WCLD

Cloud Computing Fund

Published June 6, 2024

Global Head of Research

Within WisdomTree’s suite of thematic equity strategies, both the WisdomTree Cybersecurity Fund (WCBR) and WisdomTree Cloud Computing Fund (WCLD) are tracking indexes that focus largely on software-as-a-service (SaaS) companies. There is an overall feeling of concern as we reach the halfway mark in 2024, as we are receiving questions from investors and seeing a range of articles discussing the slowing growth rates in these types of stocks.

In what follows, we combine a sense of recent history with some data that we can pull in from our Fund Comparison software, available through the WisdomTree website.

For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: WCBR and WCLD.

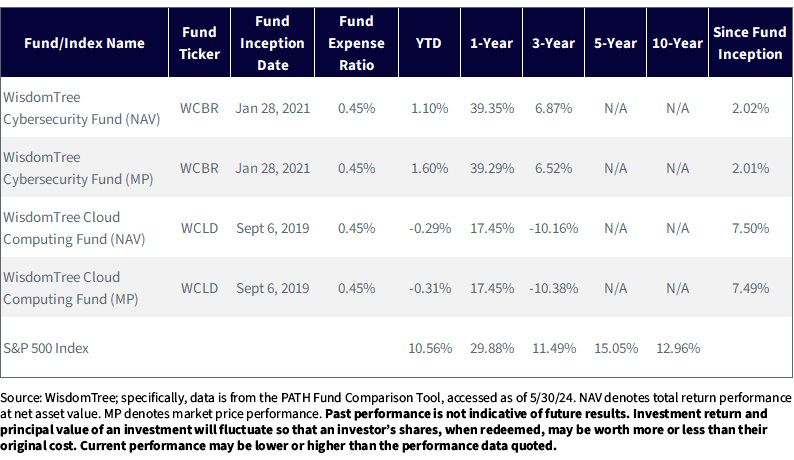

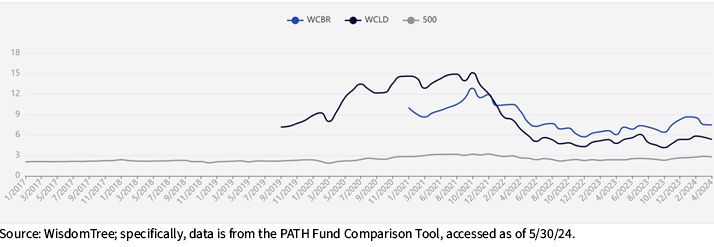

The Fund Comparison tool allows one to see, quite quickly, a range of summary information. What is immediately noticeable is a quantification of the so-called SaaS return rollercoaster:

There is no way to isolate a singular cause for share prices moving in different ways at different times, but if we step back and think about what has characterized asset price behavior since January 2021, there is one macroeconomic variable that has dominated above all others.

In what follows, we quantify this thinking using illustrations from the Fund Compare tool.

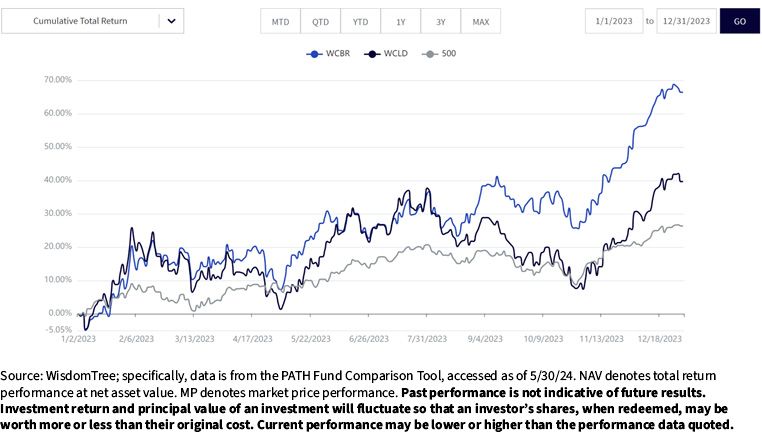

In figure 2, many may not directly remember that WCBR was up almost 70% during 2023 since the character of returns observed in 2024 has been very different. WCLD was only up about 40%. Both of these strategies dramatically outperformed the S&P 500 Index during 2023.

What’s clear is that most of this outperformance came during the last two months of 2023, so we have to zoom in there.

