Could It Be Time for a Turnaround in Cloud Computing?

Published September 3, 2024

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- In 2024, the cloud computing sector, especially Software-as-a-Service (SaaS) companies, faced significant challenges due to the U.S. Federal Reserve’s interest rate policies, resulting in negative returns for many more speculative companies.

- The WisdomTree Cloud Computing Fund (WCLD) experienced both positive and negative catalysts from 2020 to 2024, including the COVID-19 pandemic, inflation and the rise of AI, which influenced the Fund’s returns.

- Despite disappointing actual returns for software companies in 2024, AI could be a catalyst for cloud companies. The BVP Cloud 100 list highlighted strong potential in the AI, fintech and productivity sectors.

Do you remember the last time you put a disc into your computer to install new software? My laptop hasn’t had a disc drive going back several years.

Software has shifted from being a physical thing purchased from a store to being a subscription run completely over the internet.

Software business models are attractive due to their scalability and resulting high profit margins. The next copy of software available to the marginal user is not cost-intensive, and there is no physical manufacturing involved. Of course, the economics could change if we think of scaling to the next 100 million users with the need for data centers and servers.

In 2019, WisdomTree launched the WisdomTree Cloud Computing Fund (WCLD) to focus predominantly on the specific, relatively high-growth companies within the Software-as-a-Service (SaaS) space.1 This strategy focuses on those SaaS companies that are seeking to deliver their software to enterprise customers.

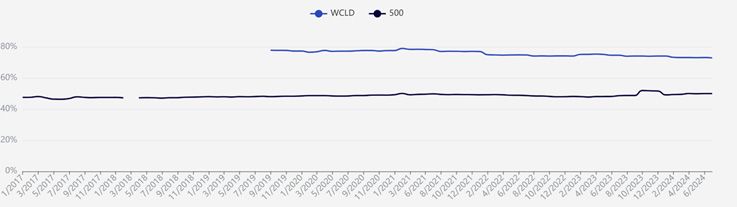

Demonstrating the attractive economics of this business, we compare the gross margin of WCLD to a major benchmark, in this case, the S&P 500 Index, and can see the dramatic differential and high margins in WCLD.

Figure 1: Gross Margin of WCLD (Software Companies) vs. the S&P 500 Index (500)

Source: WisdomTree’s Fund Compare software tool from within its PATH suite of tools, as of 7/31/24. Past performance is not indicative

of future results.

Yet, the actual returns for software companies in 2024 have disappointed. In evaluating where we are, let’s recap the experience of recent years within WCLD, which tells us how SaaS companies have been doing, returns-wise, in different environments:

- 2020: This year was characterized by the COVID-19 pandemic and the “work-from-home” trend kicking off. Companies like Zoom Video Communications saw incredible increases in revenues due to the sudden value being placed on the ability to do high-quality virtual meetings and presentations. Many cloud companies ensure that certain tasks can be performed as long as there is an internet connection, and the pandemic created an instant one-time boost in demand for this sort of thing.

- 2021: 2021 was a year of “liquidity,” and the impacts of printing money and lowering interest rates to zero really coalesced during this year. As the year progressed, higher inflation became more and more visible, and higher interest rates and contractionary monetary policy began to be anticipated. This extreme, juxtaposed with the prior year’s extreme of greater-than-100% returns, contributed to a very rough 2021 full year for WCLD's returns.

- 2022: This was a year when U.S. equities2 and bonds3 both delivered negative returns—historic for asset allocators in the negative sense since history has not seen many times when this occurred. There are a lot of speculative companies in WCLD that are not yet carrying their revenues through their income statements to indicate positive profits at the bottom line—many are continuing to make various growth-oriented investments. As interest rates sharply rose, these speculative stocks did not do well.

- 2023: The primary topic of this year was AI, and the primary companies that delivered returns connected to that story were some of the world’s largest—the so-called “Magnificent 7.”4 WCLD rallied into the end of 2023 due to expectations that the U.S. Federal Reserve had contained inflation successfully and would have to start lowering interest rates quickly to start 2024.

