WTAI

Artificial Intelligence and Innovation Fund

Published June 5, 2024

Global Head of Research

Every six months, we undertake a rebalance of the WisdomTree Artificial Intelligence & Innovation Index. We seek to ensure that the Index maintains its exposure to the broad-based AI ecosystem and accounts for anything that has evolved that we can access in publicly listed equity markets.

The WisdomTree Artificial Intelligence & Innovation Fund (WTAI) is designed to track the total return performance of, before fees, the WisdomTree Artificial Intelligence & Innovation Index.

Also, we are seeking to pay attention to diversifying across the “innovation timeline.” What we mean by this—certain innovations have very little certainty with regard to when they may bring something to a company that has the potential to influence business fundamentals, such as revenues, cash flows or profits. Other innovations have a greater probability of impacting these kinds of fundamentals over a shorter time horizon. While we never know anything about the future with certainty, we do not want a full portfolio of deeper technology plays where we cannot credibly build a case that they can bring much, if any, business value within the next two years. It is important to mix longer-term innovation time horizons (like commercially available quantum computing systems and fully personalized medicine) with shorter and more medium-term innovation time horizons (like AI models being run directly on smartphones and laptops).

With all of that said, the two primary theses that influenced this May 2024 rebalance are:

Thesis 1: The big platform companies are important for dispersing AI tools.

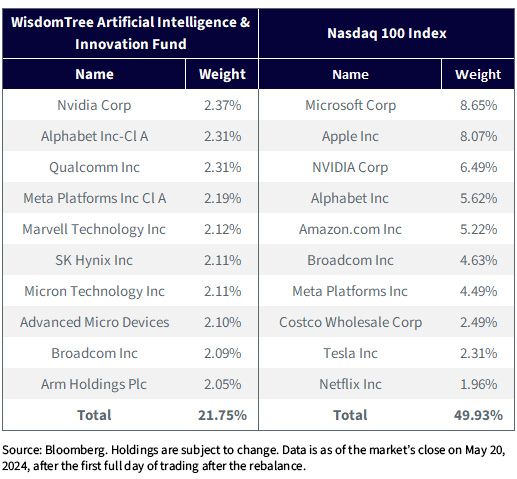

When viewing figure 1, it’s clear that Alphabet and Meta are firmly within the top five positions. Meta is positioning itself as the leader in the “open source” movement. Alphabet just recently, through its I/O conference, announced many new AI functionalities across its different applications.1 As of this writing, people in the U.S. using Chrome may have already noticed a generative AI search summary to their queries. Microsoft, Amazon.com and Apple, while not in the top 10 on this date, also saw initial weights of 2.0% at the exact rebalance, but with small downward share price moves on the first full day of trading, market movement took them below the top 10.

We believe that many people, within the next year or so, will interact with AI through one of these platform players. They have an advantage in that they can deploy AI functionality across a very wide base of users quite quickly.

Thesis 2: Devices capable of directly running AI could be widely available from the second half of 2024 into 2025.

Yusuf Mehdi, who heads up consumer marketing for Microsoft, said the company expects that 50 million AI PCs will be purchased over the next year. At the press event [for Microsoft Build 2024], he said faster AI assistants that run directly on a PC will be “the most compelling reason to upgrade your PC in a long time.”2

It’s also clear in figure 1 that semiconductors have retained their importance—but it’s not all about Nvidia. Nvidia is a central player, but when we see Qualcomm as our second-largest semiconductor position, it’s clear that we are focused on “AI on devices.” In fact, when Microsoft was discussing its newly announced AI PCs, it emphasized partnerships with ARM, AMD and Qualcomm.

We think it is possible that people, through the second half of 2024 and into 2025, will get excited about the concept of “AI on devices” and refresh their laptops and smartphones. If we are correct in this thesis, an important step will be Apple’s WWDC event in June 2024, where we expect an array of AI announcements.3 While not yet confirmed, we are excited to see what AI functionality may be in the iPhone 16, expected to come out later in 2024.

When we look at figure 1, we can see, as of the close of May 20, 2024, the weights for the WisdomTree Artificial Intelligence & Innovation Fund (WTAI) and the Nasdaq 100 Index. Many have ridden the AI wave within the Nasdaq 100 Index, starting with the launch of ChatGPT in November 2022. Performance there has been strong.