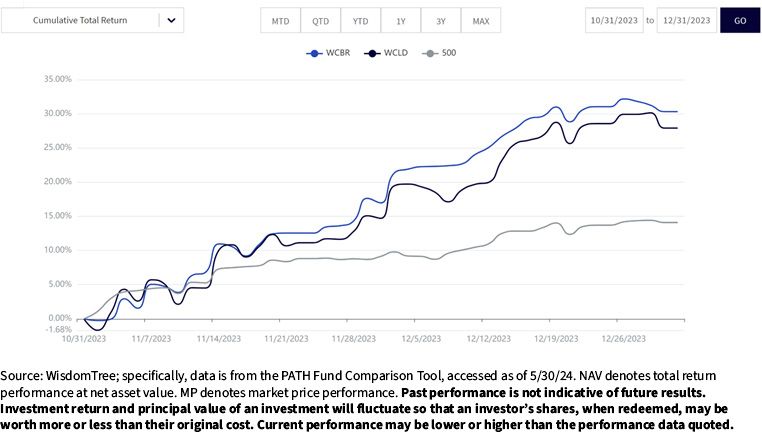

In figure 3, we zoom in on the period from October 31, 2023, to December 31, 2023. Both WCBR and WCLD were up roughly 30%. We cannot say that this move was solely due to expectations of lower interest rates—but we can say that it was a major factor that did create a risk of a mispricing if the path of interest rates was going to stay higher for longer.

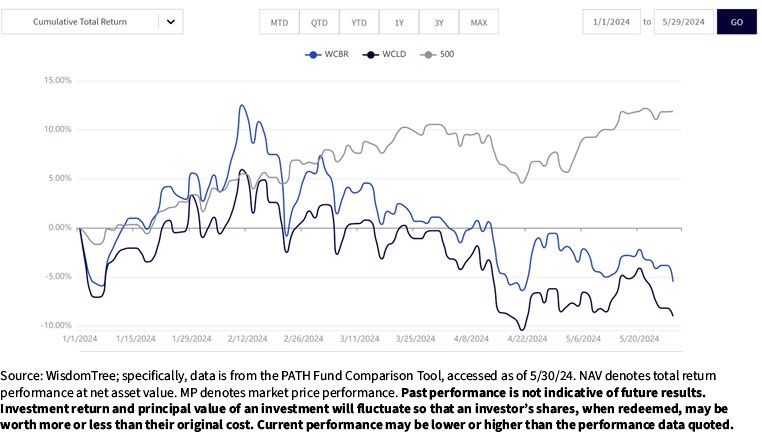

In figure 4, we see the challenge faced by WCBR and WCLD in 2024. Now, most of the underlying constituent companies are growing revenues, year-over-year, above 10%. Some are growing revenues above 20% or even above 30%. But the growth is not accelerating and getting investors anywhere near as excited as they might have been in 2020 or 2021. In short, the growth we are experiencing is not enough to cancel out the negative impact on valuations of higher-for-longer interest rates.2

WCBR and WCLD are underperforming the S&P 500 Index, but we’d caution against benchmarking these rather narrow, high-volatility strategies against such a broad benchmark since we expect the return experience to always be dramatically different.

We believe that, with the higher risk of WCBR and WCLD, the time horizon needs to be extended, and anyone who needs to place a lot of focus on the 2024 performance results in a portfolio may face a significant risk of a negative return contribution from these strategies.

