The Costco Economy

Published June 14, 2024

Samuel Rines

Macro Strategist, Model Portfolios

Key Takeaways

- Both Costco and Ross Stores are experiencing increased foot traffic and higher sales of previously less popular products, indicating a strong and resilient U.S. consumer.

- The shift in consumer behavior toward buying more discretionary items is attributed to the deceleration of inflation, according to Costco management.

- Constellation Brands, including its Modelo beer brand, is also not seeing any issues with the U.S. consumer and is investing in capacity to meet the demand.

Earnings season never really ends. It is a slow, steady drip of useful—sometimes conflicting—data. But listening closely can be powerful for uncovering both positive and negative trends. For example, American Airlines signaling a weaker-than-expected summer should be taken with a grain of Boeing. Norwegian Cruise Lines is not seeing a problem with its travelers. Not every headline should be taken as a sign. It takes a bit of digging.

When it comes to top-notch operators, Costco is up there with the best of them. The company has a rather wide view of the consumer. From food to furniture, Costco sells it. What did it have to say about the health of the consumer?

Source: Costco.

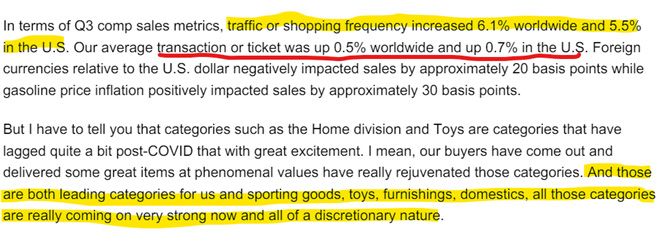

For Costco, there is little to no worry about the health of the consumer. The retailer’s envied foot traffic? Strong. The categories that have been weak in the post-pandemic period? Those were the leading categories for Costco. That does not align with the narrative of a slowing, struggling consumer. And it should not be readily dismissed, either.

Partly, the shift in consumer behavior—according to Costco management—is due to the deceleration of inflation. With less inflation pressure came a shift in consumer behavior back toward buying more of other categories. While specific to the experience of Costco, the data points should not be dismissed. Not only is the U.S. consumer alive and well, it is buying the more discretionary stuff.

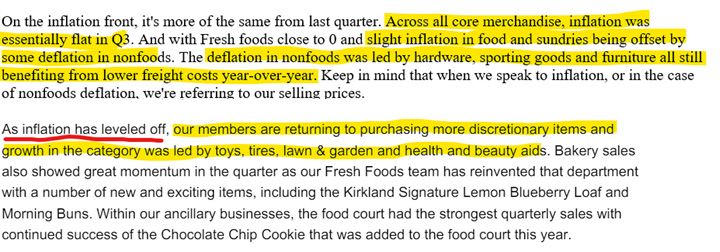

Source: Costco.

But surely this is a Costco-specific phenomenon? No, it is not.

Source: Ross Stores.

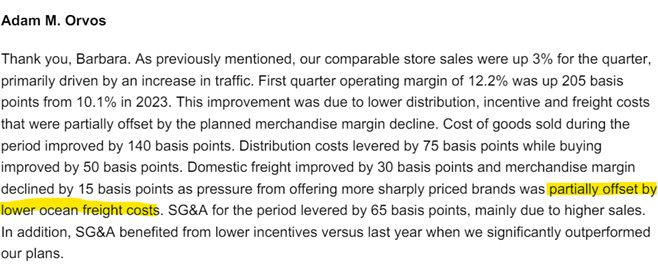

Ross Stores called out better foot traffic as well. And it sold more “sharply priced” products—that is code for “expensive.” The consumer is shopping more (foot traffic) and buying stuff that was shunned for the past several quarters. That is a meaningful pushback to the narrative of a potentially problematic U.S. consumer.

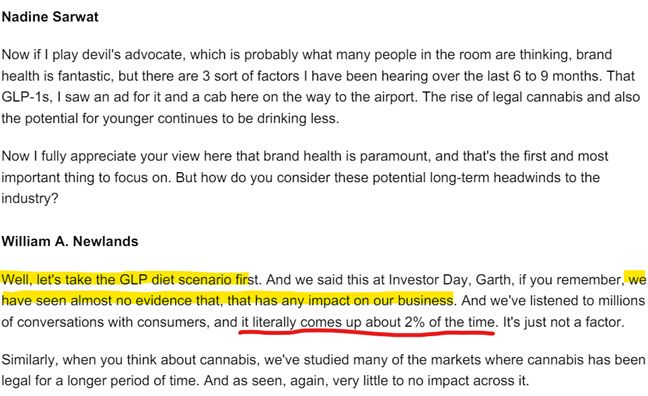

Then, there is commentary from Constellation Brands. Its Modelo beer brand is the #1 brand in the U.S., and the commentary around the outlook was similar to Costco’s. The consumer? No issues there.

Source: Constellation Brands.

There are certainly headwinds, though. The rise of GLP-1s could be an issue for beer consumption. After the meteoric success of weight loss drugs, many of the staples companies were viewed as at risk. But that might be overplayed for the beer category.

Source: Constellation Brands.

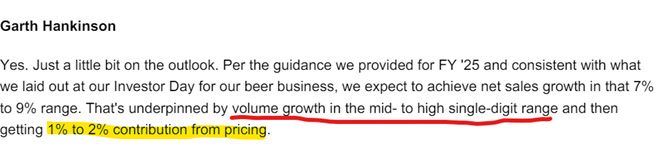

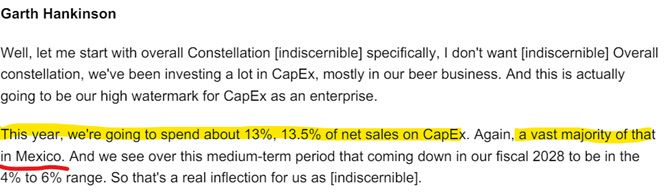

In fact, Modelo and Constellation’s broader beer business has been so successful that it is playing catch-up with its capital expenditures. Where is that capital being invested? Mexico. Again, that is more signal than noise. And it is being done in size.

Source: Constellation Brands.

Why does any of this matter? Because it is the reality of the economy, not a sentiment about the direction. Costco is seeing prices “level off” and the consumer begin to shift spending habits. Both Costco and Ross Stores are seeing foot traffic increase. Constellation is not seeing a consumer slowdown and is investing in capacity to keep up with the demand. None of that is a “maybe.” All of that is the reality of the U.S. consumer. Yes, the consumer sentiment numbers have been horrid. But what the surveys say and what the consumer is doing are two wildly different things.

Welcome to the Costco Economy.

Categories

Related articles

About the contributor

Samuel Rines

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.