- 2024: The market, and the world, has been waiting on the U.S. Federal Reserve for basically the first eight months of the year. The misplaced expectation of a quick series of interest rate cuts had to be “corrected” with negative returns from more speculative companies—like those within WCLD. If interest rate cuts do come, it’s possible that these companies could see their share prices respond.

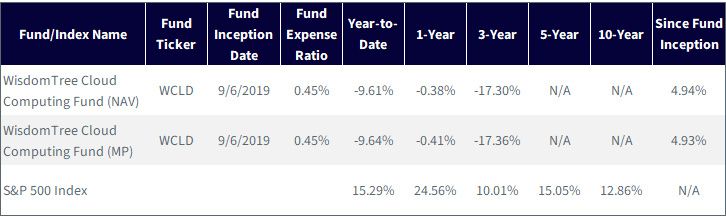

If one takes the full figure 2b into account, starting at the end of 2019 and carrying through to the end of July 2024, one will see an annualized return of 4.7% for WCLD as compared to 14.2% for the S&P 500 Index. Even with the greater-than-100% return, being cut in half in 2022 was by far the critical driver of this result.

AI could be a significant catalyst for these businesses. The pandemic was a catalyst for a massive amount of software adoption—adoption that might have naturally played out over years played out over months. If AI increases or improves what software providers can do, maybe this is a future growth catalyst that could contribute to further equity returns.

Figure 2a: Standardized Performance

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 6/30/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results.

Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may

be worth more or less than their original cost. Current performance may be lower or higher than the performance data

quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses,

click here.

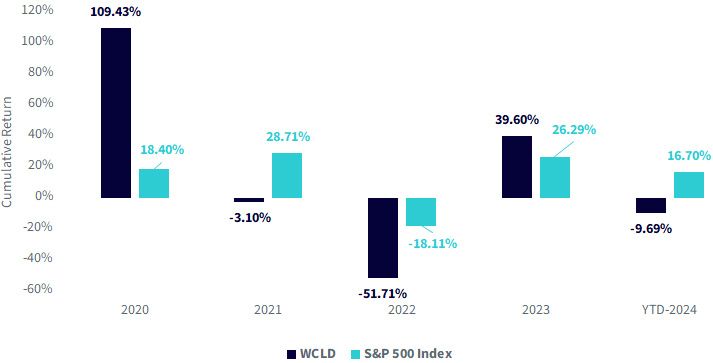

Figure 2b: WCLD’s Journey through the Calendar Years

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, for the period 12/31/19–7/31/24. NAV

denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of

future results. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when

redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the

performance data quoted. For the most recent month-end and standardized performance and to download the respective

Fund prospectuses, click here.

The BVP Cloud 100 List Is Out!

The BVP Cloud 100 list is something we have been following in earnest since 2019—WCLD was launched during the 2019 event.5

WCLD comprises a basket of publicly listed equity investments, and the BVP Cloud 100 comprises the 100 most significant private cloud companies—but the largest and most impactful private companies may foreshadow what we see over the coming years in the public equity space.

There have been nine versions so far of the Cloud 100 list. Figure 3 indicates summary information of this journey back to 2016:

- The list value at C100 (Cloud 100)—we have seen that go from $99 billion to $820 billion in 2024. This is the total value across all 100 companies, so we have seen this figure getting to a point where we are thinking about that 10x type of increase.

- Possibly the starkest statistic in the figure regards the number of exits. Eighty in 2016. Three in 2023. We don’t have indications that 2024 will be a big year on this front—but it is only about eight months in.

Figure 3: The BVP Cloud 100 List Highlights across Time (2016 to 2024)

Source: Bessemer Venture Partners.