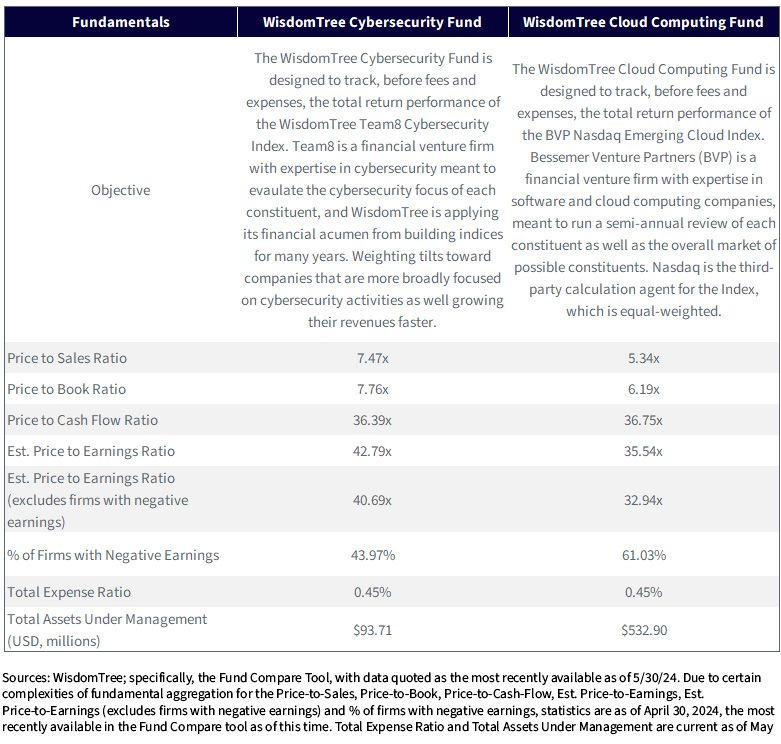

Yes, WCBR and WCLD are also “expensive” from a valuation perspective. But figure 5 shows valuations were significantly higher in 2021 when interest rates were at or near zero. The massive rallies in WCLD and WCBR at the end of 2023 were likely largely driven by interest rate expectations. But, interest rate expectations can change and are independent of company results. Maybe it is accurate to indicate that as we started 2024, these stocks, in many cases, were too expensive IF the U.S. Federal Reserve was not going to cut its policy rate quite quickly.

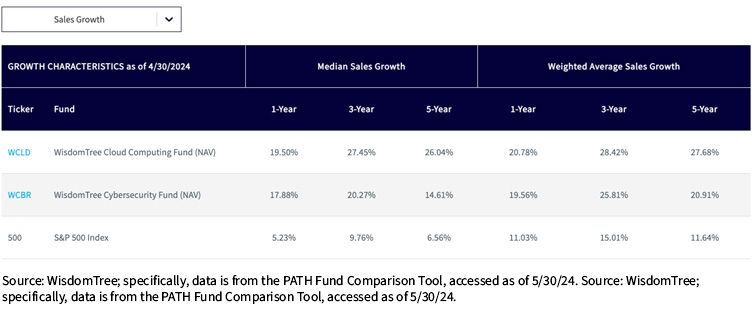

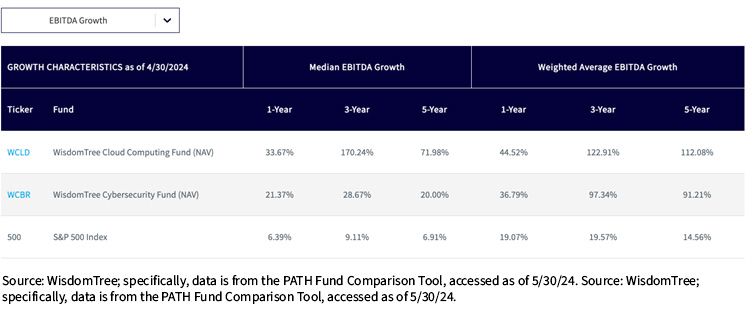

Now, anytime software companies are in focus, we caution investors to look at valuation without looking at growth. Figures 6a and 6b indicate measures of both sales growth and EBITDA3 growth, looked at from both a median and a weighted average basis.

There’s a large divergence between what the world thinks about the themes of cybersecurity and cloud computing through their actions and the share price performance of the companies within WCBR and WCLD.

As we adopt more AI, we will need more cybersecurity since AI is just a tool—it can be used in negative ways and positive ways. The more that different industries adopt, the more they have to secure. We don’t know which cybersecurity companies will be the long-term winners—that is why we like a basket and ETF approach—but the topic is only getting more important.

Nvidia is getting the lion’s share of attention in the technology space. If we think about who is buying the chips, it is the companies that offer the largest public cloud computing infrastructure. The world is spending hundreds of billions of dollars over a period of years to build more compute infrastructure in the cloud than we have ever had. However, we do not know yet which companies will be the long-term winners based on what they are using AI to do.

This divergence from the potential of the theme and the current share price performance signals a time to invest IF one has a time horizon of multiple years. This is because with big technology shifts, very little happens in the earlier years of the transition, but in the later years, the compounding effect of the growth can be quite large. Volatility will likely remain quite high—but if we follow the spending, the world loves and needs both cybersecurity and cloud computing.

1 Specific period of calculation: January 27, 2021, to May 29, 2024.

2 Growth rates are sourced from Bloomberg and represent the year-over-year sales growth of the most recent quarterly financial report of the respective constituents within WCBR or WCLD, available as of May 30, 2024.

3 EBITDA stands for Earnings before Interest, Taxes, Depreciation and Amortization and allows investors to go down the income statement and get closer to a measure of “Operating Earnings.’”

For current holdings, please click the respective ticker: WCLD, WCBR. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal.

WCLD: The Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the Internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WCBR: The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those which are internet related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.