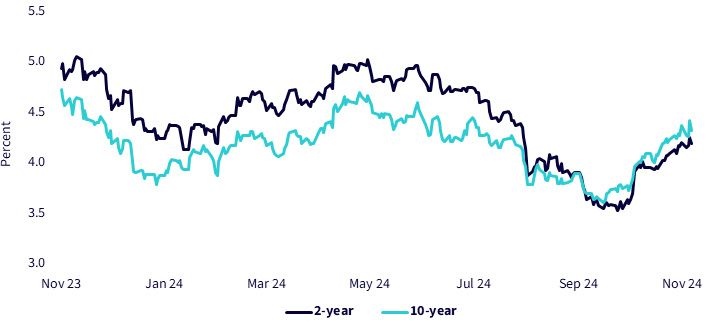

A Post-Election/Post-Fed Look at U.S. Treasuries

Regardless of who won the presidential election, we were expecting U.S. budget deficits to continue rising. In fiscal year (FY) 2024, the deficit came in at $1.8 trillion, or a +8.1% increase higher than FY 2023’s deficit of $1.7 trillion. Higher deficits are funded by higher Treasury issuance, which drives bond yields up. Normally, issuance volume is a secondary or tertiary driver of bond yields, with macro and monetary policy drivers being the primary driver. Trump’s U.S. presidential election win, combined with a “red sweep” with the Republicans controlling both chambers of Congress, paves the way for decisive policy change. This outcome has placed more focus on deficits. Certainly, markets appear to view the red sweep as more pro-growth and inflationary than other outcomes, and thus, bond yields have risen.

Figure 1: U.S. Treasury Yields

Source: Bloomberg, as of 11/8/24. Historical performance is not an indication of future performance, and any investments may go down in value.

We believe market focus will shift back toward macro-economic data and the Fed. Instead of focusing on how high the UST 10-Year yield may be headed, the more pertinent question is whether it can go back down to its mid-September levels. Unless the labor market data collapses, the answer would be “no,” with yields more than likely remaining elevated in the months ahead.

Japan’s Elusive Rate Hikes

The Bank of Japan had been slow-rolling its pace of interest rate hikes while it waited for U.S. election results. Knowing the chemistry between the country’s leaders appears to be an important factor in determining the course of the Japanese economy.

The yen has stabilized after the carry trade blew up in late July and early August. That happened when the market came to the sudden conclusion that the Fed would aggressively cut rates while the Japanese central bank would seemingly do the opposite, an occurrence that sent traders panicking out of their short yen positions. The sudden rush into yen sent the forex pair from Y162 before the comeuppance to levels below Y141 by mid-September. As we write, the exchange rate is Y153, owing to the market’s repricing of the Fed’s 2025 path to something more benign than previous intimations.

There is still plenty of room for an upside valuation rerating for Japanese stocks, if for no other reason than the U.S. stock market’s relentless rise could drag other developed markets along with it. But, for a sustainable move, Japan’s aggregate return on equity (ROE) will need to improve. At 9.0%, it is languishing compared to the U.S.’s 17.8%. The efforts by the Tokyo Stock Exchange to motivate corporations to boost profitability may help.

China: Waiting for the Bazooka

China’s most recent stimulus package, announced a couple of days after Trump’s victory, called for a CNY10 trillion ($1.4tn) package of debt swaps to aid local governments. It was a useful but very narrow form of stimulus, and the market was expecting more. Faced with a threat of 60% tariffs from the U.S., China needs a bazooka, and this policy announcement is insufficient. China may be keeping dry powder aside for when it has actual clarity about trade restrictions under the new administration in 2025.

A series of other stimulus announcements had been made earlier in the year, including initiatives to reduce the down payment requirements on second home purchases, along with general mortgage rate reductions. Critically, the People’s Bank of China (PBoC) also cut banks’ required reserve ratios, an oft-used tactic that we have seen the central bank employ during the country’s bear markets over the course of our careers.

A final note on China. We do not believe the sheer scale of the collapse in the country’s cost of capital is studied enough or fully appreciated in macro circles. As we write, China’s long bond yield has dumped to 2.26% from levels north of 4% during COVID-19. For context, 2.26% is equal to Japan’s 30-year bond quote. This is a new ballgame. With bond yields this low, we believe Chinese equities should get a second look.

Figure 2: 30-Year Government Bond Yields

Source: Refinitiv, as of 11/11/24. Historical performance is not an indication of future performance, and any investments may go down in value.

