The Prices Don’t Feel Right: Unraveling the Inflation Perception

Published June 10, 2024

Macro Strategist, Model Portfolios

Key Takeaways

- Consumers are experiencing the impact of rising inflation, particularly in the grocery sector, leading to a shift in consumer sentiment and the need to reassess budgets.

- Major retailers like Target and Walgreens are addressing consumer concerns by announcing price cuts, aiming to break the perception that prices only go up.

- The perception of lower prices has a powerful effect on consumer sentiment, but for now, many consumers still feel that prices are not right.

Inflation is not fun. And—for the past 30 years—it has largely been a non-issue for consumers. That dynamic has changed. The relevant question is whether this is something persistent and meaningful or simply a fleeting feeling.

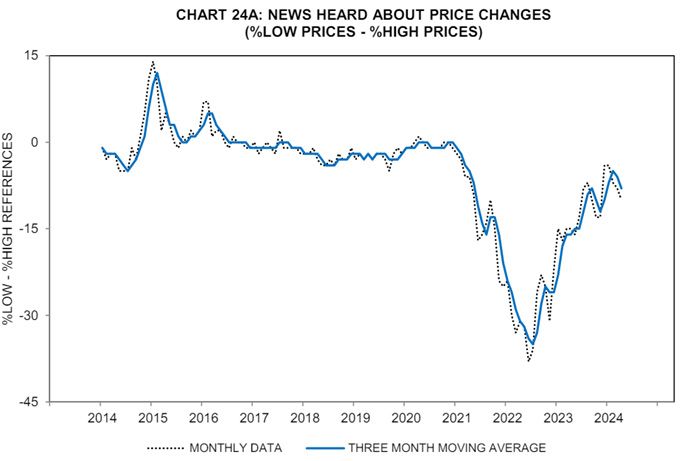

Source: University of Michigan Consumer Sentiment Survey. The chart is simply how many survey respondents “heard” about

lower prices versus higher prices with readings above 0 indicating prices are lower and below 0 indicating prices higher.

This is where some extrapolation is worthwhile. There should be little doubt the price hikes of 2022–2023 were problematic for consumers. They noticed. Volumes for the major grocery store aisle companies fell, and over the past few quarters many announced plans to regain their lost volumes. Now, there is a different narrative. First, it was Target announcing price cuts. Then it was Walgreens. These will not be the last.

And these announcements matter. Sure, they are likely to drive some incremental foot traffic. But, more importantly, the announcements are critical to breaking the mentality that “prices only go up.” If you are the Federal Open Market Committee (FOMC), that is welcome news. Maybe—finally—the inflation cycle is breaking in the parts that can be controlled. The FOMC is not going to break the inflation coming through the insurance channel. That is regulated and sticky, beyond the reach of interest rates. The FOMC breaking inflation at the grocery store is a victory it can relish.

Consumers do not like having to redo their budgets. An underappreciated tailwind for the U.S. consumer for the past 70 years was the declining cost of food relative to discretionary income. Less budget spent on necessities meant more budget spent on other things. And that meant a boom for truly discretionary spending.

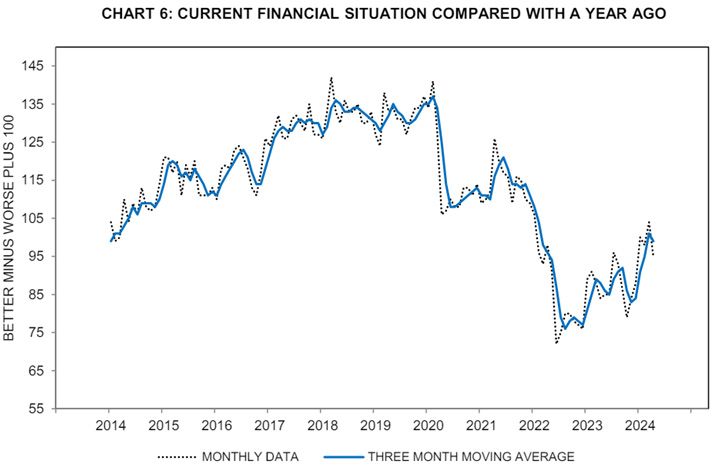

Source: University of Michigan Consumer Sentiment Survey. The chart asks respondents whether their financial situation is better or

worse than a year ago, takes the difference between the answers better or worse, and then adds 100 to it. It is designed to garner an idea

of how consumers “feel” about the economy.

That is not the current situation. Like nearly every economic theory and dataset, Covid and the resulting oddities challenged or broke many of the traditional empirical relationships. The invasion of Ukraine did not help matters. Consumer sentiment data was not spared in the resulting model fractures. How can the U.S. consumer feel so bad when wages are moving higher, jobs are plentiful and the economy is growing? It is the first time in a couple generations that buying groceries is consuming a more significant share of disposable income.

That does not feel great.

There is an odd justification to the “economy is good” and the “economy is not good” argument. And it hinges on the “feels” of the consumer. One of the most noticeable things for the consumer? The grocery bill. The recent announcements by a few major retailers should not be ignored as a catalyst for consumer sentiment. The perception of lower prices is a powerful thing. But, for the time being, the prices don’t feel right.

Categories

About the contributor

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.