QHY

U.S. High Yield Corporate Bond Fund

Published May 30, 2024

Head of Investment and Fixed Income Strategy

While the money and bond markets continue their Fed-watch saga, there is one constant that we have been emphasizing for the fixed income landscape: a new rate regime. An integral aspect of this investment setting is that, despite what the Federal Reserve may or may not do, rates appear to be on course for staying higher for longer.

Against this backdrop, investors have been trying to determine where should they allocate funds in the fixed income universe, specifically within the U.S. Typically, one can break down the bond market into two distinct sectors: interest sensitive and credit sensitive. I’ve been spending a good amount of time in recent blogs posts and podcasts on the interest-sensitive side of the equation, so I thought it would be prudent to address trends for U.S. credit.

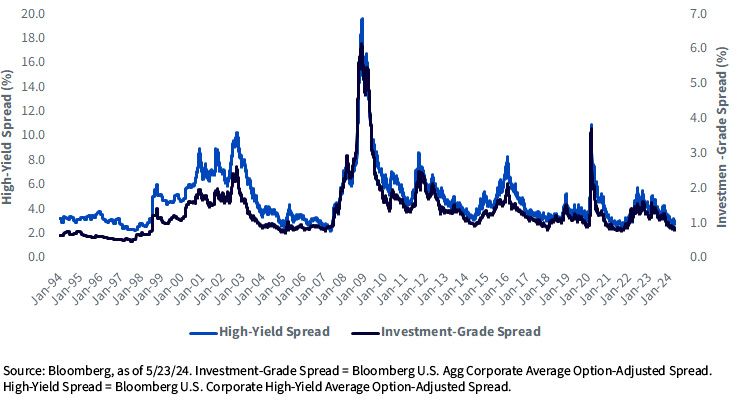

For definitions of terms in the chart above, please visit the glossary.

A key gauge in measuring relative value in U.S. corporate bonds is to look at spread relationships when compared to Treasury securities. These differentials can help determine where current corporate bond yields may reside in relation to historical levels. This analysis applies to both the investment-grade (IG) and high-yield (HY) universes. For reference, a narrow spread is often viewed as a sign that corporates could be leaning toward being expensive, while a wider differential would be viewed as the opposite, or comparatively cheap.

Throughout the better part of this year, there has been a sense among investors that U.S. corporate bonds appear to be more on the expensive side of the ledger due to the fact that both IG and HY spreads have been visibly narrowing since late October. To provide some perspective, IG spreads have declined over 40 basis points (bps) while HY differentials have fallen roughly 140 bps, as of this writing. Their current respective levels of 87 bps and 300 bps places them at the lower end of historical ranges.

This is where things get interesting. To listen to some of the current narrative on the subject, one could be forgiven for thinking the current readings are an unusual development. However, as the above graph illustrates, IG and HY spreads are definitely not in uncharted territory. In fact, there have been a variety of periods in the past when corporates have traded at these levels, and in some cases, even lower.

While I’d be the first to admit that, based on current spread levels, U.S. credit is not necessarily cheap, the resilient economy and somewhat favorable fundamentals seem to suggest they are not necessarily overly expensive either. In fact, using history as our guide, as long as the economy doesn’t fall of the cliff anytime in the months ahead, IG and HY spreads could continue to trade in their present respective ranges, but we would emphasize a quality-screened approach. In fact, if the fundamental backdrop can be maintained, one could potentially argue that a notable re-widening in spreads could be viewed as a buying opportunity, as we saw in pre-Covid trading.

For investors looking to allocate to U.S. credit, here are two quality-screened solutions to consider:

There are risks associated with investing, including possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.