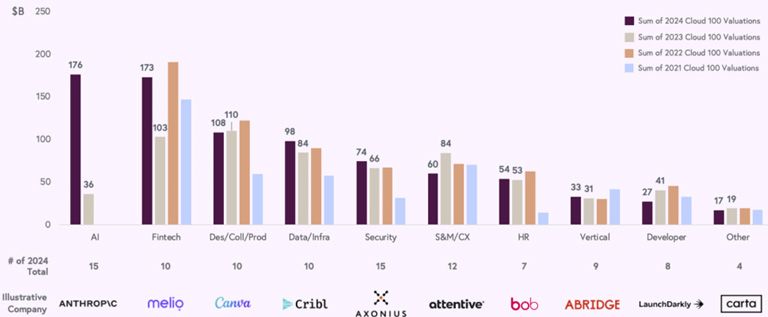

We saw in figure 3 that OpenAI has attained the top position now for two years in a row (2023 and 2024). There is some time yet to compete with Stripe’s five out of nine years in the top spot, but we see in figure 4 that as a category—AI—we have a massive overall valuation of $176 billion.

What’s more interesting about this “AI” category is that it only started being included in 2023, so in 2022, it was not even being tracked or on the radar of the Cloud 100.

Figure 4: Summary of Highlights from 2024’s BVP Cloud 100 List

Source: Bessemer Venture Partners.

In figure 5, we see that three overall functional groups of companies in the Cloud 100 achieved an aggregate value greater than $100 billion.

- AI: $176 billion

- Fintech: $173 billion

- Design/Collaboration/Productivity: $108 billion

Figure 5: It’s Useful to Know Where We See the Biggest Private Software Companies

Source: Bessemer Venture Partners.

It’s funny to take a step back and consider, as someone following developments in technology markets, the last time I heard the term “unicorn.” This was the term used for a company in the private market that achieved a valuation of $1 billion or more. A “decacorn” would be a company in the private market that achieved a valuation of $10 billion or more.

The Cloud 100 companies have a value of $820 billion, an average value of $8.2 billion per company.

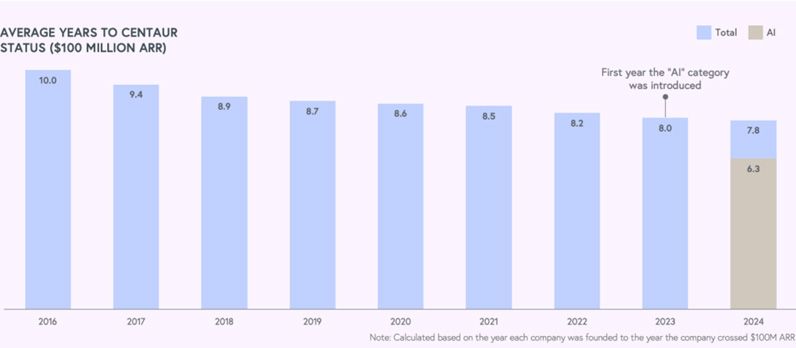

BVP, a few years ago, shifted the thinking from the idea of the “unicorn” valuation to the “centaur”—companies that are able to achieve $100 million or more in annual recurring revenues (ARR). This means that they are convincing customers to sign up and pay them this amount on an ongoing basis—far more impressive than simply raising money.

What’s interesting—and figure 6 only allows us to look at one year—is that AI companies are taking an average of 6.3 years to hit centaur status. The general company in the Cloud 100 is taking 7.8 years. With cloud companies, speeding up the trajectory to get to major revenue milestones is significant.

Figure 6: How Long Until “Centaur” Status?

Source: Bessemer Venture Partners.

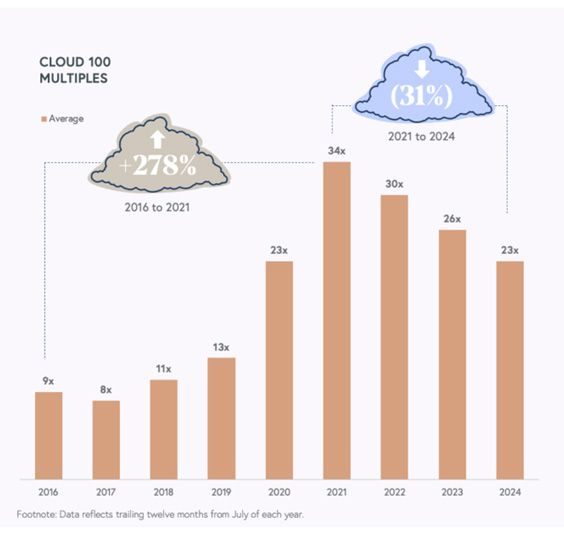

Finally, within software, it does make sense to think about “valuation, valuation, valuation.” It’s a good measure of inherent risk. When interest rates were zero, valuations peaked at a 34x ARR multiple within the Cloud 100.