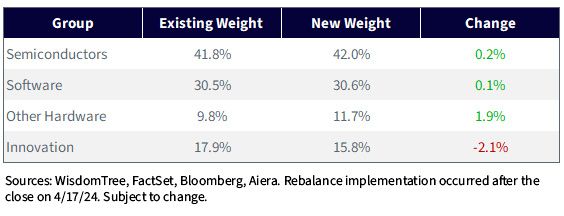

Within the WisdomTree Artificial Intelligence & Innovation Index, we use four groupings to organize the companies within the AI ecosystem. Those are: 1) Semiconductors, 2) Software, 3) Other Hardware and 4) Innovation. Figure 2 indicates the changes to these groupings from the May 2024 rebalance, and we explain some of the details behind them here:

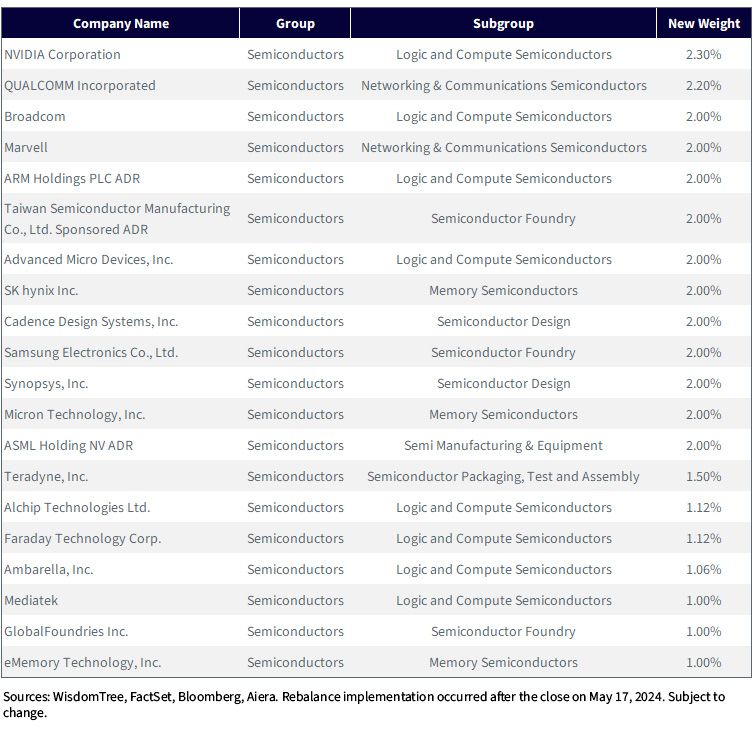

With the semiconductors group representing 42% of the total strategy weight as of the rebalance, we felt it important to show, for illustrative purposes, the top 20 individual company positions within that group. We believe that Nvidia is a historic business story; however, we think that a lot of excitement and growth is already “priced in,” given the company’s massive market capitalization gains in the past 18 months.

This is the core question, and we admit that we do not know what the uptake of AI-enabled devices will be. We believe it represents something tangible and something that can potentially impact company revenues, cash flows and earnings in the second half of 2024. It is also something that users would be able to engage directly with. The big ideas like AI-assisted drug discovery or fully autonomous vehicles are still there, but we are unsure as to when these types of things will have a chance to impact financial fundamentals. WTAI has maintained a diversified exposure to AI, with a tilt toward areas that could benefit if people are inspired to refresh some of their hardware.

For more on AI, join Christopher Gannatti (Global Head of Research) and Mobeen Tahir (Director of Research, Europe) for a discussion about the megatrends shifting the way we live and invest. Register here.

1 Source: https://io.google/2024/

2 Source: Max A. Cherney, “Microsoft debuts ‘Copilot+’ PCs with AI features,” Reuters, 5/21/24.

3 Source: https://developer.apple.com/wwdc24/

5 Sources: https://build.microsoft.com/en-US/home; https://www.dell.com/en-us/dt/events/delltechnologiesworld/2024/index.htm#accordion0; Implementation of the WisdomTree Artificial Intelligence & Innovation Index rebalancing for May 2024 occurred after the close on May 17, 2024, with the new positions opening for their first day of trading on Monday, May 20, 2024.

For current holdings of WTAI, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending in research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Artificial Intelligence and Innovation Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.