DDWM

Dynamic International Equity Fund

Published July 25, 2024

Director of Modern Alpha

At WisdomTree, we offer numerous suites of Funds. In this blog post, I will focus on two particular suites: one that is dynamically hedged and another that is not hedged.

The only difference between the Funds in each pair is the dynamic currency hedge, allowing for an easy evaluation of the net impact of currency hedging.

Dynamic currency hedging has reduced international portfolio risk while adding value on non-hedged equity portfolios.

Since 2016, DDWM has added 2% annually over DWM, as it benefited from adapting its hedge during a stronger dollar period for much of the last few years.

Because the U.S. dollar has been strong, it has been difficult to beat a 100% hedged portfolio. However, dynamically hedged DDWM, with a performance of 8.3% and risk of 12.7% since 2016, has been able to beat a 50% hedged portfolio.

The current dynamic hedging strategy has five components, with a broad market currency trend indicator accounting for 50% of the weight and the other four components (carry, cross asset, low vol and momentum) equal weighted across the remaining 50%.

Since 2023, every component has added some value, with carry and low volatility signals adding the most.

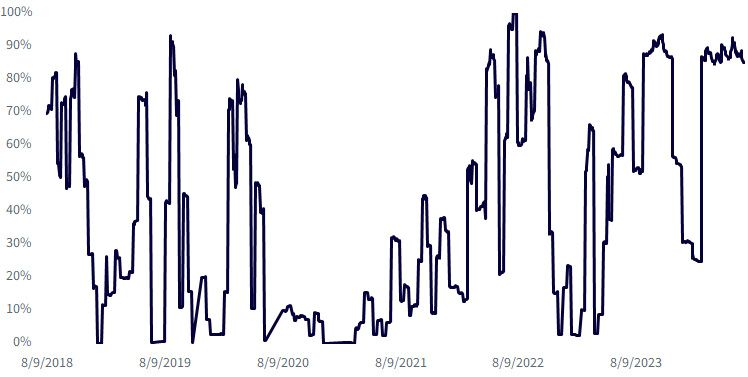

In July, we rebalanced both our developed and emerging markets currency models. Specifically, the hedge for the developed market decreased to about 20%. This change was primarily influenced by the two momentum components of the strategy: the broad trend and cross-sectional momentum, which together account for 62.5% of the weight. As previously mentioned, the increased momentum weight in the new developed market strategy since 2023 has led to more frequent adjustments in hedge ratios.

Sources: WisdomTree, FactSet, Refinitiv 1/06/16-7/10/24. Past performance is not indicative of future results.

In July, the currency strategy for the WisdomTree Emerging Markets Multifactor Fund (EMMF) remains similar to June. We are closely monitoring whether the strategy’s signal regarding the potential weakening of the dollar is limited to developed markets.

Sources: WisdomTree, FactSet, Refinitiv 8/9/18–7/10/24. Past performance is not indicative of future results.

In summary, we maintain our belief that a factor-based dynamic currency strategy can mitigate volatility in international portfolios while potentially enhancing long-term performance.

There are risks associated with investing, including the possible loss of principal.

Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development, which may result in greater share price volatility. Investments in derivatives to obtain a dynamic currency hedge exposure can be volatile, less liquid than other securities, and more sensitive to varied economic conditions, and may not perform as intended. Dividends are not guaranteed, and a company currently paying dividends may cease at any time. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from third parties, which may not perform as intended. Funds that invest in securities included in, or representative of, an Index do not attempt to outperform the Index or take defensive positions in declining markets. Investing involves risk, including possible loss of principal. Investments in non-U.S. securities involve additional political, regulatory and economic risks.

Specific additional risks for EMMF include emerging markets risk, which involves risks relating to political, economic or regulatory conditions not associated with U.S. securities or more developed international markets. The Fund’s investment process is heavily dependent on quantitative models that may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Director of Modern Alpha

Liqian Ren, Ph.D., joined WisdomTree as Director of Modern Alpha in 2018. She leads WisdomTree’s quantitative investment capabilities and serves as a thought leader for WisdomTree’s Modern Alpha® approach. Liqian was previously at Vanguard, where she worked for 12 years, most recently as a portfolio manager in the Quantitative Equity Group managing Vanguard’s active funds and conducting research on factor strategies. Prior to joining Vanguard, she was an associate economist at the Federal Reserve Bank of Chicago. Liqian received her bachelor’s degree in Computer Science from Peking University in Beijing, her master’s in Economics from Indiana University—Purdue University Indianapolis, and her MBA and Ph.D. in Economics from the University of Chicago Booth School of Business. Liqian co-hosts a podcast on China and Asian markets with Jeremy Schwartz, WisdomTree’s Global Head of Research, and she is a co-host on the Wharton Business Radio program Behind the Markets on SiriusXM 132.