In 2024, even with the increase in aggregate value to $820 billion—it was $113 billion in 2021—the valuation has gone down to 23x, which is a drop of 31% relative to 2021’s figure.

Figure 7: Evolution of Cloud 100 Multiples

Source: Bessemer Venture Partners.

Conclusion: Software Is Here to Stay

Especially if we consider the “application economy” in our smartphones, there are few things that we use as much as software. BVP has also pointed out in its 2024 State of the Cloud report that we must all remember that the large language models that feel as though they are in almost every AI headline in 2024 are very expensive to develop, train and maintain. Companies that build software on top of these models, using them as a foundation, could have a much more compelling economic proposition—similar to how companies building data centers have different economic profiles than those using the compute resources.

For those with a longer time horizon, software could be quite interesting.

1 WCLD is designed to track the total return performance of the BVP Nasdaq Emerging Cloud Index, before fees and expenses. This Index has as its main criteria for inclusion the generation of more than 50% of revenues from cloud activities focused on enterprise customers and at least 15% year-over-year revenue growth.

2 Refers to the S&P 500 Index.

3 Refers to the Bloomberg U.S. Aggregate Index.

4 Refers to Alphabet, Amazon, Apple, Microsoft, Meta Platforms, Nvidia and Tesla.

5 Source: D’Onofrio, Mary, et al. “The Cloud 100 Benchmarks Report 2024.” Bessemer Venture Partners, 8/6/24, www.bvp.com/atlas/the-cloud-100-benchmarks-report.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. The Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

THE INFORMATION SET FORTH IN THE BVP NASDAQ EMERGING CLOUD INDEX IS NOT INTENDED TO BE, AND SHALL NOT BE REGARDED OR CONSTRUED AS, A RECOMMENDATION FOR A TRANSACTION OR INVESTMENT OR FINANCIAL, TAX, INVESTMENT OR OTHER ADVICE OF ANY KIND BY BESSEMER VENTURE PARTNERS. BESSEMER VENTURE PARTNERS DOES NOT PROVIDE INVESTMENT ADVICE TO WISDOM TREE OR THE FUND, IS NOT AN INVESTMENT ADVISER TO THE FUND AND IS NOT RESPONSIBLE FOR THE PERFORMANCE OF THE FUND. THE FUND IS NOT ISSUED, SPONSORED, ENDORSED OR PROMOTED BY BESSEMER VENTURE PARTNERS. BESSEMER VENTURE PARTNERS MAKES NO WARRANTY OR REPRESENTATION REGARDING THE QUALITY, ACCURACY OR COMPLETENESS OF THE BVP NASDAQ EMERGING CLOUD INDEX, INDEX VALUES OR ANY INDEX RELATED DATA INCLUDED HEREIN, PROVIDED HEREWITH OR DERIVED THEREFROM AND ASSUMES NO LIABILITY IN CONNECTION WITH ITS USE. BESSEMER VENTURE PARTNERS AND/OR POOLED INVESTMENT VEHICLES WHICH IT MANAGES, AND INDIVIDUALS AND ENTITIES AFFILIATED WITH SUCH VEHICLES, MAY PURCHASE, SELL OR HOLD SECURITIES OF ISSUERS THAT ARE CONSTITUENTS OF THE BVP NASDAQ EMERGING CLOUD INDEX FROM TIME TO TIME AND AT ANY TIME, INCLUDING IN ADVANCE OF OR FOLLOWING AN ISSUER BEING ADDED TO OR REMOVED FROM THE BVP NASDAQ EMERGING CLOUD INDEX.

Nasdaq® and the BVP Nasdaq Emerging Cloud Index are registered trademarks and service marks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by WisdomTree. The Fund has not been passed on by the Corporations as to its legality or suitability. The Fund is not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE FUND.

You cannot invest directly in an index.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.