Europe—Going Soft on Soft Landing

The European Central Bank (ECB) has taken note of the weak recovery of the euro area. It appears to be rushing toward a neutral rate as concerns about economic growth trump inflation fighting. The ECB’s bank lending survey showed some tentative improvements in the lending environment. Banks did not tighten credit standards for the first time in two years, and demand for borrowing is cautiously improving, especially for households. Yet, monetary policy can be a weak tool for managing an economy’s business cycle, especially one with as diverse growth trajectories as the euro area. A weaker euro area could tip the balance toward a slightly softer stance by the ECB; a weaker euro versus the U.S. dollar argues against that. Owing to this, the ECB is likely to lower the deposit rate three more times, by 25 bps each, in the coming months to reach a trough of 2.5% by March 2025.

The prospect of trade protectionism is also weighing on the outlook for the European economy, and Trump’s win is putting that risk into focus.

Trump’s win in the U.S. arguably accelerated the collapse of Germany’s fragile coalition. After Chancellor Olaf Scholz dismissed Finance Minister Lindner, who is also the chairman of the liberal Free Democratic Party (FDP), the coalition is in tatters. Snap elections are likely to be called in mid-January, which will probably take place in March. The snap elections can pave the way for a new start in Germany. This should result in a raft of reforms that will strengthen supply and demand with more room for public investment, lowering of business taxes and trimming of welfare and pension benefits alongside a reasonable immigration policy.

Despite the three-party coalition government experiencing tensions over a stagnant economy, Germany’s DAX Index has continued to outperform broader European peers by 9.2% in 2024. The strong performance can be attributed to specific tailwinds in artificial intelligence (AI) and cloud computing, beneficiaries from the electrification theme and financials.

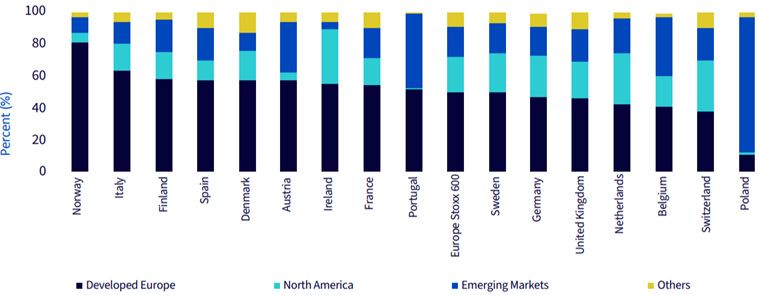

Figure 3: Revenue Exposure by Country—Eurostoxx 600 Index

Sources: Bloomberg, FactSet, WisdomTree as of 6/30/24. Historical performance is not an indication of future performance, and any investments may go down in value.

UK Budget Provides Largest Loosening in Decades

Chancellor Rachel Reeves’ 2024 budget struck a delicate balance between stimulating growth and maintaining fiscal credibility. While expansionary measures initially offered a temporary boost to markets, new borrowing projections triggered a sharp rise in 10-year gilt yields, which reached their highest level in a year of 4.47%. The increase in spending announced in the budget caused the Office for Budget Responsibility (OBR) to double its forecast of annual growth in real government spending over the next two years. By front-loading spending while increasing tax revenue gradually, the government will provide a significant boost to growth in 2025 and add to inflationary pressure. However, as National Insurance tax bills rise, companies are likely to feel the pressure, slowing hiring and investment and dampening economic growth. The Bank of England’s (BOE’s) rate path has become more complicated, and we could see it ending its cutting cycle after just three more cuts at 4.25% in Q2 2025.

The New Era of Central Bank Gold Buying Continues

Central banks have become big buyers of gold in recent years. In 2022 and 2023, central banks bought the equivalent of 29% of mined gold in those years. The watershed moment came in 2022 when the Russia-Ukraine war started and G7 countries “weaponized” their currencies, which left a bitter taste in many central banks’ mouths. Instead of accumulating these traditional fiat reserve currencies, they now look to gold. The lack of viable alternative currencies outside of the G7 favors gold as a pseudo-currency that has no central bank controlling its supply or status as legal tender.

Central bank or “official sector” gold buying in 2022 was at a record high and more than double the average between 2012 and 2021. Central bank purchases in 2023 declined by only a fraction and remained more than double the average between 2012 and 2021. The first half of 2024 saw the largest H1 central bank gold buying on record. Buying in Q3 2024 cooled, but mainly as a result of China not reporting any purchases. It’s debatable whether China has actually stopped buying or is just not reporting its purchases. Outside of China, central bank gold buying is broad, and surveys of central banks point to continued strong demand.

For deeper insight, read the latest edition of The Global Edge Report here.

Important Information Related to this Article

Nitesh Shah and Anneka Gupta are employees of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree, Inc.

About the contributors

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.